Oil heads for the biggest weekly loss since November amid talks of potential Gaza ceasefire

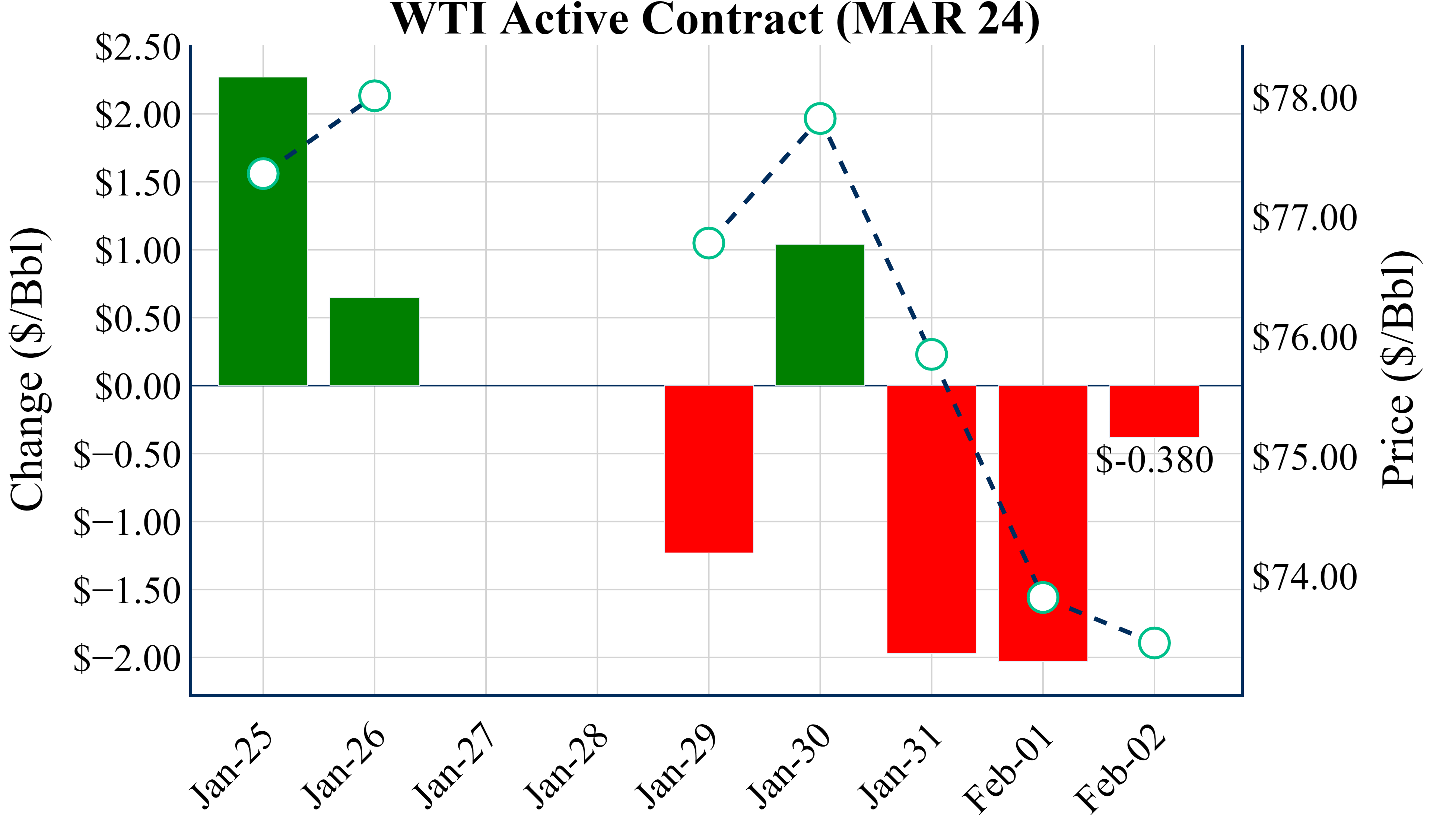

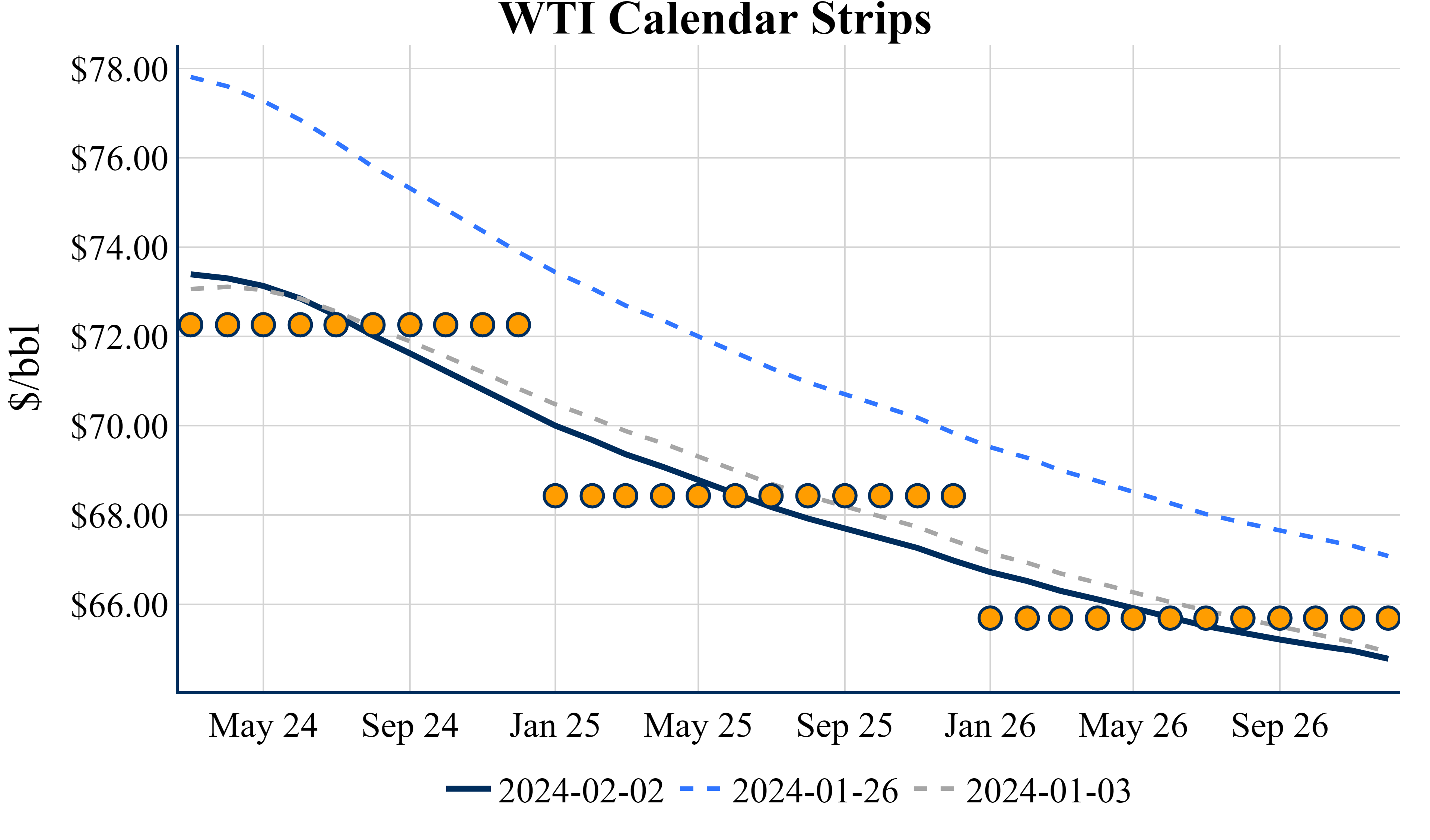

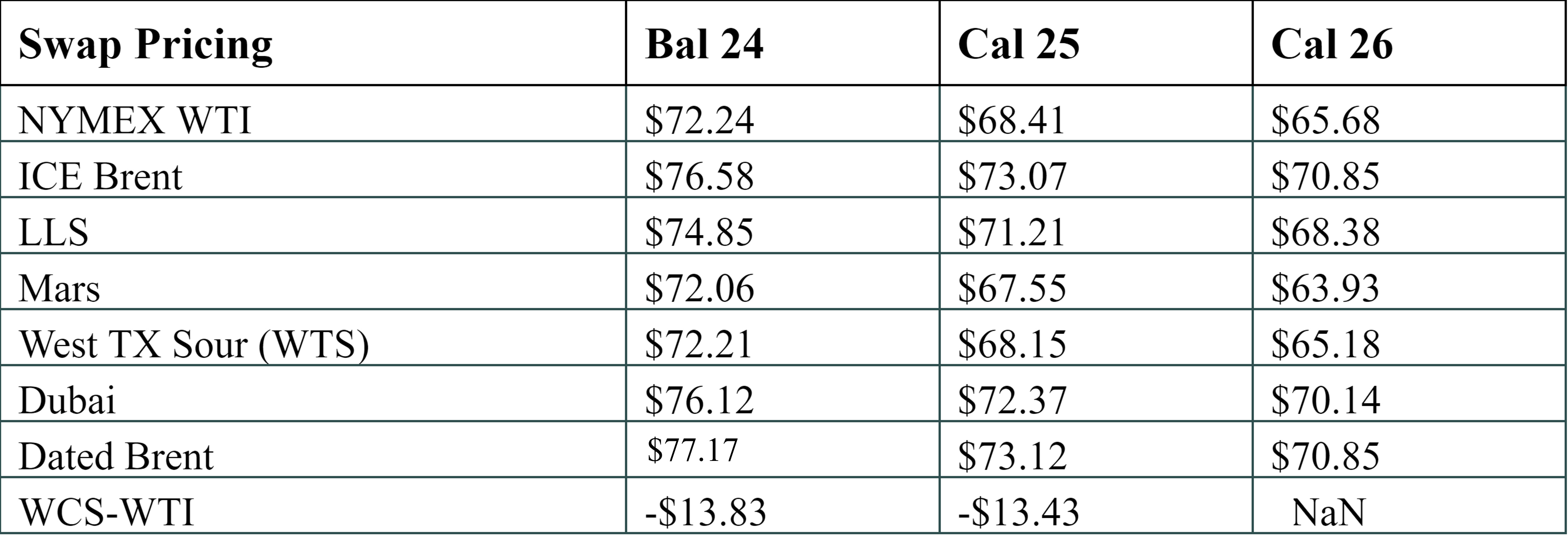

March ’24 WTI loses 42c this morning to trade around $73.40/Bbl

Crude finished lower by $2/Bbl yesterday amid reports of Israel agreeing to a ceasefire proposal, as reported by Al Jazeera

However, Al Jazeera deleted the tweet later amid ongoing peace talks between Israel and Hamas

Meanwhile, Bloomberg reported that Qatar presented Hamas with a proposal for a 45-day pause and the release of some Palestinian prisoners in exchange for Israeli hostages

Furthermore, BP shut down its 0.44 MMBbl/d Whiting refinery following an unexpected power outage yesterday, with no estimated timeline to restart

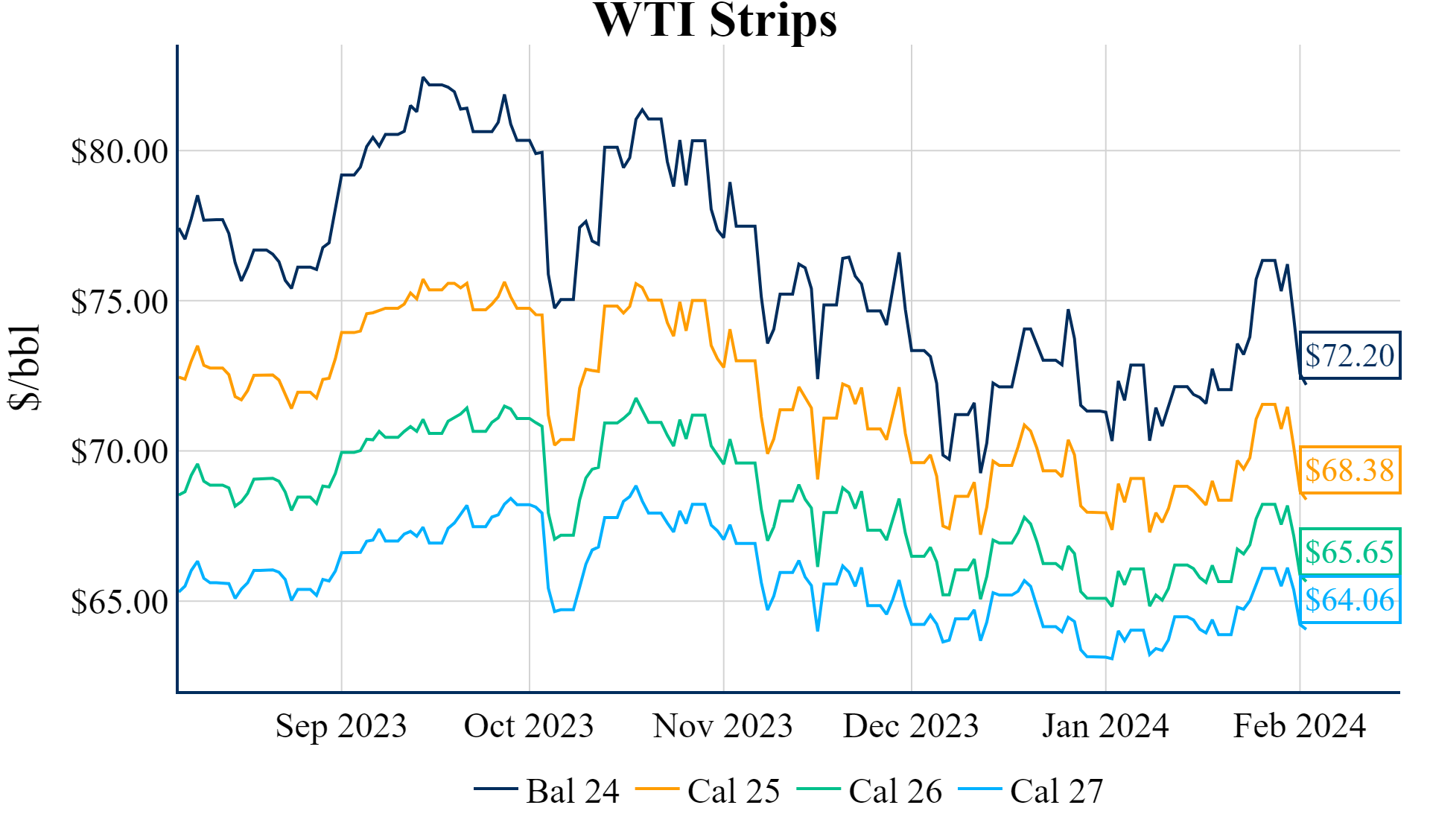

OPEC cuts start to kick in as the cartel looks to support oil prices (Bloomberg)

OPEC and its allies curbed oil production by 0.49 MMBbl/d in January to avoid a global surplus and support prices, reducing output to 26.57 MMBbl/d

Half of the OPEC production cut was from Iraq and Kuwait, with another 25% due to protests disrupting output in Libya

While leaving the policy unchanged for now, OPEC+ is set decide in early March on whether to extend production cuts into the second quarter, with Riyadh indicating that extension is “absolutely” possible

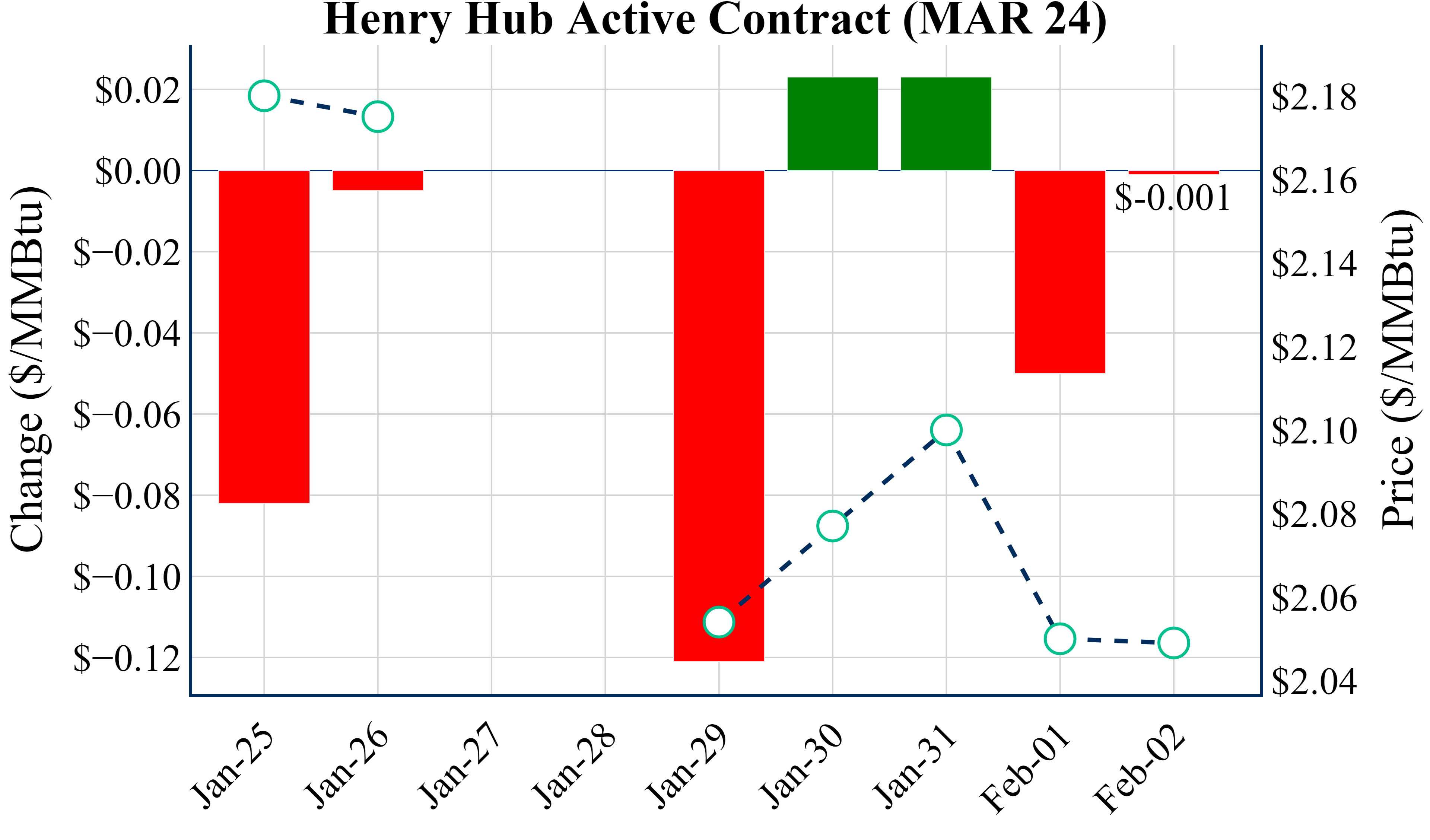

Natural gas prices trade lower amid near-term bearish weather outlook

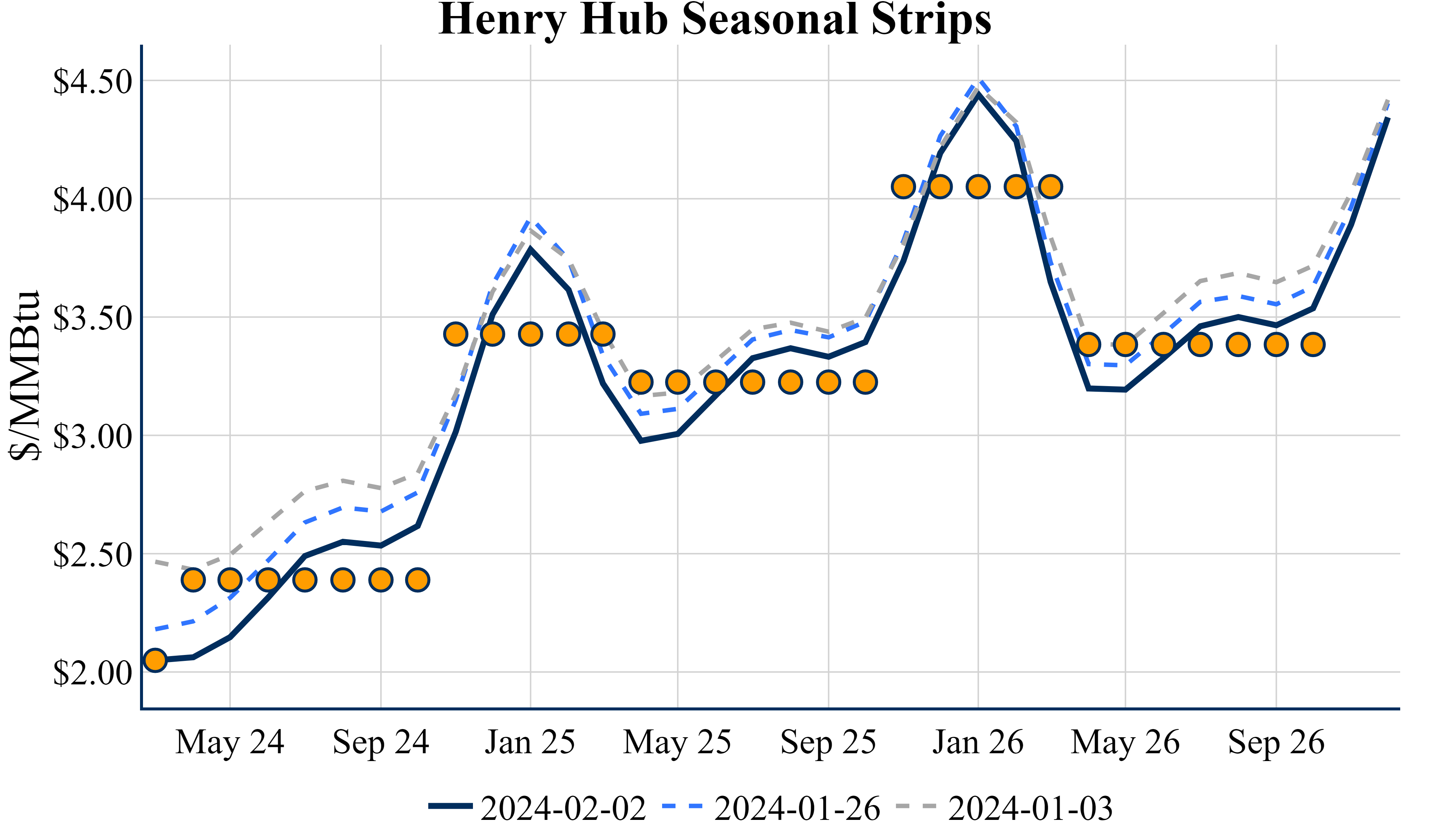

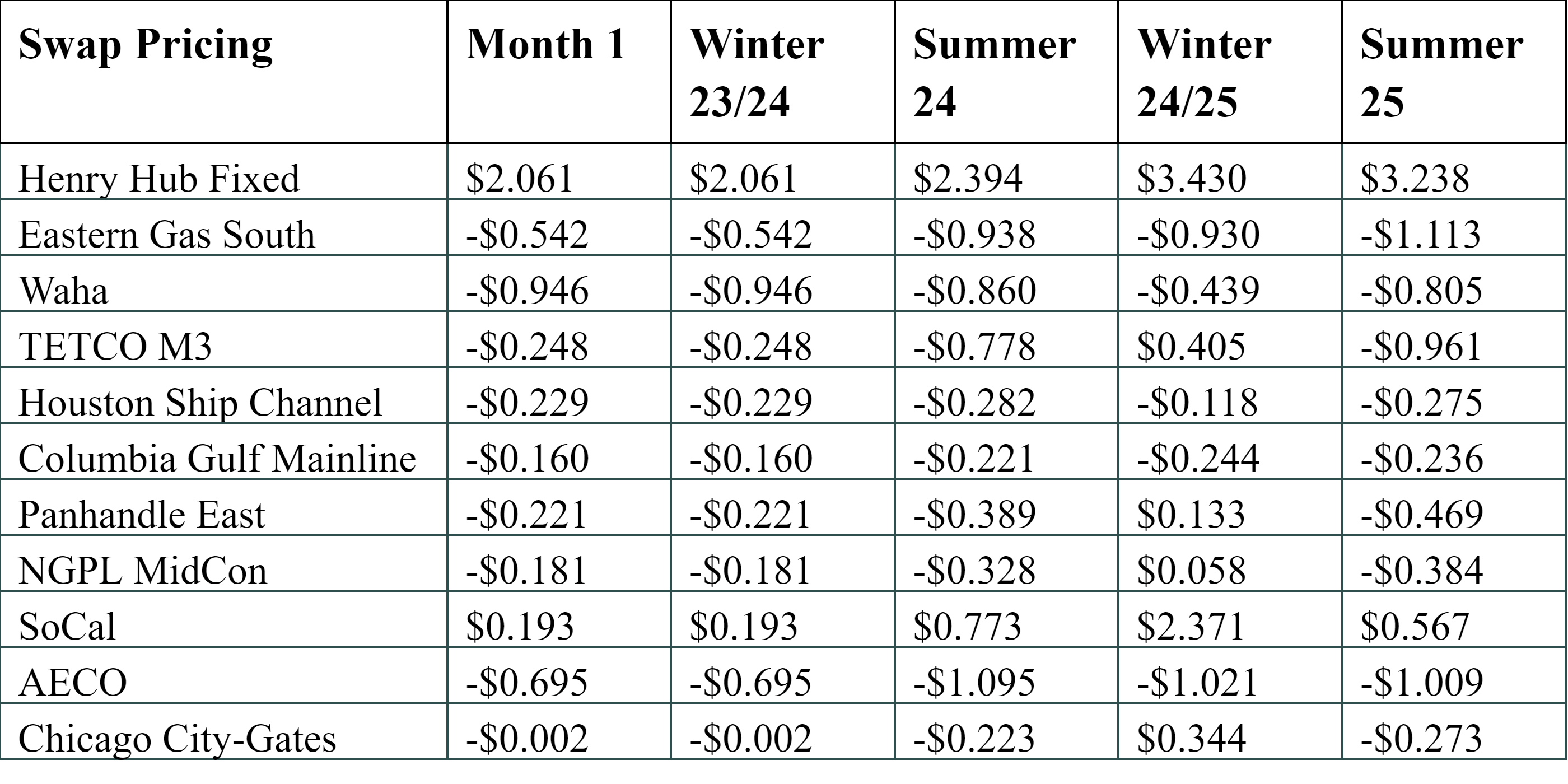

March ’24 Henry Hub is down 0.1c this morning to trade around $2.049/MMBtu

The Summer ’24 strip is down 2.1c to $2.374, and the Winter ‘24/’25 strip is down 1.5c to $3.413

Today's Euro Ens shows a dramatic shift, warming the Lower 48 by over +10o F, marking the warmest week since December with slightly cooler temperatures in the 11-15 day period

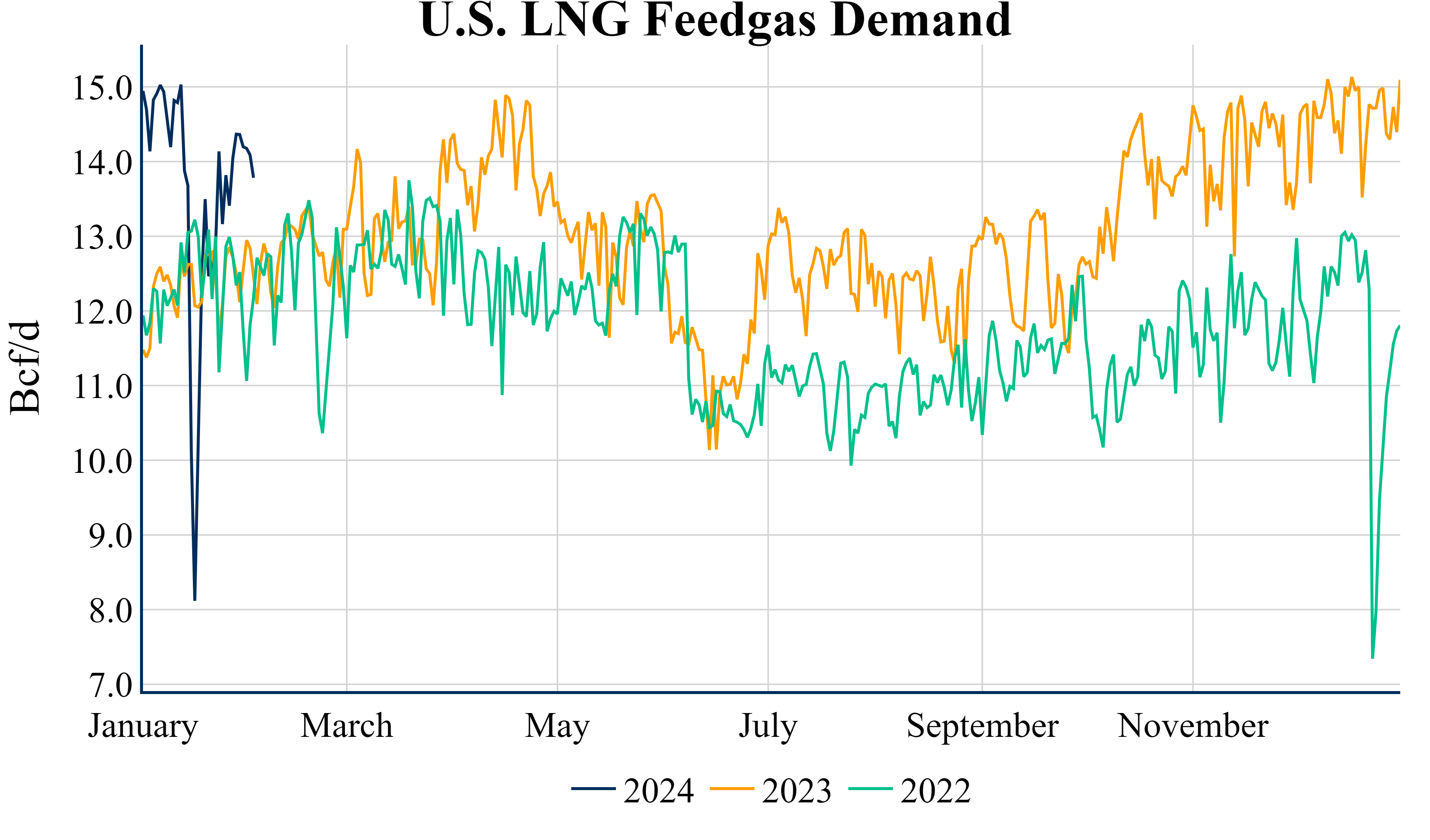

Lower 48 production rose by 0.93 Bcf/d, reversing early losses and achieving a net gain yesterday, reaching 103.8 Bcf/d with gains concentrated in the South-Central region (Criterion)

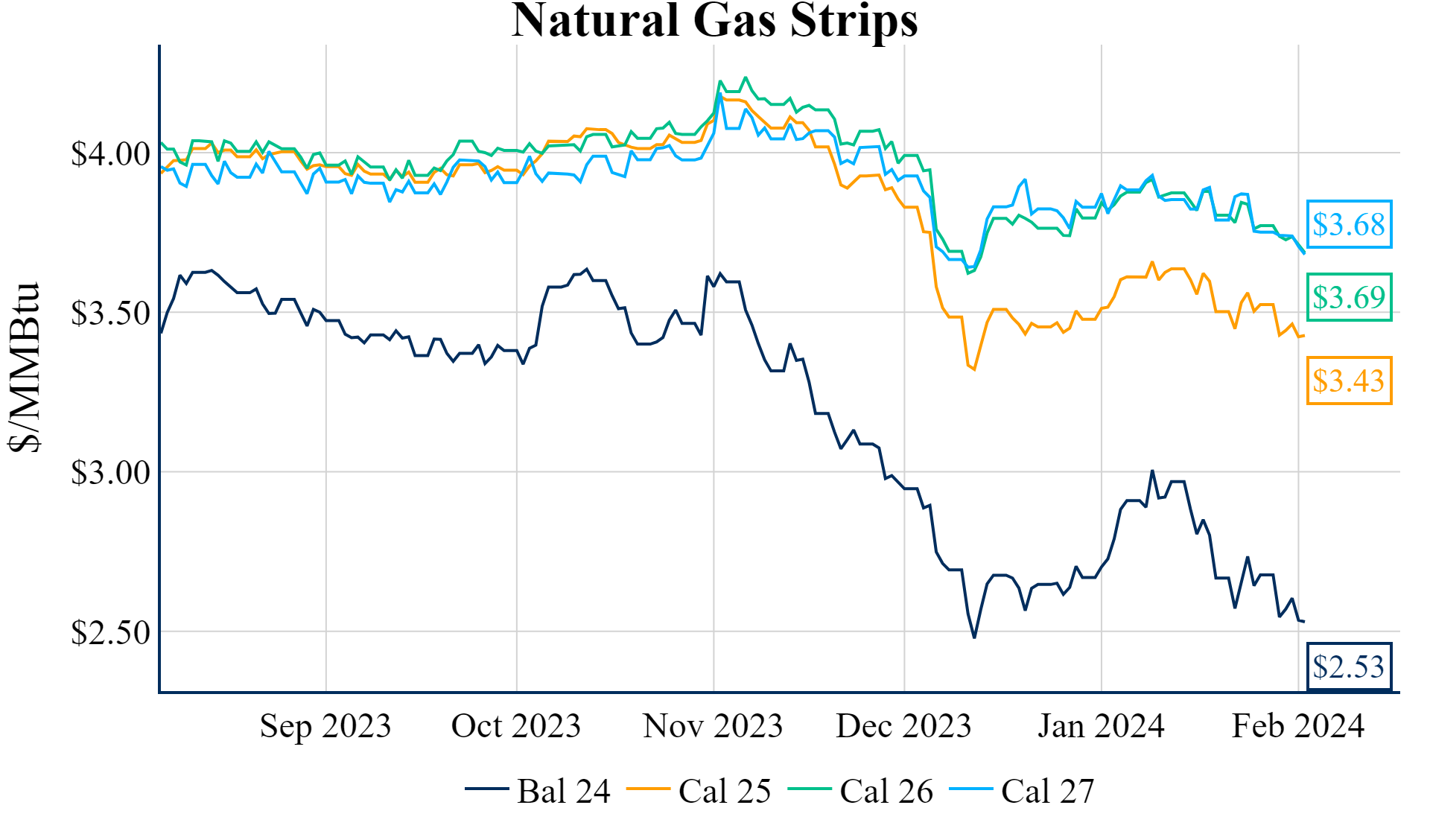

IEA sees China driving LNG demand growth amid various supply constraints (IEA, NGI)

Global natural gas demand is set to rise by 2.5% (100 Bcm) in 2024, led by Asia, Africa, and the Middle East, outpacing the 0.5% growth of 2023, driven by the industrial and ResCom sectors, said IEA in its Gas Market Report

LNG trade growth is expected at 3.5% (18 Bcm) for 2024, a decline from the 8% growth between 2016-2020, attributed to delays in liquefaction projects and feed gas availability issues

About one-fourth of the incremental supply is expected to come from the US and Mexico, less than previously forecasted due to the delay of Golden Pass Train 1 to 2025, added the bloc

China's LNG imports are projected to rise over 10%, with India, Bangladesh, and Pakistan also boosting imports due to falling domestic gas output and new power projects

The group expects Asian spot LNG prices to stay $1/MMBtu above European rates in 2024, with demand growth and supply constraints expected to cause significant price volatility

Get market insights delivered to your Inbox every day!