Geopolitical tension lifts oil, but outlook remains bearish

The WTI prompt-month contract climbed to its highest level in nearly two months, rising $0.74 on Friday to settle at $65.72/Bbl, as markets balanced intensifying geopolitical risks against signs of additional supply returning to the market.

In Europe, Ukraine ramped up its drone strikes on Russian energy infrastructure, with fresh attacks reported on the Afipsky refinery in southern Russia and facilities along the Black Sea coast. Bloomberg reported the strikes have taken more than 7% of Russia’s refining capacity offline, spurring domestic fuel shortages and prompting Moscow to consider curbs on diesel exports. Despite these setbacks, Russian crude exports remained resilient. As volumes were diverted from refineries to export terminals, seaborne shipments climbed to a 16-month high of 3.62 MMBbl/d, underscoring the difficulty of materially curtailing Russian flows even as refinery output falters.

At the same time, Western leaders escalated their rhetoric. President Trump urged NATO allies to shoot down Russian aircraft violating allied airspace and pressed Turkey and Hungary to halt Russian oil purchases. Canadian Prime Minister Mark Carney called for swift implementation of secondary sanctions, while France emphasized that Europe’s remaining Russian imports are now “very marginal.”

Yet, potential disruptions to Russian supply were countered by new sources of oil coming back to market. Iraq announced a breakthrough deal to resume Kurdistan exports via the Ceyhan pipeline. Initial flows are expected around 230 MBbl/d, with volumes potentially rising to 400–500 MBbl/d over the coming months as new fields ramp up. This development highlights how regional supply gains are helping offset geopolitical risks elsewhere.

On the demand side, U.S. consumer confidence softened in September, with the Michigan sentiment index falling to 55.1 from 58.2 in August and finishing slightly below expectations. A similar tone emerged in the Dallas Fed Energy Survey, where the Business Activity Index stayed negative at -6.5 and nearly four out of five executives reported delaying investments due to rising costs and uncertainty. Both households and producers appear cautious, holding back on spending until inflation cools and demand signals become clearer.

While heightened geopolitical tensions supported crude prices this week, the fundamental backdrop continues to point toward oversupply. The resilience of Russian exports, the resumption of Kurdish flows, and sluggish domestic demand all reinforce expectations of a surplus heading into 2026. AEGIS maintains a bearish outlook.

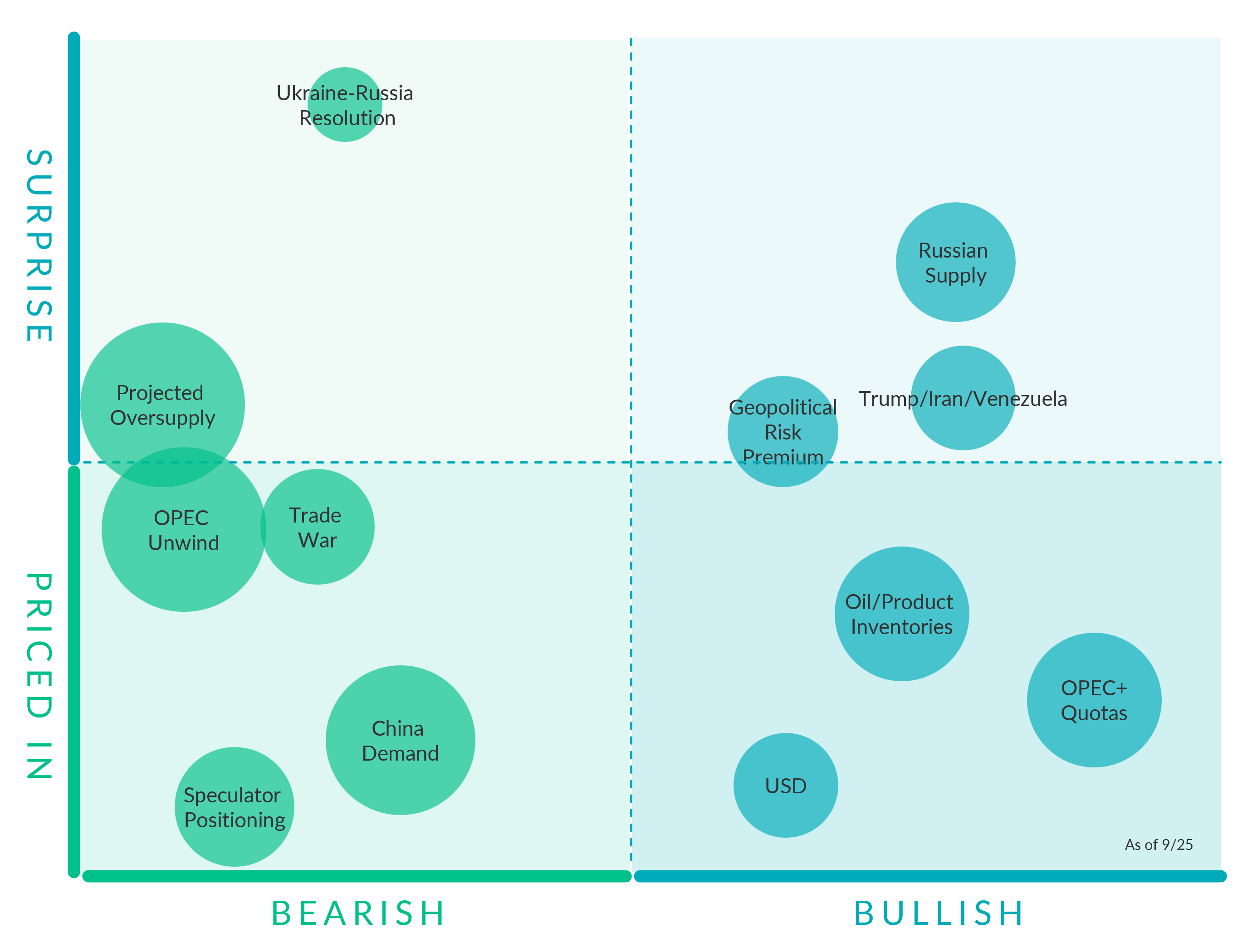

Crude Oil Factors

Geopolitical Risk Premium. (Bullish, Mostly Priced In)President Trump urged NATO allies to shoot down Russian aircraft violating allied airspace and pressed Turkey and Hungary to halt Russian oil purchases. Canadian Prime Minister Mark Carney called for swift implementation of secondary sanctions, while France emphasized that Europe’s remaining Russian imports are now “very marginal.”

Speculator Positioning (Bearish, Priced In) The latest CFTC data show that as of August 12, money managers reduced their net long in CME’s flagship NYMEX WTI contract to just 48,865 contracts, the smallest bullish position since April 2009. Meanwhile, trades of WTI done on the ICE exchange show money managers holding a net short of about 53,000 contracts. When the two venues are combined, overall positioning in WTI has slipped into net short territory for the first time on record.

Oil/Product Inventories. (Bullish, Priced In) The latest EIA report leaned bearish as well, showing a surprise build in commercial crude inventories of roughly 600 MBbls and a 2.1 MMBbl increase at Cushing, which pushed stocks at the hub to their highest level since early May and pressured prompt-month spreads. Product demand indicators were softer, with total refined product supplied running nearly 2% below the same week last year, and exports slipped to about 3.55 MMBbl/d after several weeks of strength, signaling a weaker pull from international buyers.

OPEC+ Quotas. (Bullish, Priced In) On June 2, OPEC+ announced its extension of 3.66 MMBbl/d cuts through December 2025. Additionally, the 2.2 MMBbl/d voluntary cuts from eight member countries will continue into Q3 2024 but will start to be reversed in October at a rate of 0.18 MMBbl/d per month. OPEC+ members agreed on September 5 to delay a planned gradual 2.2 MMBbl/d supply hike by two months, shifting the start to December. The group will add 0.19 MMBbl/d in December and 0.21 MMBbl/d from January onwards, with an option to adjust or pause these hikes depending on market conditions. The cartel also reaffirmed its compensation cuts of 0.2 MMBbl/d per month through November 2025, as members such as Iraq, Russia, and Kazakhstan have struggled to meet their original production quotas.

AEGIS notes that the global crude market would quickly build inventories without OPEC's support in reducing supply.

OPEC Unwind. (Bearish, Mostly Priced in) OPEC+ announced it will raise the group’s production quota by 137 MBbl/d for October, marking the start of unwinding 1.66 MMBbl/d of voluntary cuts that were originally planned to stay in place through the end of 2026.

China Demand. (Bearish, Priced In) China’s behavior remains the key wild card. Goldman Sachs expects Beijing to continue filling commercial and strategic tanks through 2026, projecting inventory builds of 500 MBbl/d over the next five quarters. Analysts note that without renewed Chinese stockpiling, OECD inventories could swell noticeably as new OPEC+ and non-OPEC supply hits the market.

USD (Bullish, Priced In) The Federal Reserve cut its benchmark interest rate by 25 basis points, the first cut since December 2024, and signaled that another 50 basis point cut could be coming by then end of 2025. If markets expect rate cuts or looser monetary conditions, the dollar tends to weaken. Oil is priced in dollars, so a weaker dollar lowers the “real” cost of oil for buyers using other currencies. This often boosts demand at the margin and supports prices.

Ukraine-Russia Resolution. (Bearish, Surprise) President Trump is pushing for a summit between Vladimir Putin and Volodymyr Zelensky following a series of high-level talks. Vandana Hari of Vanda Insights said crude “may be in for a holding pattern,” noting that while the path to a resolution has opened, it could take time. A peace deal could eventually ease restrictions on Russian crude exports, though Moscow has largely maintained flows throughout the conflict.

Trade War. (Bearish, Mostly Priced In) A federal appeals court ruled that most of President Trump’s global tariffs were illegal, saying he exceeded his authority. The decision adds uncertainty over the tariffs’ future, and while the Trump administration looks to appeal the decision the ruling is set to take effect on October 14 unless overturned, which has raised hopes for stronger economic growth.

Projected Oversupply. (Bearish, Mostly Surprise) According to the EIA, global oil inventories are expected to rise by an average of 1.7 MMBbl/d in 2025, followed by a slightly slower but still significant 1.6 MMBbl/d increase in 2026. The most aggressive builds are forecast for 4Q 2025 and 1Q 2026, when inventories are projected to swell by 2.3 MMBbl/d on average.

Trump/Iran/Venezuela. (Bullish, Surprise) The US government has sent several ships off the coast of Venezuela prompting speculation that the Trump administration may be seeking to push Venezuelan President Nicolas Maduro from power. Tensions rose after the US sent fighter jets to the Carribean after two Venezuelan military aricraft flew over an American naval vessel in the area.

Russian Supply. (Bullish, Surprise) In Europe, Ukraine ramped up its drone strikes on Russian energy infrastructure, with fresh attacks reported on the Afipsky refinery in southern Russia and facilities along the Black Sea coast. Bloomberg reported the strikes have taken more than 7% of Russia’s refining capacity offline, spurring domestic fuel shortages and prompting Moscow to consider curbs on diesel exports. Despite these setbacks, Russian crude exports remained resilient. As volumes were diverted from refineries to export terminals, seaborne shipments climbed to a 16-month high of 3.62 MMBbl/d, underscoring the difficulty of materially curtailing Russian flows even as refinery output falters.

Commodity Interest Trading involves risk and, therefore, is not appropriate for all persons; failure to manage commercial risk by engaging in some form of hedging also involves risk. Past performance is not necessarily indicative of future results. There is no guarantee that hedge program objectives will be achieved. Certain information contained in this research may constitute forward-looking terminology, such as “edge,” “advantage,” ‘opportunity,” “believe,” or other variations thereon or comparable terminology. Such statements and opinions are not guarantees of future performance or activities. Neither this trading advisor nor any of its trading principals offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program.