| Commodity / Low Carbon Fuel Standard Exploring the LCFS ProgramA closer look into the program encouraging the use of cleaner fuels in the transportation sector.How it Works Market Impact Future Trends | |

| | OverviewThe Low Carbon Fuel Standard (LCFS) is a regulatory program aimed at reducing greenhouse gas (GHG) emissions by promoting the use of cleaner, lower-carbon fuels in the transportation sector. California’s LCFS, established under the Global Warming Solutions Act (AB 32), is the oldest and most rigorous program in the United States. The regulation requires fuel providers to gradually lower the carbon intensity (CI) of transportation fuels over time. Fuels with a CI below the annual benchmark generate LCFS credits, while those above generate deficits. Providers must balance their deficits with credits, either by producing or purchasing them. This creates a market-based incentive to invest in and adopt innovative low-carbon technologies and alternative fuels. The LCFS is a cornerstone of California’s broader climate strategy and continues to evolve as a model for other jurisdictions aiming to decarbonize their transportation sectors. |

How LCFS WorksLCFS programs operate through a credit and deficit system. Fuel providers must balance their deficits with credits, either by producing low-carbon fuels themselves or purchasing credits from others. This market-based mechanism allows for flexibility and incentivizes the adoption of cleaner fuels. Companies and governments use LCFS credits to meet regulatory requirements. The trading of credits also provides a financial incentive for companies to exceed their carbon reduction targets, fostering a competitive market for low-carbon solutions. The overall result is a gradual decarbonization of the transportation sector, with measurable reductions in GHG emissions. |

| Carbon Intensity Benchmarks & Credit/Deficit Generation State regulators set benchmark CI targets for each year, representing the maximum allowable carbon intensity for fuels. This benchmark decreases annually, gradually tightening the standards and requiring continual improvement in fuel carbon efficiency. Suppose the CI benchmark for a particular year is set at 95 grams of CO2 equivalent per megajoule (gCO2e/MJ). | A company producing bioethanol with a CI of 60 gCO2e/MJ would generate credits because its CI is below the benchmark of 95 gCO2e/MJ. However, a company refining petroleum diesel with a CI of 105 gCO2e/MJ would generate deficits, as it exceeds the benchmark. LCFS credits can be traded between companies, providing flexibility in how they meet their CI reduction obligations. Companies that produce low-CI fuels can sell excess credits to those that generate deficits, creating a financial incentive for innovation and the adoption of cleaner technologies. |

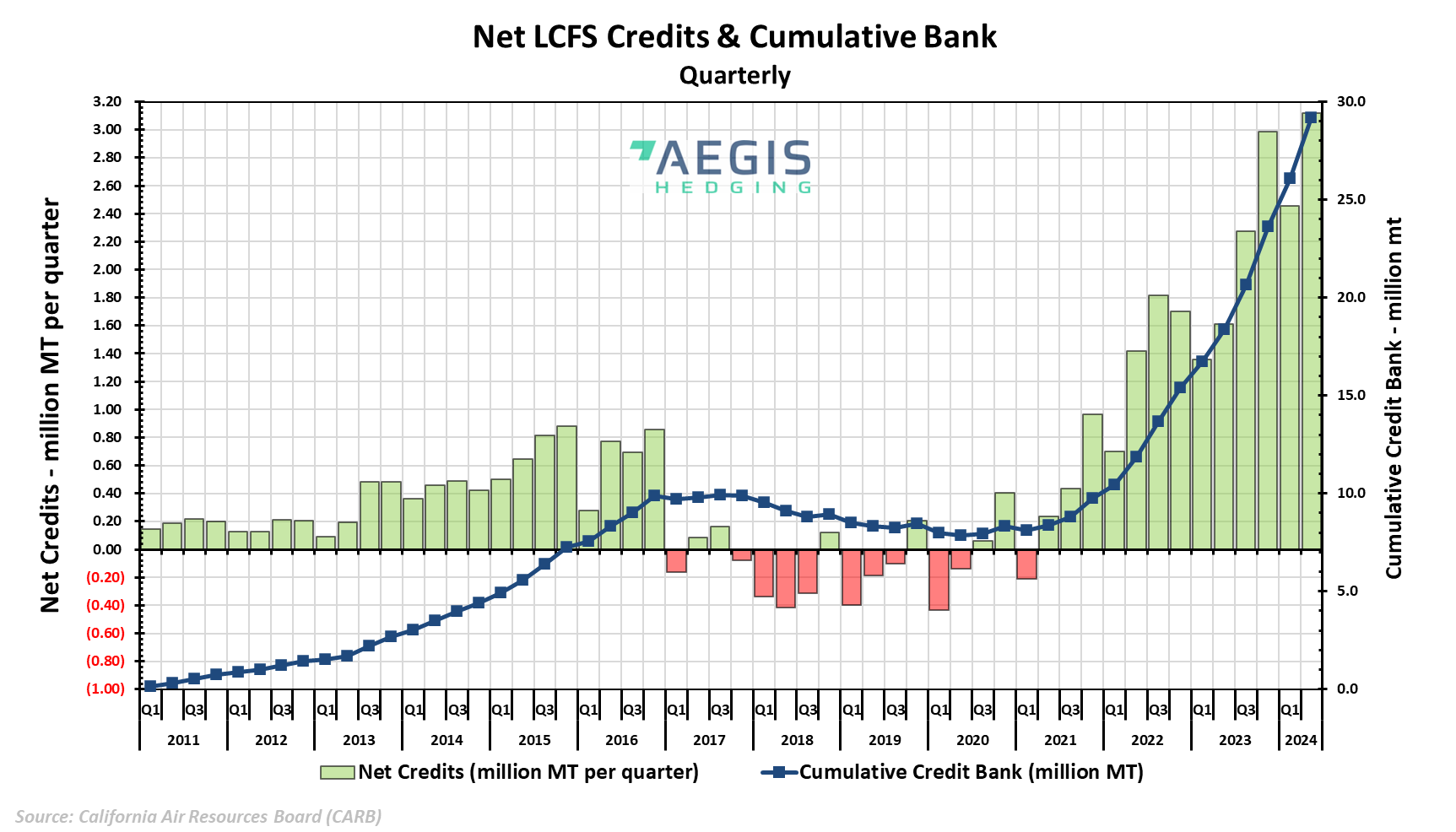

| Credit Banking and Carrying Over Deficits Unlike other environmental credit programs, LCFS credits do not expire. Companies can bank excess credits for future use, providing a cushion against years where they might struggle to meet CI targets. Conversely, if a company cannot purchase enough credits to offset its deficits each year, it may carry over the deficit to the next year. However, repeated deficits can lead to penalties. A company that generates more credits than needed in 2024 may bank those credits to offset potential deficits in 2025, especially if they anticipate challenges in meeting the more stringent CI benchmarks of the future. |  |

A wide range of low-carbon fuels and technologies are eligible to generate LCFS credits. These include:

| Biofuels Ethanol, biodiesel, renewable diesel, and biogas, especially when produced from waste products or other low-CI feedstocks. | Hydrogen Produced using renewable energy sources through processes like electrolysis. | Natural Gas Compressed natural gas (CNG) or liquefied natural gas (LNG), particularly if derived from renewable sources like landfill gas. |

The LCFS program creates a dynamic market where the supply and demand for credits can lead to price fluctuations. Companies with innovative low-carbon technologies can profit from selling credits, while those reliant on high-carbon fuels face increasing costs.

If a new technology significantly lowers the CI of a fuel, the market could see a surge in credit supply, potentially lowering credit prices. Conversely, a shortage of low-carbon fuel production could drive prices up, increasing costs for deficit-generating companies.

Future Trends & Innovations

|