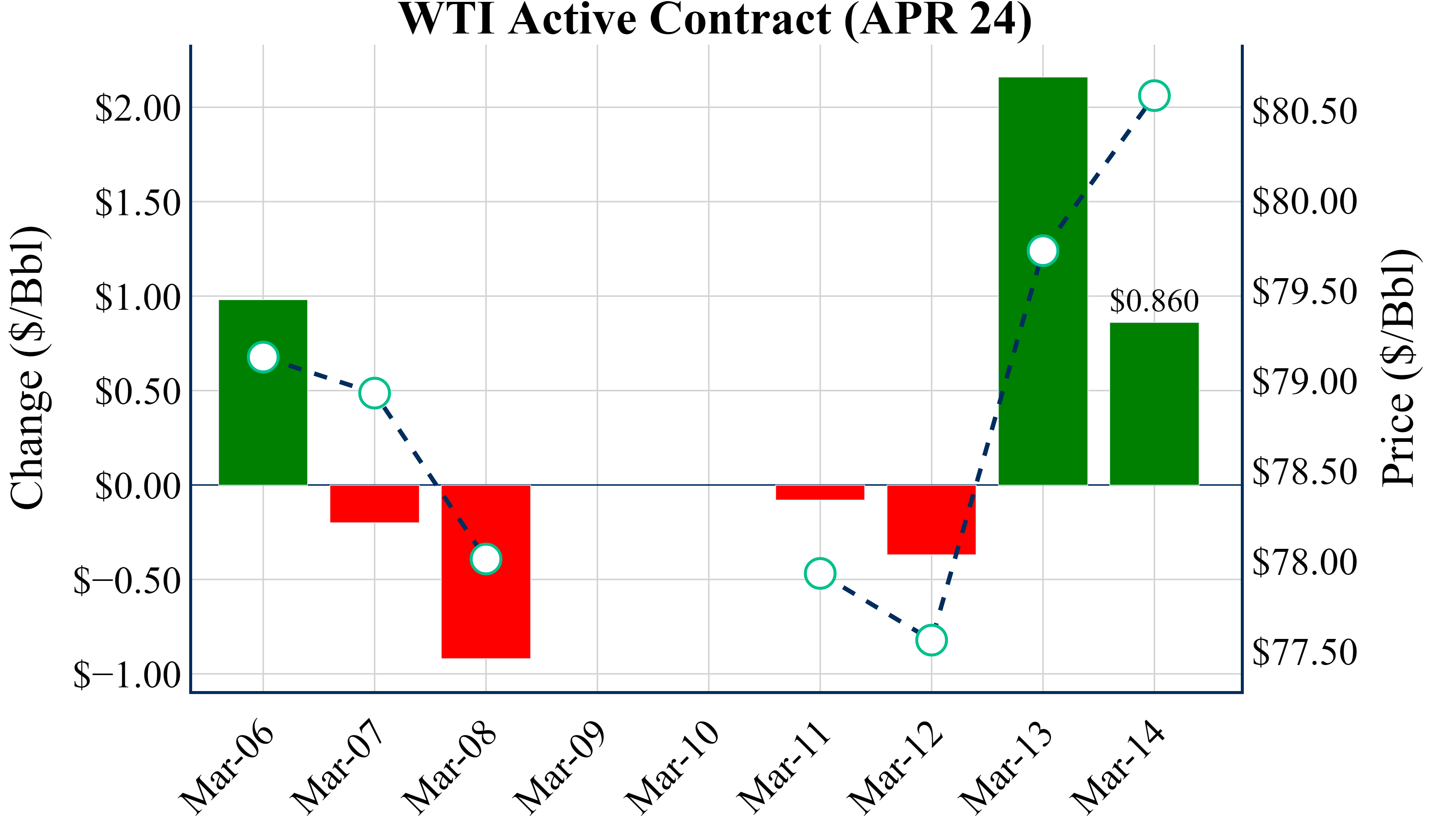

Following yesterday's EIA inventory report, US crude storage is about 3% below the five-year average

IEA says oil markets to be undersupplied on OPEC+ cuts (BBG)

Global oil markets could be in a supply deficit in 2024 instead of a surplus, which the IEA previously forecasted, if OPEC continues to reduce supply through the second half of the year

The IEA said, “The changed assumptions shift our implied balance into a slight deficit rather than the hefty build in last month’s report”

The agency also increased its forecast for global demand growth by 110 MBbl/d to 1.3 MMBbl/d due to a stronger US outlook and higher demand for ship fuel as vessels take longer routes to avoid the Red Sea

On June 1, OPEC will decide whether to extend the supply cuts through the rest of the year

Chinese refiners cut output (BBG)

Independent refineries in China have reduced operating rates to a two-year low as demand for products has fallen

When adjusting for the pandemic and the Shanghai lockdown, refinery run rates are the weakest since 2016

China’s independent refineries are more sensitive to market prices than the larger state-run refineries and will typically throttle output quicker

The Chinese manufacturing sector has been contracting since September, leading to a reduction in diesel demand

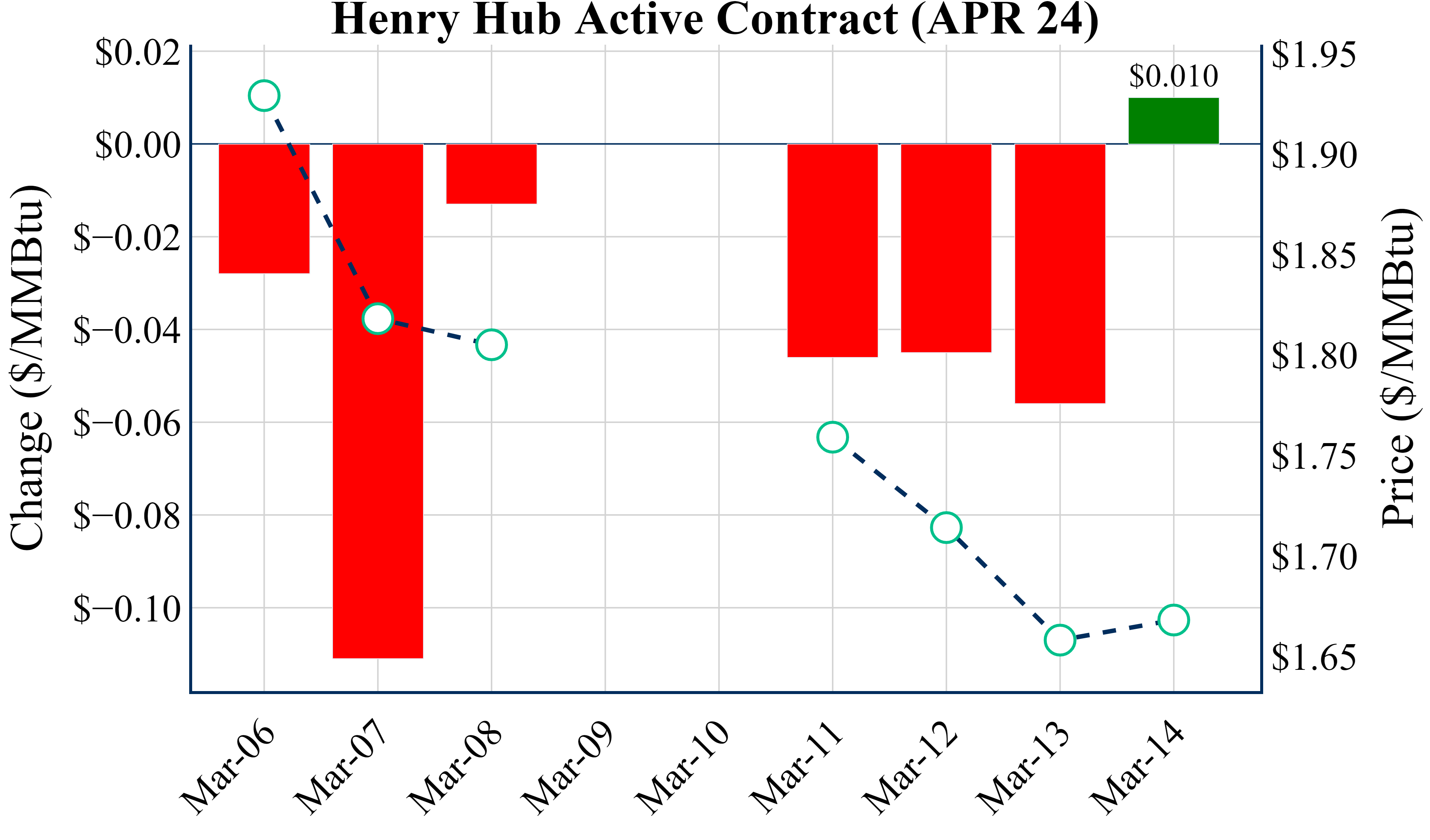

Natural gas prices trade slightly higher ahead of the weekly storage report

April ’24 Henry Hub is up 1.2c this morning to trade around $1.670/MMBtu

The Summer ’24 strip is down 0.2c to $2.201, and the Winter ‘24/’25 strip is up 0.6c to $3.382

Today's Euro Ens forecasts a cooling in the 6-10 day period and warming in the 11-15 day, with a final cold shot next week before temperatures warm, remaining slightly below normal post this week's heat

Lower 48 natural gas production rose by +0.21 Bcf/d yesterday to 99.61 Bcf/d but fell to 99.27 Bcf/d today due to declines in the South Central and Northeast, with potential for a supply rebound this weekend amid ongoing Permian maintenance (Criterion)

Physical gas prices at Waha Hub trade below zero for three straight days amid pipeline maintenance (S&P)

Maintenance on the El Paso pipeline restricted east-to-west capacity in West Texas by 213 MMcf/d from March 12-14, impacting physical gas prices at the Waha Hub in the Permian Basin

The El Paso pipeline is expected to return to full capacity on March 15, potentially alleviating some pressure on gas prices

The negative trading of gas prices is also expected in April due to scheduled maintenance on the Gulf Coast Express for several weeks

NextDecade aims to finalize a contract with Bechtel for Rio Grande LNG expansion by July (NGI)

NextDecade targets a July deal with Bechtel for phase two expansion of the Rio Grande LNG project, aiming to boost global LNG capacity by 17.6 MMTY by 2027

After starting construction on the first three trains, the focus is now on finalizing a phase two EPC contract, with an eye on the surging global LNG demand

Following a successful $18.4 billion financing for phase one, NextDecade aims for a year-end FID on the expansion

Negotiations are underway for up to 9.4 MMTY of expansion capacity, with the potential for a 3 MMTY commitment from TotalEnergies

Get market insights delivered to your Inbox every day!