WTI rebounds from five-month low as US sanctions on Russia jolt market

WTI crude staged a sharp reversal this week, climbing from a five-month low after the US announced sweeping sanctions on Russia’s top oil producers. The WTI prompt-month contract rose $3.96 week-over-week to settle at $61.50/Bbl on Friday, as traders priced in renewed geopolitical risk after earlier weekly declines.

Crude prices opened at $57/Bbl on Monday, the lowest since May, amid signs that supply growth continues to outpace demand. The IEA’s latest Oil Market Report projected a widening surplus approaching 4 MMBbl/d in early 2026, driven by the unwinding of OPEC+ voluntary cuts and new output from non-OPEC countries. Despite optimism around upcoming US–China trade talks, fundamentals remained heavy, keeping bearish sentiment intact through midweek.

Momentum shifted on Wednesday after reports that India was preparing to scale back Russian crude purchases as part of a potential US–India trade deal. The prospective agreement, which would reduce tariffs on Indian exports in exchange for a phased wind-down of Russian oil imports, signaled growing diplomatic coordination ahead of an expected EU sanctions vote.

The real inflection came Thursday when Washington blacklisted Russian state-owned Rosneft and Lukoil, sending WTI prices up over $3/Bbl intraday. Analysts at Rystad Energy estimate 500–600 MBbl/d of Russian output could be curtailed, forcing Moscow to rely more heavily on shadow tanker fleets and Chinese buyers.

Despite the late-week rally, underlying fundamentals remain unchanged. OPEC+ supply recovery, record US production, and elevated crude-on-water volumes continue to point toward a structurally oversupplied market heading into 2026. The rebound was driven primarily by renewed geopolitical risk rather than a shift in physical balances. Any sustained price strength will depend on how aggressively India enforces reductions and whether Russia can reroute displaced barrels to China or other buyers.

This week’s developments highlight the market’s ongoing tension between oversupply and geopolitical volatility. While Russian barrels could indeed fall from the market under the new sanctions, the extent of any disruption remains uncertain, and it may take time to gauge how material the impact truly is. For producers, the rally offers an opportunity to layer in incremental hedges or extend existing positions at improved strike levels. With the structural surplus still intact and agency forecasts pointing to continued inventory builds into 2026, upside driven by geopolitical risk is likely to be temporary. AEGIS maintains a bearish outlook, viewing the week’s rally as a window to manage price exposure rather than a durable shift in fundamentals.

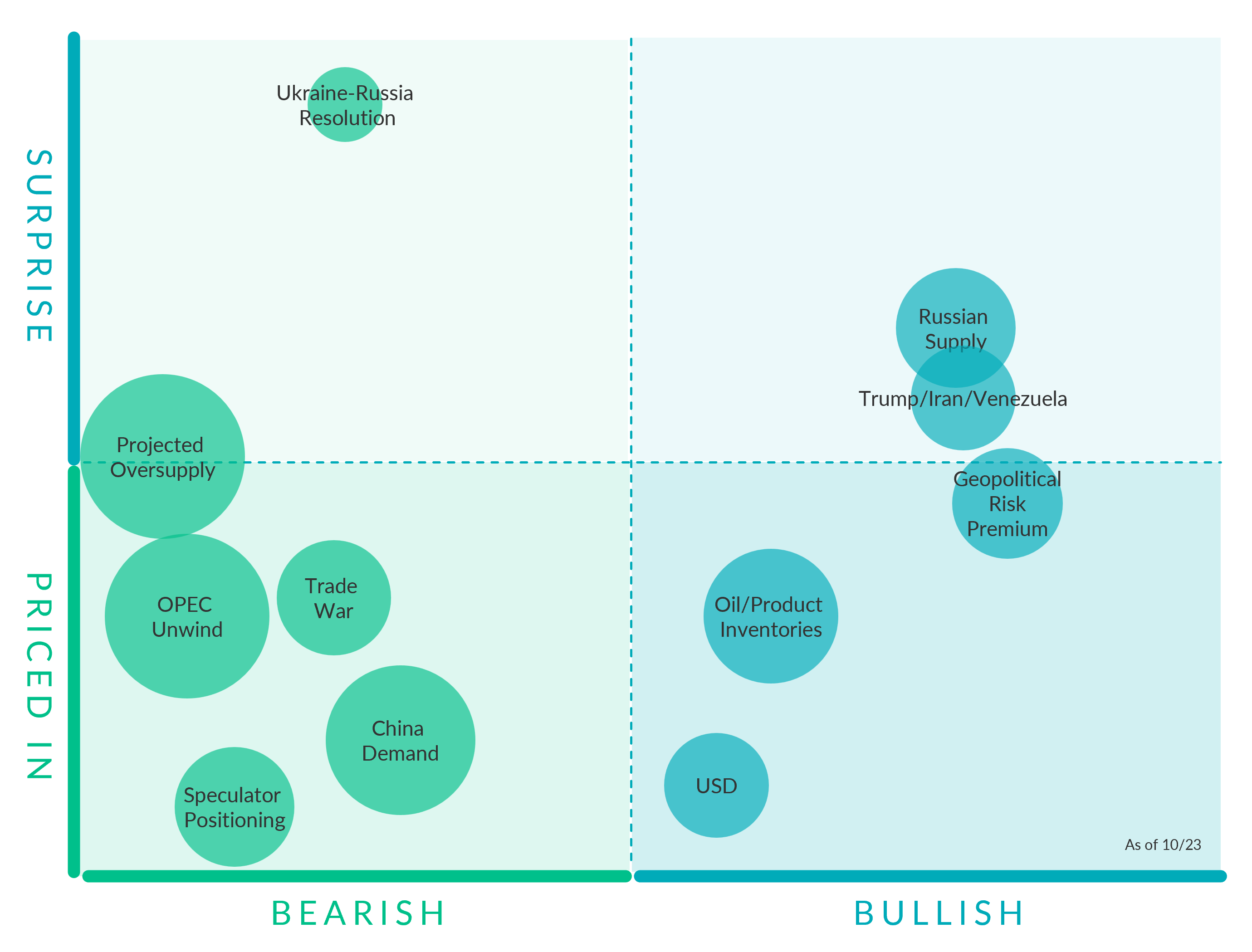

Crude Oil Factors

Geopolitical Risk Premium. (Bullish, Mostly Priced In) The US announced they would be blacklisting Russian state-owned companies Rosneft and Lukoil, sednign WTI prices up over $3/Bbl intraday.

Speculator Positioning (Bearish, Priced In) The latest CFTC data show that as of August 12, money managers reduced their net long in CME’s flagship NYMEX WTI contract to just 48,865 contracts, the smallest bullish position since April 2009. Meanwhile, trades of WTI done on the ICE exchange show money managers holding a net short of about 53,000 contracts. When the two venues are combined, overall positioning in WTI has slipped into net short territory for the first time on record.

Oil/Product Inventories. (Bullish, Priced In) The EIA reported a 3.53 MMBbl build in US commercial crude inventories last week. The build marks the third consecutive weekly build, the first such streak since April, bringing total nationwide inventories to about 423.8 MMBbls.

OPEC+ Quotas. (Bullish, Priced In) On June 2, OPEC+ announced its extension of 3.66 MMBbl/d cuts through December 2025. Additionally, the 2.2 MMBbl/d voluntary cuts from eight member countries will continue into Q3 2024 but will start to be reversed in October at a rate of 0.18 MMBbl/d per month. OPEC+ members agreed on September 5 to delay a planned gradual 2.2 MMBbl/d supply hike by two months, shifting the start to December. The group will add 0.19 MMBbl/d in December and 0.21 MMBbl/d from January onwards, with an option to adjust or pause these hikes depending on market conditions. The cartel also reaffirmed its compensation cuts of 0.2 MMBbl/d per month through November 2025, as members such as Iraq, Russia, and Kazakhstan have struggled to meet their original production quotas.

AEGIS notes that the global crude market would quickly build inventories without OPEC's support in reducing supply.

OPEC Unwind. (Bearish, Mostly Priced in) OPEC+ opted for a smaller-than-expected production increase o, easing concerns that the group might accelerate its supply recovery into an increasingly fragile market. The alliance agreed to raise its collective quota by 137 MBbl/d for the month of November, continuing the gradual unwind of its 1.66 MMBbl/d voluntary cuts through early 2026.

China Demand. (Bearish, Priced In) China’s onshore crude inventories declined to 1.17 billion barrels this week, down from a record 1.20 billion barrels in mid-August, according to data from Kayrros. The draws came from commercial stockpiles, partially reversing the country’s earlier stockpiling surge, a key factor that has supported global oil prices even as the broader market faces record oversupply.

USD (Bullish, Priced In) The Federal Reserve cut its benchmark interest rate by 25 basis points, the first cut since December 2024, and signaled that another 50 basis point cut could be coming by then end of 2025. If markets expect rate cuts or looser monetary conditions, the dollar tends to weaken. Oil is priced in dollars, so a weaker dollar lowers the “real” cost of oil for buyers using other currencies. This often boosts demand at the margin and supports prices.

Ukraine-Russia Resolution. (Bearish, Surprise) Trump announced plans to meet with Russian President Vladimir Putin “within two weeks or so” to discuss ending the war in Ukraine, a development that could pave the way for additional Russian supply returning to market

Trade War. (Bearish, Mostly Priced In) There has been an increase in tit-for-tat trade tension between the US and China, with China sanctioning the US unit of Hanwha Ocean Co., a South Korean shipping major, and warned of additional retaliatory actions against the industry. However, President Trump said high tariffs on China were “not viable,” suggesting potential for de-escalation even as broader tensions remain elevated.

Projected Oversupply. (Bearish, Mostly Surprise) The IEA’s latest Oil Market Report projects global crude supply to outpace demand by nearly 4 MMBbl/d next year. The forecasted overhang is about 18% larger than last month’s estimate, reflecting OPEC+’s ongoing supply revival.

Trump/Iran/Venezuela. (Bullish, Surprise) The US government has sent several ships off the coast of Venezuela prompting speculation that the Trump administration may be seeking to push Venezuelan President Nicolas Maduro from power. Tensions rose after the US sent fighter jets to the Carribean after two Venezuelan military aricraft flew over an American naval vessel in the area.

Russian Supply. (Bullish, Surprise) Due to the latest sanction on Rosneft and Lukoil, analysts at Rystad Energy estimate 500–600 MBbl/d of Russian output could be curtailed, forcing Moscow to rely more heavily on shadow tanker fleets and Chinese buyers. However, the extent of any disruption remains uncertain, and it may take time to gauge how material the impact truly is.

Commodity Interest Trading involves risk and, therefore, is not appropriate for all persons; failure to manage commercial risk by engaging in some form of hedging also involves risk. Past performance is not necessarily indicative of future results. There is no guarantee that hedge program objectives will be achieved. Certain information contained in this research may constitute forward-looking terminology, such as “edge,” “advantage,” ‘opportunity,” “believe,” or other variations thereon or comparable terminology. Such statements and opinions are not guarantees of future performance or activities. Neither this trading advisor nor any of its trading principals offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program.