Oil Steadies on Geopolitical Risk; Natural Gas Pulls Back After Weather-Driven Rally

- Oil steadies as geopolitical risk offsets oversupply outlook

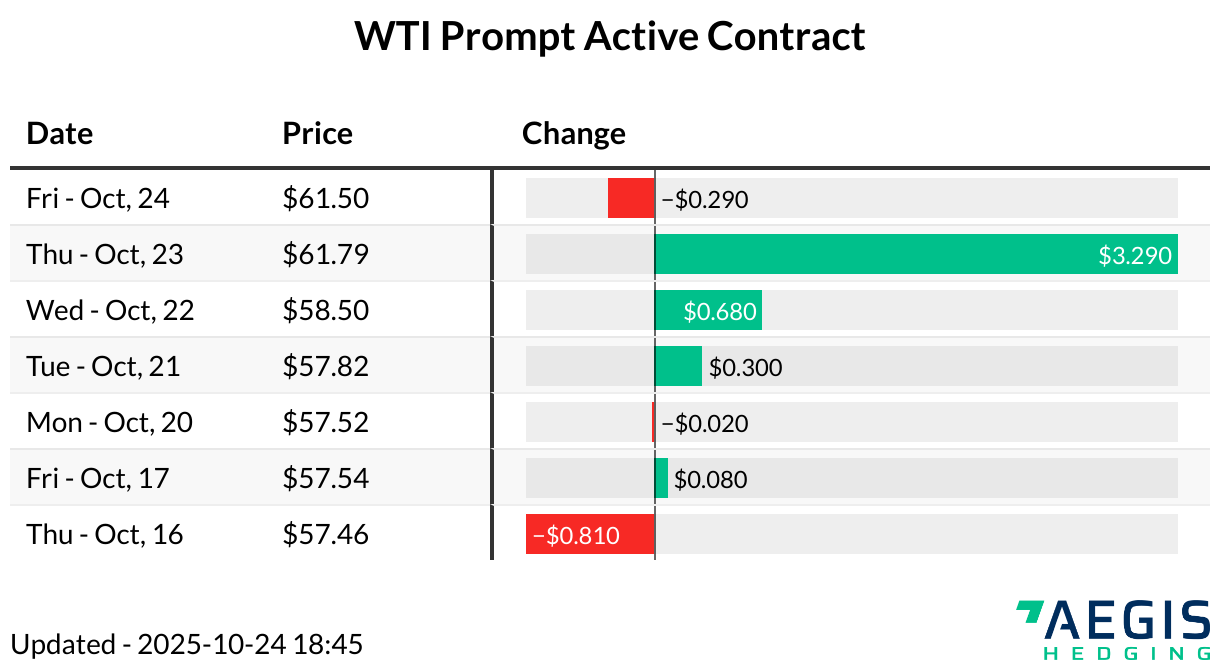

- The WTI prompt-month contract rose $0.07 to $58.45/Bbl on Wednesday morning (7:45 AM CT)

- Prices have rebounded from last week’s multi-year lows, helped by escalating US pressure on Venezuelan oil exports

- The US is still pursuing an additional tanker tied to Venezuelan crude, reinforcing concerns around export disruptions and freight risk

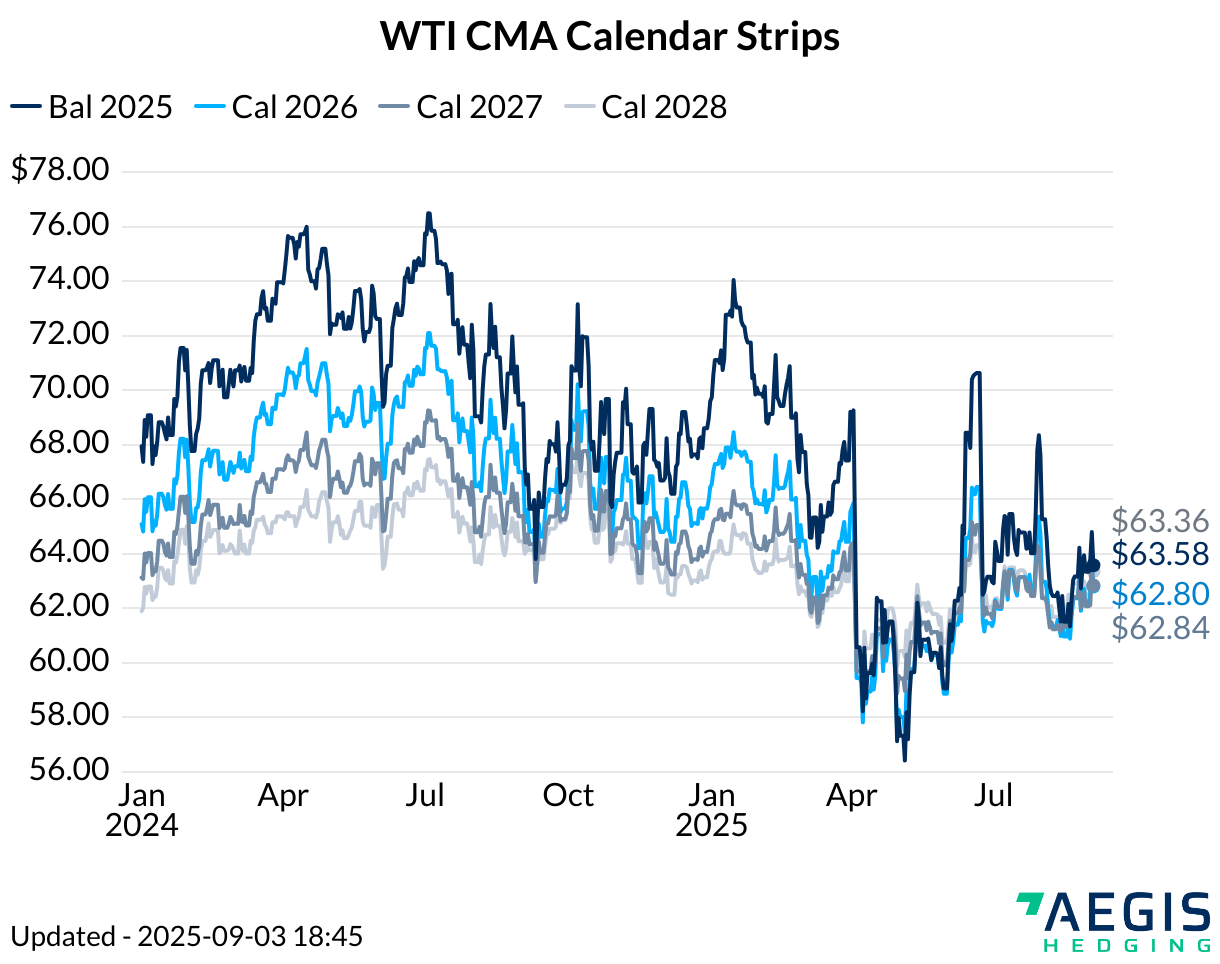

- Despite headline risk, the broader market remains focused on a growing global surplus in 2026 as OPEC+ and non-OPEC supply outpaces demand

- Geopolitical premiums have provided near-term price support, but have not materially shifted the underlying oversupply narrative

- US inventory data remains bearish, with API reporting a 2.4 MMbbl build in crude stocks last week

- Official EIA inventory data will be released later than usual due to the federal holiday

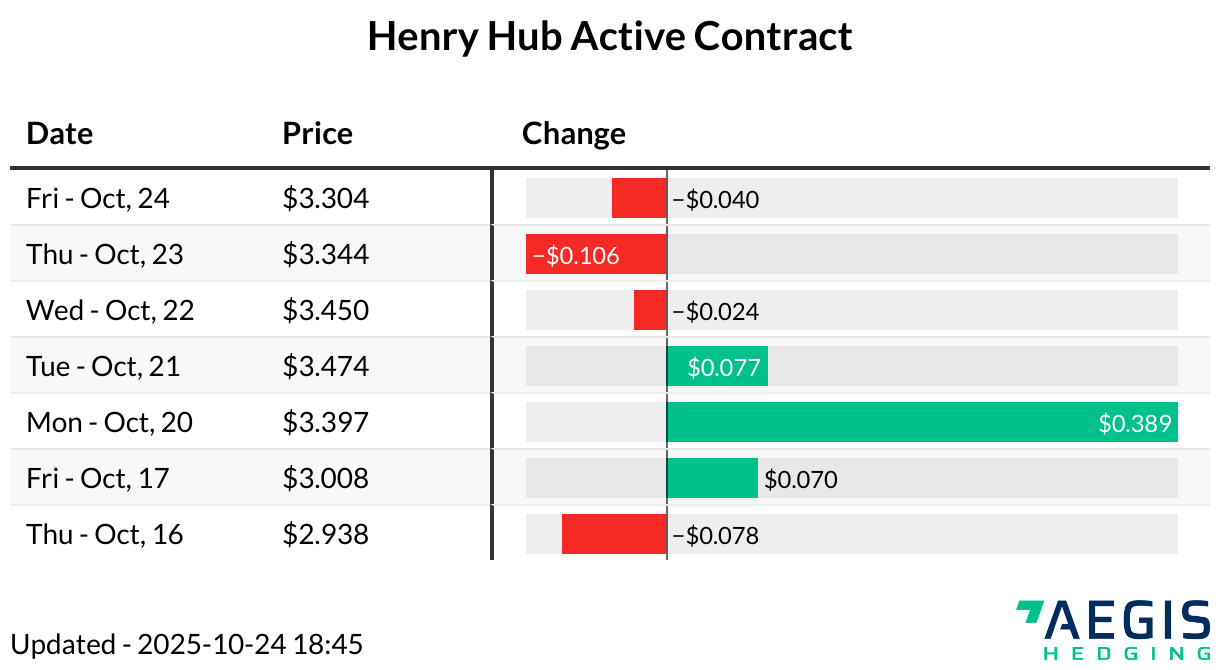

- Natural gas trades lower after yesterday’s rally

- The January contract climbed from $4/MMbtu to as high as $4.40/MMbtu yesterday, but is lower this morning, near $4.30/MMbtu (8:15 AM)

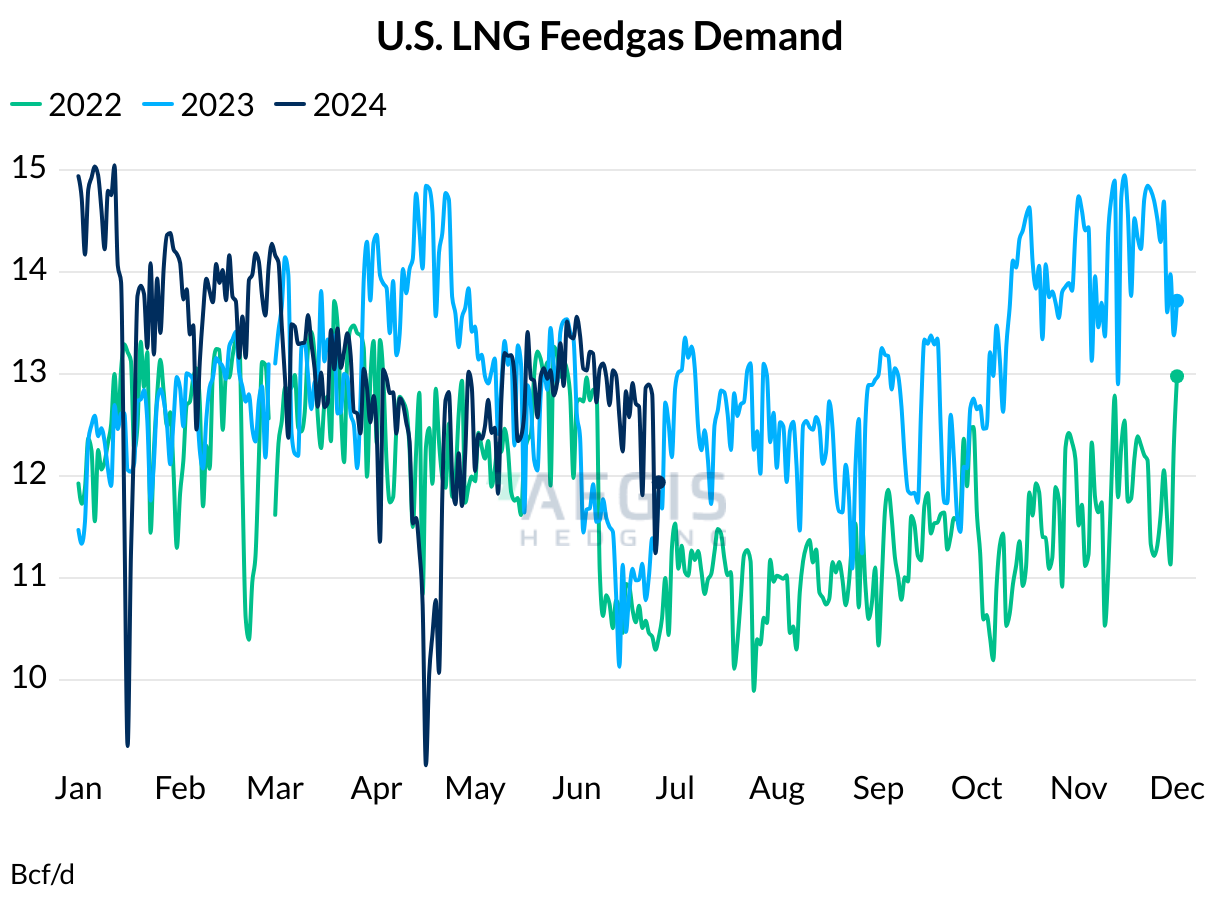

- Since last week, Lower-48 weather forecasts have shifted colder, resulting in a significantly improved near-term demand outlook

- Dry gas production is down slightly but still above 109 Bcf/d, according to data from S&P

- More LNG export projects expected to FID in 2026 (S&P)

- After a record year for LNG export project final investment decisions, more US projects are expected to FID this year

- Its expected that up to 3.75 Bcf/d of new projects could move forward this year

- Most new projects will be several years from startup, likely around the beginning of the 2030s

- However, the IEA has cautioned against complacency regarding LNG projects set to start up in the 2030s

^