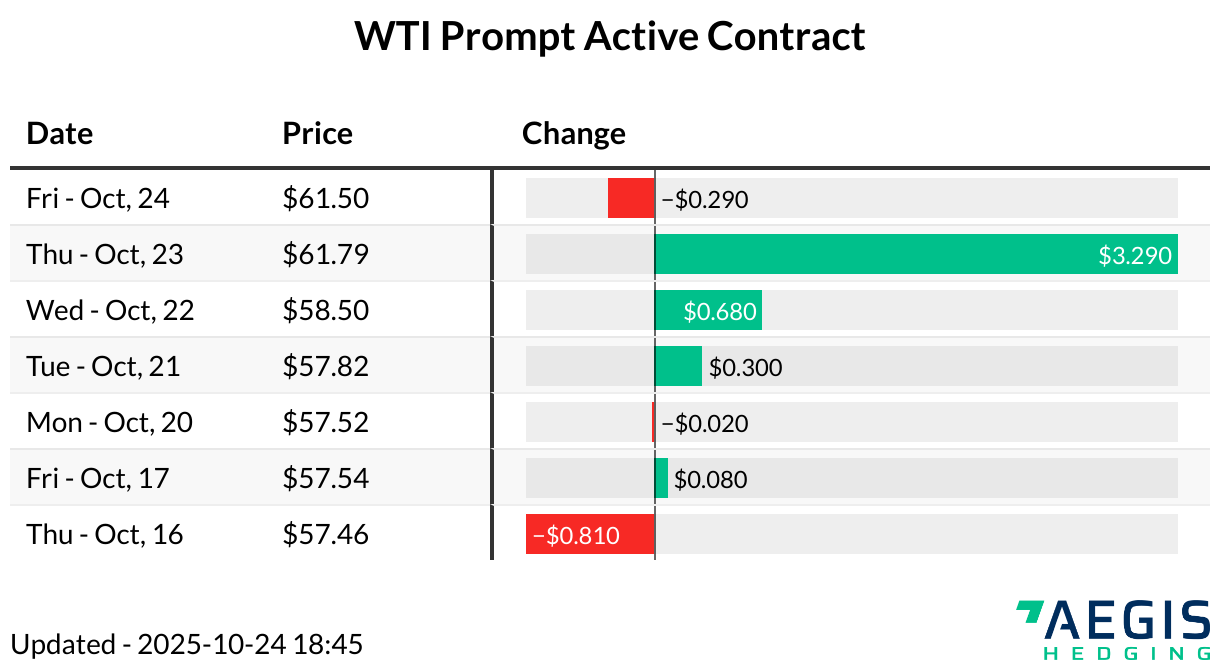

The WTI prompt-month contract climbed $0.52 to $66.15/Bbl on Wednesday morning (7:30 AM CT)

The next round of nuclear negotiations between the US and Iran is scheduled for Thursday in Geneva

The talks come just ahead of this weekend’s OPEC+ meeting, where delegates indicate the group is likely to approve incremental supply increases

OPEC+ has held output targets unchanged through the first quarter of 2026

President Trump said in his State of the Union address that Iran is attempting to rebuild elements of its nuclear program, fueling speculation that military options remain under consideration

Crude prices have reacted sharply to geopolitical headlines this year, rallying even as consensus expectations point to growing global supply

That uncertainty is increasingly evident in the options market, where front-end contracts are skewed toward upside calls (see our latest piece on positive call skew)

In the event of escalation, Iran could respond by threatening traffic through the Strait of Hormuz, a chokepoint that carries roughly one-quarter of global seaborne crude flows

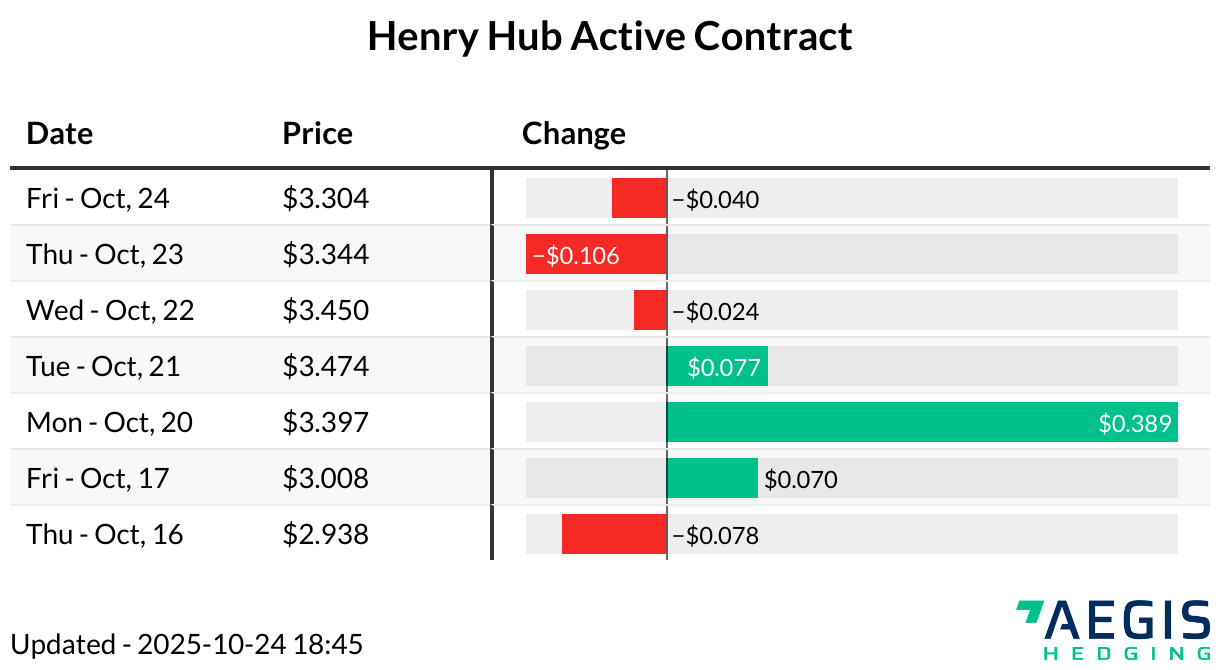

March natural gas rebounds slightly, up 6.3c to $2.978/MMBtu (As of 07:30 AM CDT)

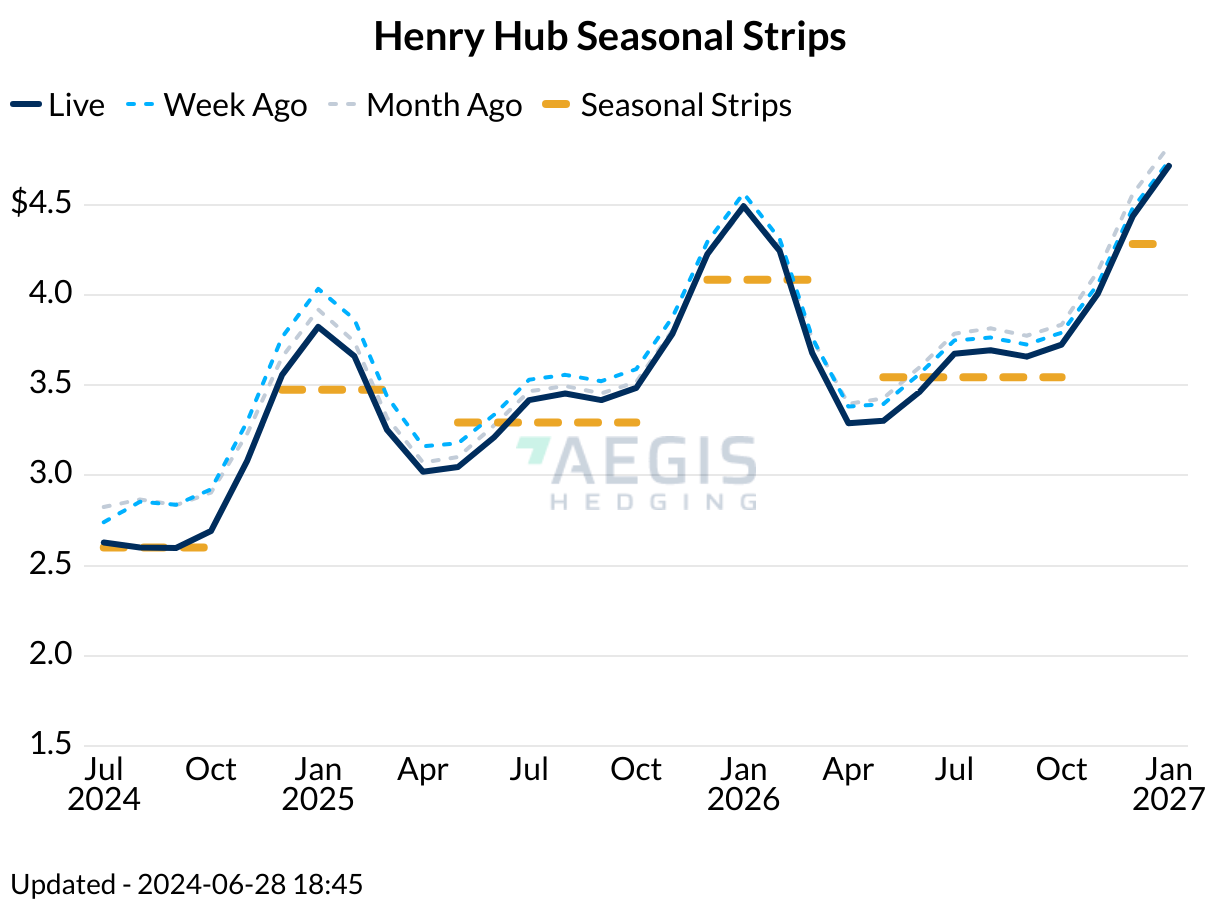

A short-lived cold front is still on the radar for early next week, but the forecast period after that has warmed this morning

L48 temperatures in early-middle March have shifted from normal to above average, sitting around 5 °F above the 10-Year average

Production remains slightly below the 110 Bcf/d level from last week, sitting at 107.2 Bcf/d, as weather shuts in minimal production in the Rockies and Appalachia (S&P)

Total L48 gas demand is down 14 Bcf/d to 134 Bcf/d this morning as temperatures warm after the brief cold spell

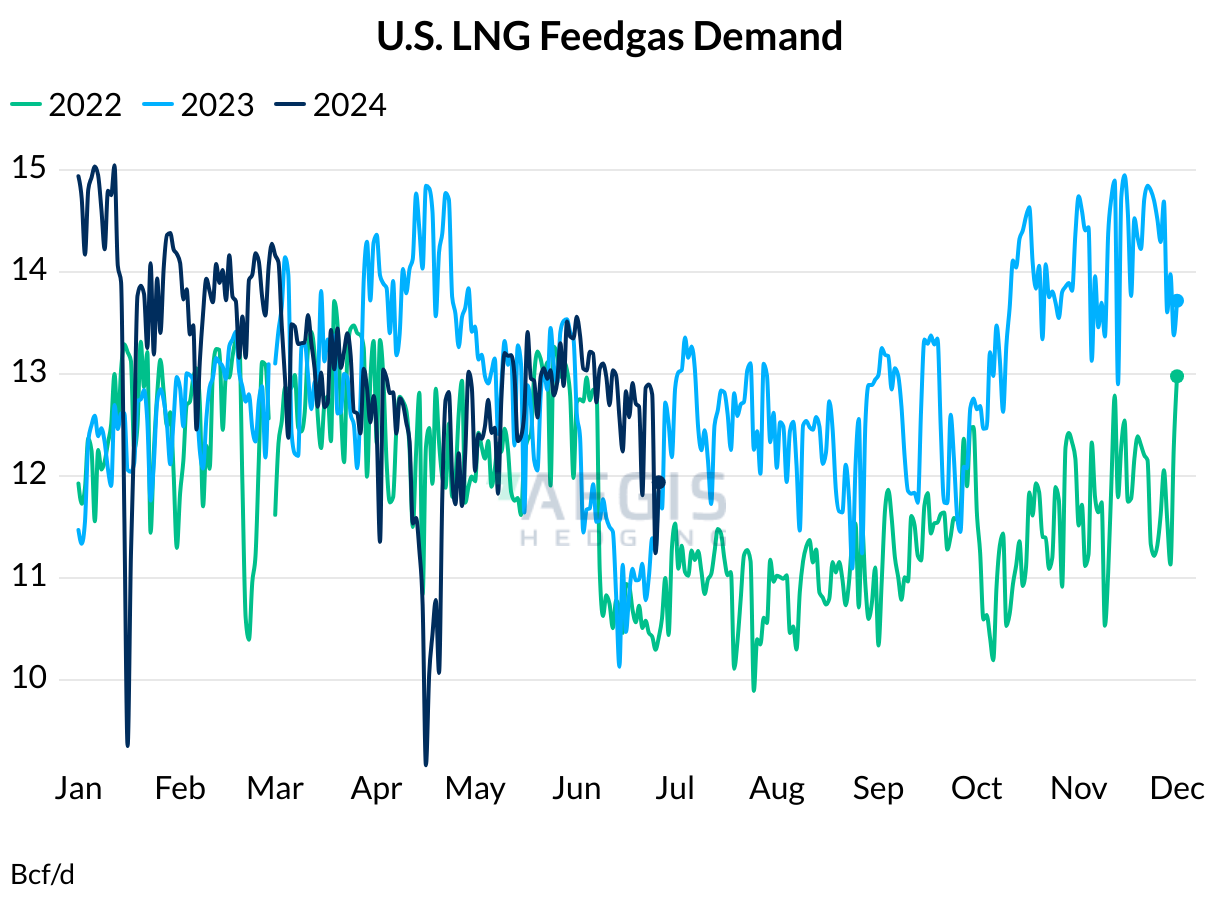

LNG feedgas demand is at 19.6 Bcf/d, at the lower end of the recent range (Criterion)

Forecasts for next week sit at 20.4 Bcf/d, suggesting a quick recovery supported by ongoing commissioning at Corpus Christi Stage 3

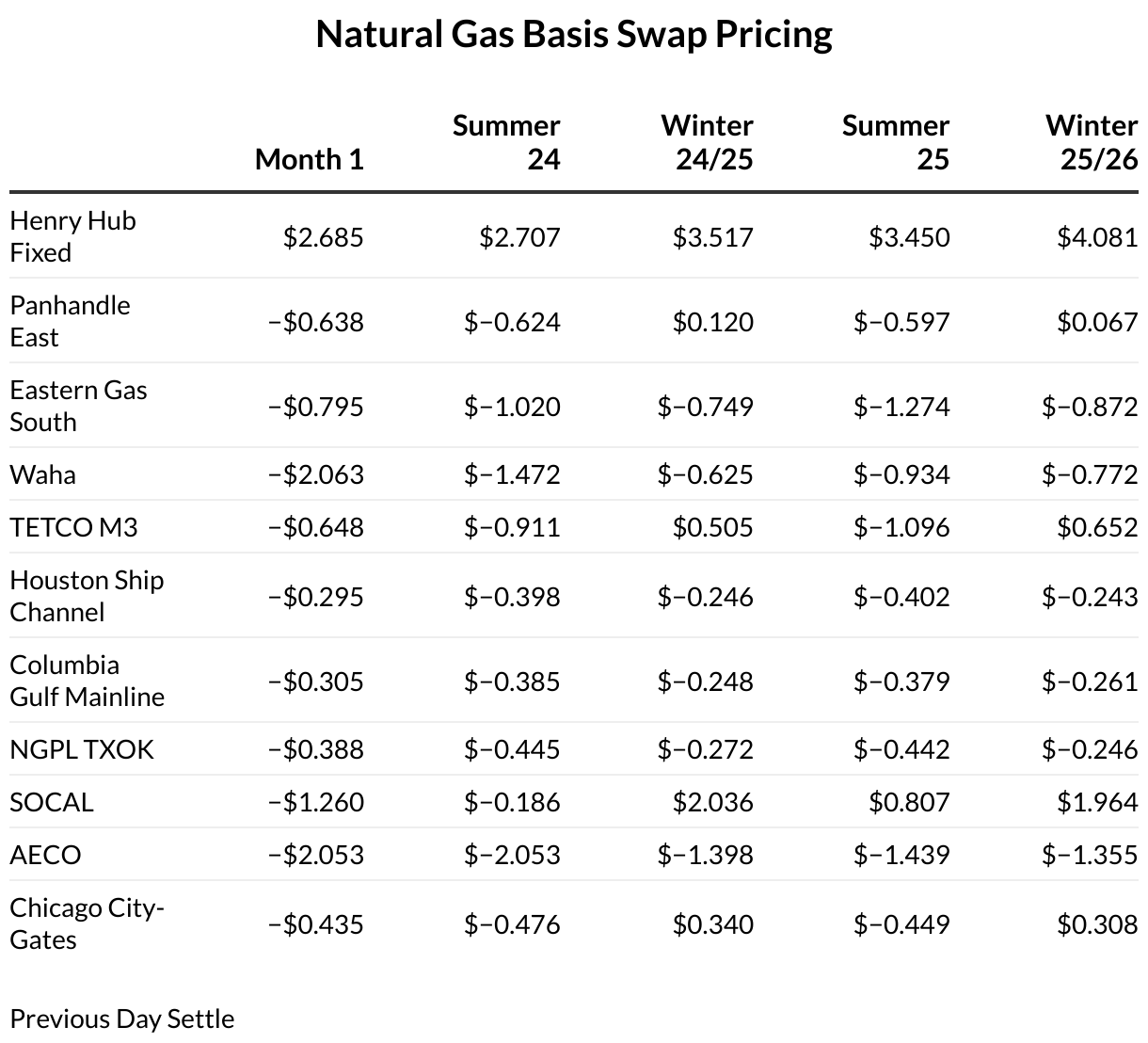

HSC at wide discount to Katy hub amid Weak Texas demand (S&P)

The Katy premium to HSC has averaged 46c/MMbtu over the course of February

HSC is heavily influenced by local consumption, which has been weak this month

Get market insights delivered to your Inbox every day!