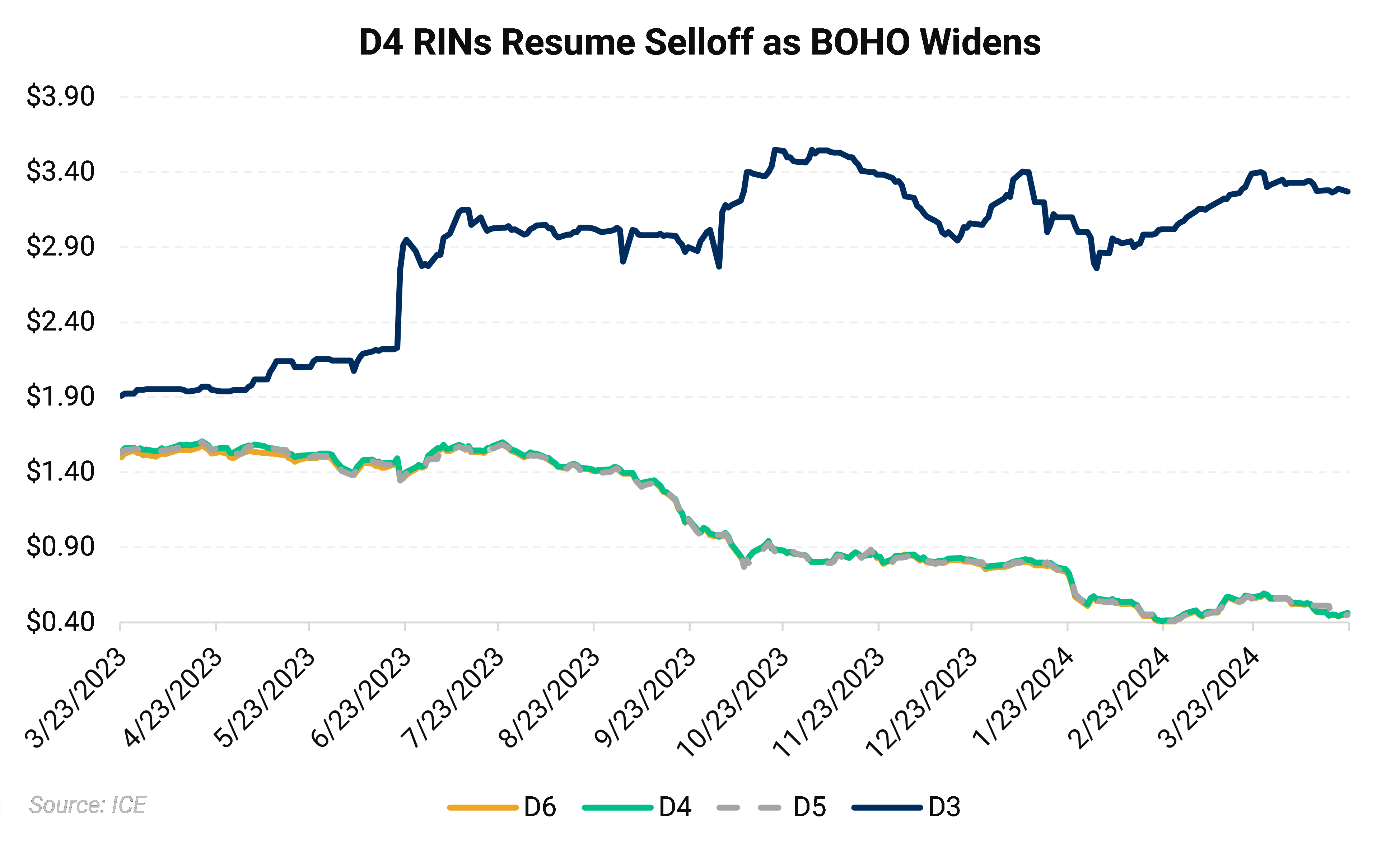

RIN prices resumed their decline in late-March/early-April as the BOHO spread shed 11% over the course of the month. Pronounced weakness in CBOT soybean oil by a strong Brazilian harvest and mounting US stockpiles saw the BOHO spread reach as low as $0.72/gallon. D4 prices shed 18% of their value from March 22 through April 22, reaching as low as 44.25c/RIN on April 19. The D4 market’s year-to-date losses widened to 41% from 26% the month prior. The D4/D6 spread widened to 25pt over the course of April, though often reached parity, or near parity intra-day.

D4 losses and soft diesel demand weighed on renewable diesel margins, with month-over-month losses averaging 11%. Soybean oil renewable diesel margins managed to increase 7% over the period on persistent feedstock weakness. Diesel prices peaked at $2.77/gallon in April before slumping to $2.54/gallon as US domestic demand reached the lowest seasonal level in 25 years. A narrower BOHO spread implies stronger biodiesel margins, which is bearish the D4 RIN all else equal.

The April 18 release of March 2024 RIN generation showed under 1.91 billion credits generated, down 6% from an upward-revised February total of 2.04 billion credits and down 12% from the December 2023 record of 217 billion credits. March total RIN generation was the lowest monthly output since January of 2024 and was down less than one percent on year-ago levels.

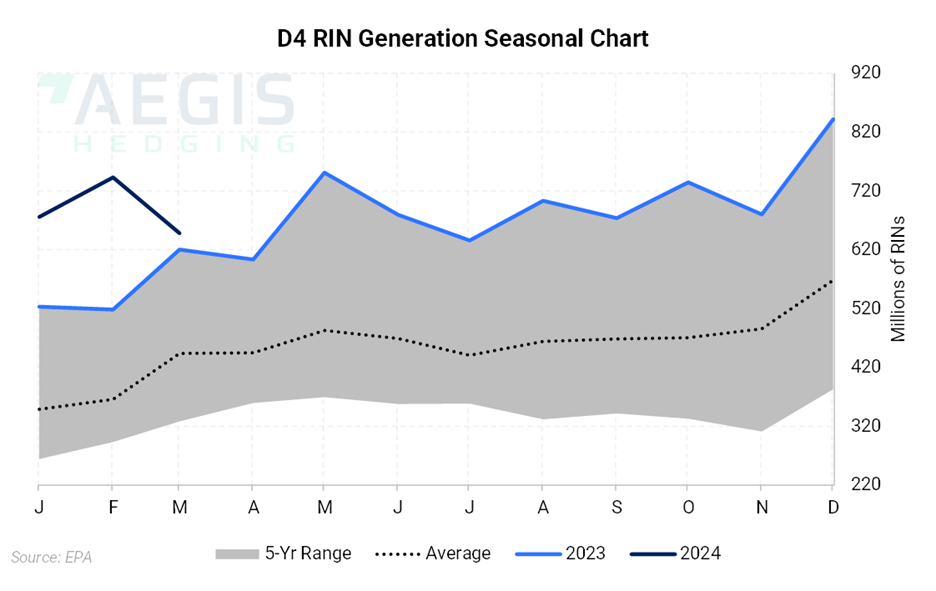

D4 generation tumbled 95 million credits, or nearly 13% from February levels, though was up 4.5% on year-ago levels. March D4 production marked the lowest level since September 2023 as maintenance, reduced runs, and increased renewable diesel exports weighed on D4 generation.

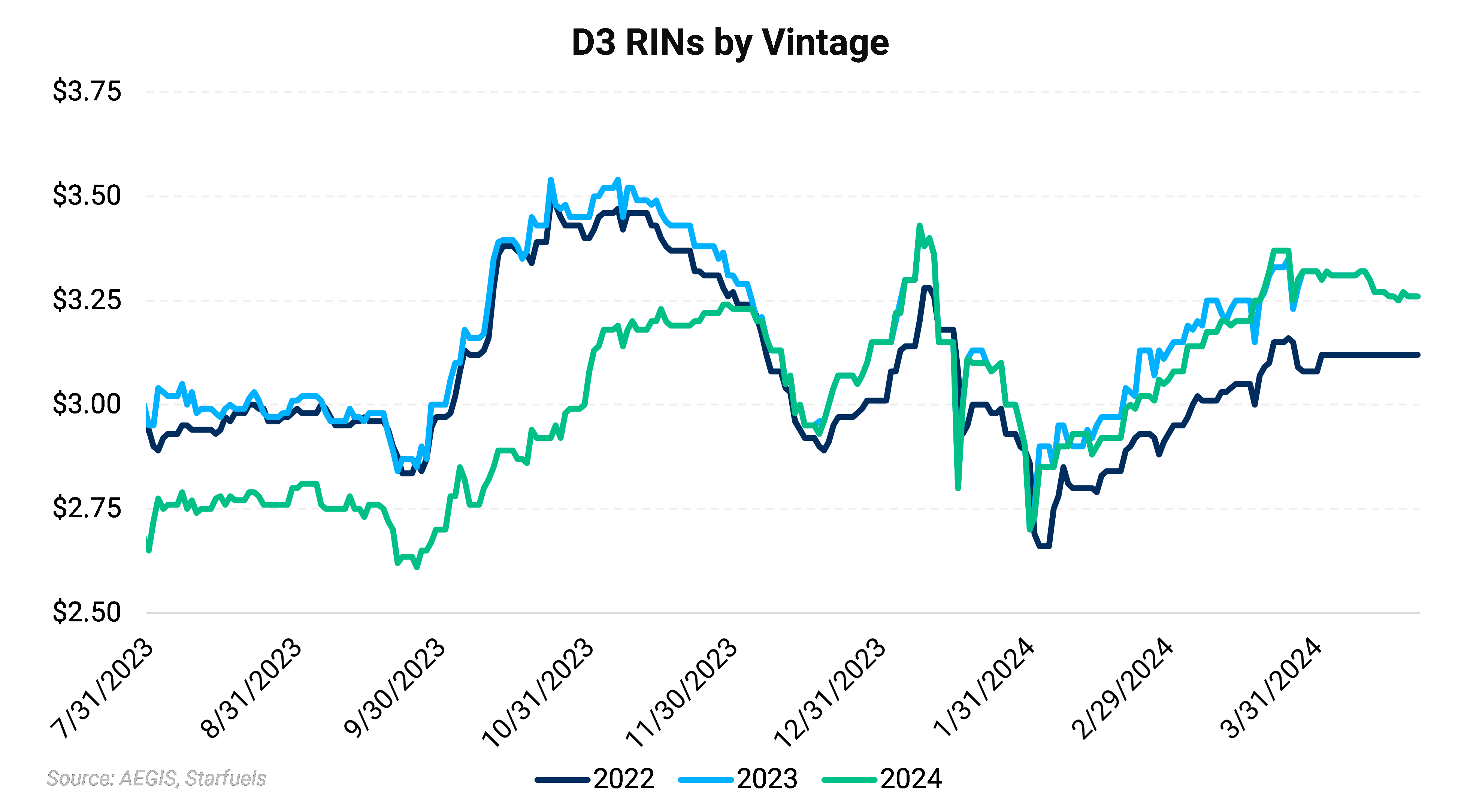

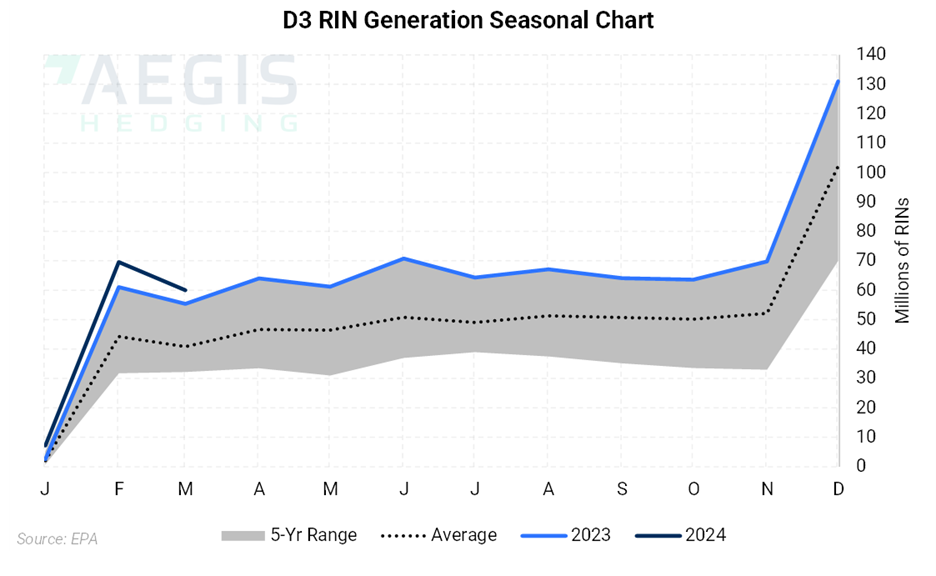

The D3 market saw more modest losses as production is falling well short of the 90.8MM credits/mo required to meet 2024 compliance. The absence of a cellulosic waiver credit should see the 2024 D3 continue to hold a $3 handle.

- March total RIN generation came in at just under 1.91 billion credits, down 6% from an upward-revised February total of 2.04 billion credits and down 12% from the December 2023 record of 217 billion credits. March total RIN generation was the lowest monthly output since January of 2024 and was down less than one percent on year-ago levels.

- D4 generation tumbled 95 million credits, or nearly 13% from February levels, though was up 4.5% on year-ago levels. March D4 production marked the lowest level since September 2023 as maintenance, reduced runs, and increased renewable diesel exports weighed on D4 generation.

- Domestic renewable diesel production accounted for 54% of total D4 output, up from 51% the month prior, yet down from 56% in January. Domestic renewable diesel production accounted for 54% of total D4 out in December. Foreign renewable diesel production made up just 7% of total D4 generation, down from 13% the month prior, and up from 6% in January. Domestic and imported biodiesel accounted for 37% of the March total, up from 36% in February and March. Over 9 million D4 credits were generated from domestic SAF production accounting for 1.4% of the March total. Foreign SAF production generated nearly 3.4 million credits after no foreign SAF was reported for February. January saw a record 15 million D4 credits were generated across domestic and foreign SAF production, accounting for 2.2% of the January total. March SAF production total 12.5 million D4 credits.

- D3 RIN generation came in at 60 million credits, down 14% from the month prior yet up 8.5%on year-ago levels. D3 generation came in under market expectations driving prices higher for just one session. The March generation number is representative of February production which typically posts the lowest number for the year given the shorter production month. Total 2023 cellulosic RIN production came in at 774.7 million credits, 65 million credits, or 7.7% short of the final cellulosic mandate. The EPA used an aggressive 25% growth rate to set the 2023 final cellulosic mandate.

- March RIN generation data house material upward revisions to both 2023 and 2024 D6 generation. Upward revisions for 2023 production totaled 2,269,107 and spanned June through December. February 2024 D6 RIN generation was revised higher by 3,917,340 credits. The prior month saw upward revisions to 2023 production totaling 6,464,450.

- Upward revisions to D4 generation totaled 19,285,686 credits spanning December 2022 through February 2024. Upward revisions for 2023 totaled 7,952,541 credits, or 41% of the total. Upward revisions for 2024 totaled 11,331,957, or 59% of the total. The month prior saw D4 generation revisions of just 77,466 credits spanning from November 2022 through January 2024.

- March RIN generation data housed modest upward revisions to 2023 and 2024 D5 production. Upward revisions for 2023 totaled 577 credits spread across the months of June and September. Upward revisions for 2024 totaled 1,144,029 credits, taking total revisions for the month to 1,144,606. The prior month’s data saw January 2024 D5 production revised higher by 2,751,635 credits, and March 2023 production up 3,545 credits.

- February 2024 D3 generation was revised higher by 7,268,555 to 69,557,227. The month prior saw January 2024 D3 generation revised up to 5,919,722 credits.

Calendar:

- March 31, 2024: EPA Deadline for 2023 Compliance

- Late Spring 2024: CARB Regulatory Proposal & Updated Modeling

- June 1, 2024: Attest Engagement Reporting Deadline for 2022

- March 31, 2025: EPA Expected Deadline for 2024 Compliance

Relevant News:

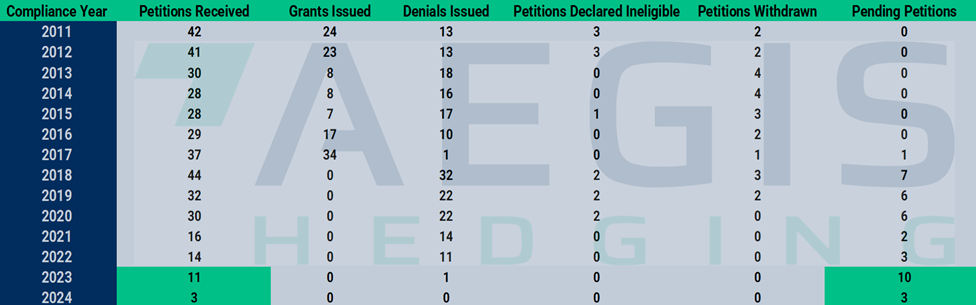

- The US Court of Appeals for the District of Columbia Circuit questioned the grounds for the EPA’s denial of small refinery waivers. At a hearing on April 16 of the Sinclair Wyoming Refining et al. v. EPA et al, judges requested the EPA to demonstrate that small refiners are able to pass on their compliance costs downstream, the cornerstone to the agency’s passthrough argument. Small refiners must demonstrate disproportionate economic hardship in order to qualify for SREs. The fresh arguments drove increased selling in RIN markets in the following sessions amid concerns that SRE approvals would decrease RIN demand.

- EPA issued a waiver allowing for the sale of E15 gasoline this summer, marking the third consecutive year for the continuation of the 15% ethanol blend. The agency pointed to supply disruptions related to the conflicts in the Middle East and Ukraine as justification for the waiver and noted that the move would not result in increased smog pollution. E15 sales are typically blocked from June through September due to RVP limitations.

- CARB is considering steeper 2025 step-downs of 7% or 9%, compared to an originally proposed 5% stepdown. The more stringent targets are aimed at managing a record supply of unused credits, which will continue to grow well into 2025. CARB maintained a 30% reduction target for 2030 and 90% target for 2045 at its April 10 public workshop, unchanged from the board’s December 2023 proposal. CARB also modeled a scenario in which the auto-acceleration mechanism was triggered twice, resulting in a drawdown of 170MM credits. CARB is considering sustainability guardrails as well as requiring an independent feedstock certification process. Stakeholders urged CARB to pursue the most aggressive 9% stepdown and displayed a preference for the program to be managed through more precise targets, relying less on the AAM for ease of planning and to drive investment.

- EIA trimmed its 2024 and 2025 forecasts for domestic RD output and demand. US RD production for 2024 was cut by 1% to 2016 Bbl/d, according to the latest Short-Term Energy Outlook. Production for 2025 was trimmed by 0.3% to 289,000 Bbl/d. EIA cut its 2024 RD consumption forecast by 1.2% to 239,000 Bbl/d, while the 2025 outlook was trimmed 0.3% to 305,000 Bbl/d. EIA expects 2024 net exports of 25,000 Bbl/d, up 1.2% from the previous month’s STEO. Net exports for 2025 were raised 6.3% to 17,000 Bbl/d. Biodiesel production is set to average 99,000 Bbl/d in 2024 and 88,000 Bbl/d in 2025 against consumption forecasts of 106,000 Bbl/d and 83,000 Bbl/d, respectively.

- EPA denied the American Petrochemical & Fuel Manufacturers’ (AFPM) petition for a partial waver of the 2023 cellulosic compliance year. The agency cited sufficient D3 RIN supply using carryover RINs and carrying deficits to comply with the 2023 obligation and dismissed AFPM’s claim of severe economic harm. EPA estimated 2023 D3 generation of 775MM credits and 75MM 2022 carryover RINs against an obligation of 850MM. EPA did not account for greater RIN demand resulting from SRE approvals in its March 15 response.

- GREET guidance has been delayed by a few weeks as the new greenhouse gas model awaits approval from the Treasury Department, USDA head Tom Vilsack said on March 1, according to Argus Media. The Biden administration was supposed to announce new guidance by March 1, with industry hopes pinned on a viable pathway for corn-based ethanol-to-SAF. Vilsack confirmed the model would be used to determine emissions for ethanol-to-SAF, according to Argus Media. The adjustment to the Department of Energy’s GREET model aims to ensure crediting for farming practices which reduce environmental impact like cover crops and no-till farming.

- The 5th US Circuit Court of Appeals turned down a request to reconsider its November 22, 2023, decision to block SRE denials for six small refineries. Biofuel industry groups Growth Energy and Renewable Fuel Association sought a rehearing on the grounds that the denials should be brought before the DC Circuit Court. The EPA has received 12 SRE petitions since the 5th Circuit’s November ruling.

- PBF reported 12,000 BBl/d of RD production during the fourth quarter 2023, down from 17,000 Bbl/d in the third quarter due to a catalyst change. St. Bernard Renewables (SBR) is a 50:50 joint venture with Italian major ENI located at PBF’s Chalmette, Louisiana, refinery. The facility has a nameplate capacity of 20,000 Bbl/d, meaning SBR was running at just 60% of capacity during the fourth quarter.

- Chevron REG is closing two biodiesel facilities indefinitely citing poor market conditions. The 2,000 Bbl/d Madison, Wisconsin, facility and 3,000 Bbl/d Ralton, Iowa, plant come as renewable diesel and biodiesel production has outpaced mandate volumes established by the EPA’s 2023-2026 ‘Set Rule.’ The resulting deterioration in the margin environment was bound to lead to closures of less economic biodiesel producers. RD producers earn 1.7 D4 RINs per gallon compared to 1.5 D4 RINs per gallon for BD. The Madison, Wisconsin, facility is scheduled for mid-April 2024 closure.

- Diamond Green Diesel’s Q4 operating income fell by 68% amid lower RD margins. RD sales averaged 3.8MM gal/d in Q4 2023, up 52% from the same period last year. Valero said its 470MM gal/y Port Arthur SAF expansion is on schedule for completion by Q1 2025.

- The 5th US Circuit Court of Appeals turned down a request to reconsider its November 22, 2023, decision to block SRE denials for six small refineries. Biofuel industry groups Growth Energy and Renewable Fuel Association sought a rehearing on the grounds that the denials should be brought before the DC Circuit Court. The EPA has received 12 SRE petitions since the 5th Circuit’s November ruling.

- The US Court of Appeals for the 11th Circuit dismissed a SRE challenge by Hunt Refining on January 11, saying the case should be heard by the US Court of Appeals for the DC Circuit. Biofuel industry group Growth Energy welcomed the decision as CEO Emily Skor responded “EPA’s denials of these SRE petitions were ‘nationally applicable’ and have nationwide effect, and challenges to the denials should only have been brought in the DC Circuit.”

- The 5th US Circuit Court of Appeals ruled to block denials of SREs for six refineries on November 22, 2023. The SREs cover Calumet’s 57,000 Bbl/d Shreveport, Louisiana refinery, Placid Refining’s 75,000 Bbl/d Port Allen, Louisiana refinery, Ergon Refining’s 26,500 Bbl/d Vicksburg, Mississippi refinery, Ergon’s 23,000 Bb/d West Virginia refinery, CVR’s 74,500 Bbl/d Wynnewood, Oklahoma refinery, and Allegiance Refining’s 21,000 Bbl/d San Antonio refinery. The court’s decision said the EPA’s blanket SRE rejection was “impermissibly retroactive; contrary to law; and counter to the record evidence.” The decision will add a bearish undertone to an already oversupplied marketplace, save for D3 credits.

- Federal judges defended the EPA’s approach to setting the 2020-2022 blending mandates. US refiners have complained blend requirements were too high based on how the EPA adjusted blending targets to account for projected Small Refinery Exemptions (SREs). The EPA is also facing a separate lawsuit for its 2022 cellulosic biofuel requirement, with biofuel groups arguing that targets were set too low based on projections of actual production and not accounting for the availability of carryover credits for compliance. Refiners have also filed a series of lawsuits in the DC Circuit court challenging the EPA’s move to reject all outstanding SREs this year.

RIN prices resumed their decline in late-March/early-April as the BOHO spread shed 11% over the course of the month. Pronounced weakness in CBOT soybean oil by a strong Brazilian harvest and mounting US stockpiles saw the BOHO spread reach as low as $0.72/gallon. D4 prices shed 18% of their value from March 22 through April 22, reaching as low as 44.25c/RIN on April 19. The D4 market’s year-to-date losses widened to 41% from 26% the month prior.

D4 losses and soft diesel demand weighed on renewable diesel margins, with month-over-month losses averaging 11%. Soybean oil renewable diesel margins managed to increase 7% over the period on persistent feedstock weakness. Diesel prices peaked at $2.77/gallon in April before slumping to $2.54/gallon as US domestic demand reached the lowest seasonal level in 25 years. UCO remained the strongest returning feedstock at $1.79/gallon as of April 22, followed by BFT at $1.23/gallon. SBO margins reached as high as $1.25/gallon earlier in the month, the highest margins have stood since mid-February. High spot DCO prices continue to pressure DCO margins, which came in at $1.18/gallon.

The BOHO spread narrowed to $0.72/gallon, marking the lowest level in nearly a month and a half as losses in the front-month soybean oil contract surpassed renewed weakness in diesel values.

RIN markets proved responsive to a widening BOHO spread, yet SRE fears sparked heavier selling in the third week of April. This saw the spread between renewable diesel-generated RINs and the BOHO spread inverted to -3.5c, after averaging a +2.8c premium month-to-date, indicating the 2024 credit is making brief forays into oversold territory. A narrower BOHO spread implies stronger biodiesel margins, which is bearish the D4 RIN all else equal.

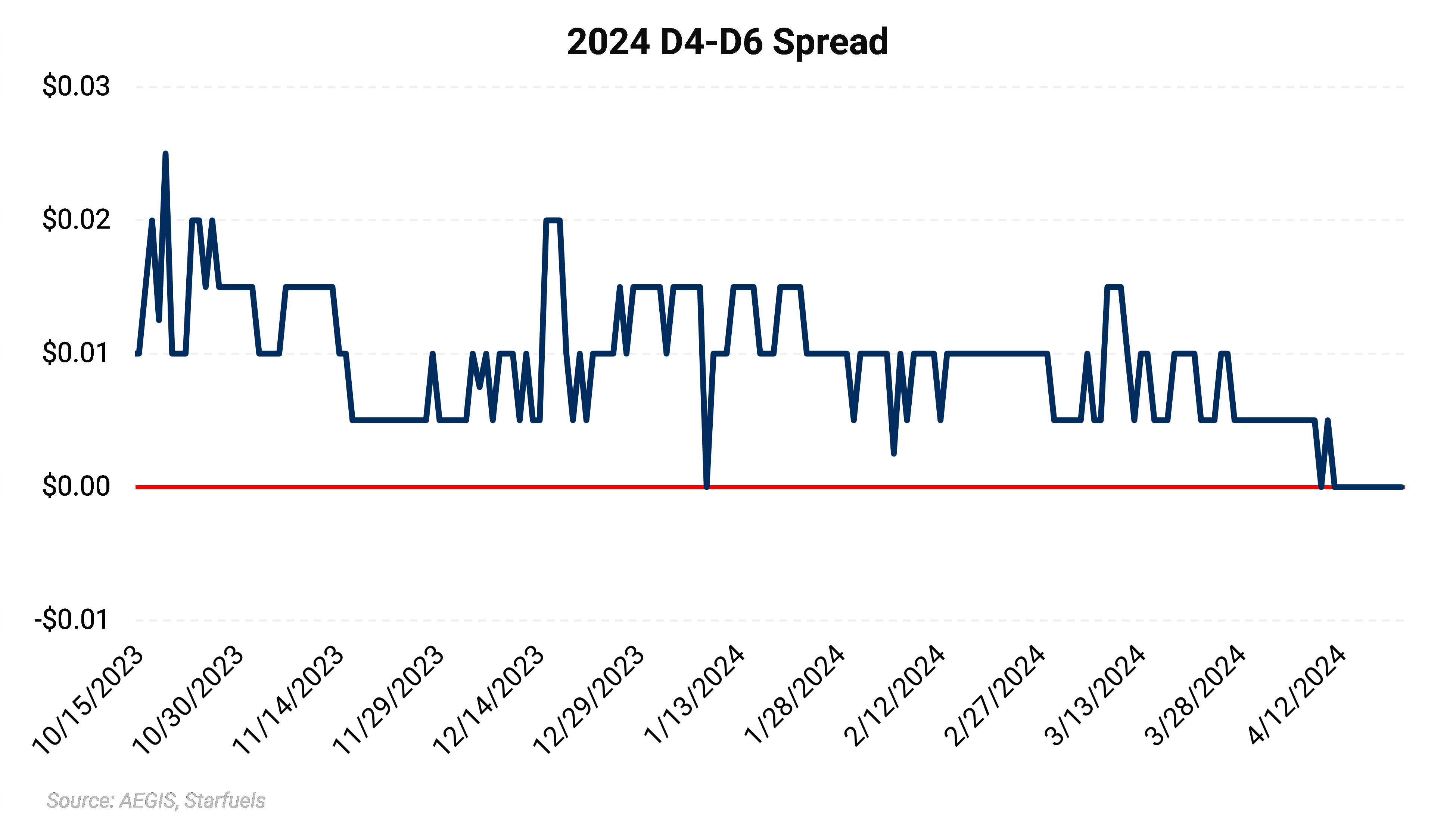

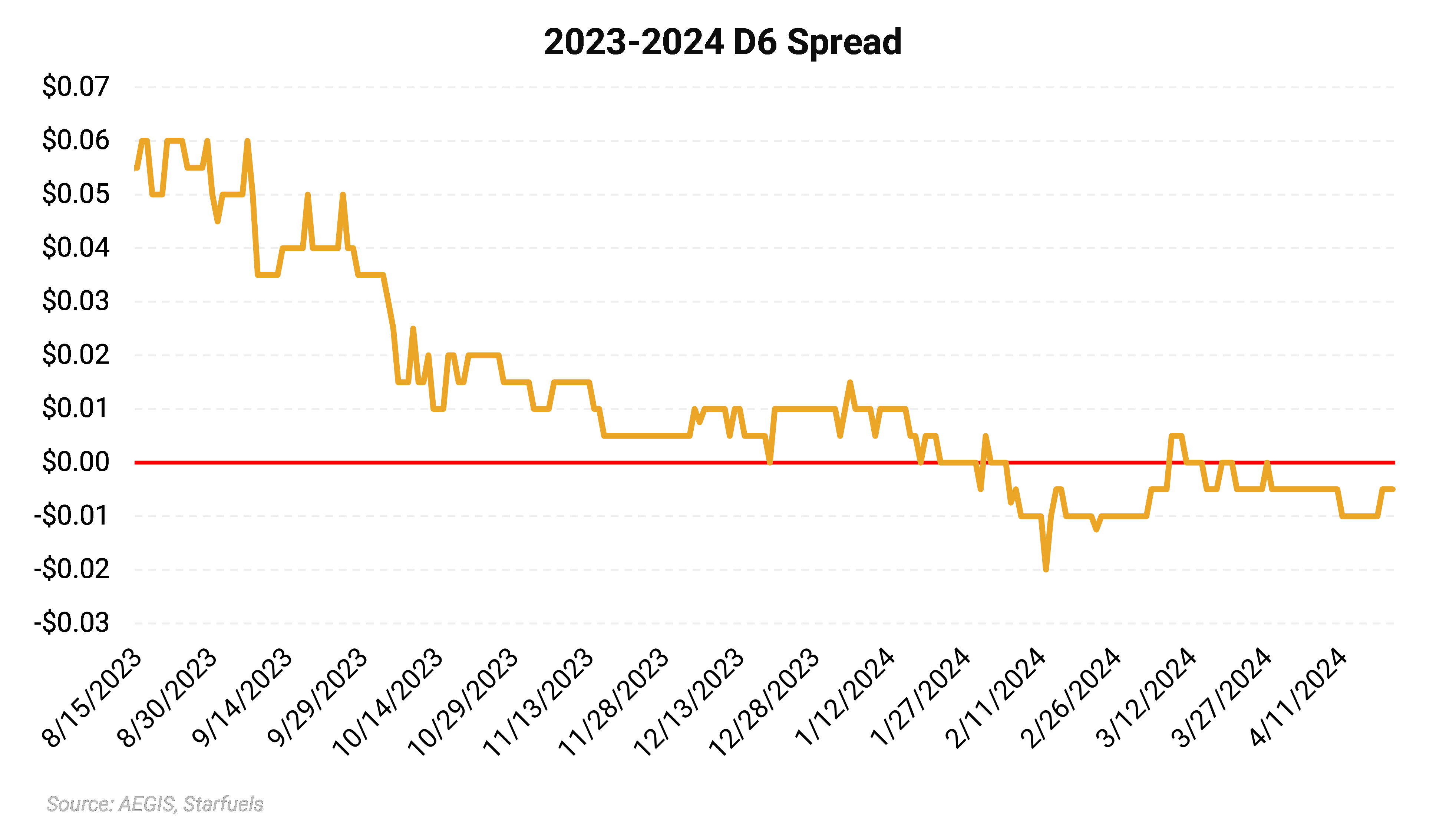

The D6 market continued to take its cues from the D4 market as the biomass-based diesel credit serves as the principal credit of compliance under the RFS. The D4/D6 spread widened to 25pt over the course of April, though often reached parity, or near parity intra-day. We believe D4 RINs have been holding premium to D6 despite relative oversupply of D4 credits due to the added value for the D4 RIN to fulfill multiple obligations relative to the D6 RIN which can only meet the renewable fuel requirement. The lack of a supplemental standard for 2024 and 2025 compliance is also bearish the D6 relative to the D4.

A narrower D4/D6 spread indicates tightness in D6 supply. In the absence of a sufficient supply of D6 credits, D4 and D5 credits from the advanced category can be used to satisfy compliance obligations.

We believe the recent widening of the D4/D6 spread indicates recent concerns that SRE approvals would have outsized bearish impacts on the D6 credit relative to other D categories. The recent approval of summer E15 sales is also bearish the D6 credit all else equal.

In recent issues we indicated that a shortfall in 2023 D6 RINs should drive the 2023 D4/D6 spread to trend toward parity which was proved true by late March. We see this dynamic carrying over into the 2024 vintage marketplace, particularly later in the year as renewable diesel production and imports increase.

The D3 market posted modest losses as the 2024 vintage marketplace remains tightly supplied. The 2024 market traded as high as $3.40/RIN following the March 15 EPA denial of AFPM’s partial waiver request for the 2023 cellulosic biofuel requirement. The move will require some obligated parties to carry forward 2023 cellulosic deficits into the 2024 compliance period, increasing demand for 2024 vintage credits.

The C23/C24 spread narrowed to flat from -4c/RIN the month prior, indicating both 2023 and 2024 D3 supply is tight. The spread held a +5c/RIN premium prior to the March 15 waiver denial.

Total 2023 D3 and D7 RIN generation stands at 774.9 million credits, or 7.75% short of the 840-million-gallon mandate. With no Cellulosic Waiver Credit in place and a record low RIN bank, we continued to expect 2024 D3 RINs to remain at elevated levels—above the $3.00/RIN mark.

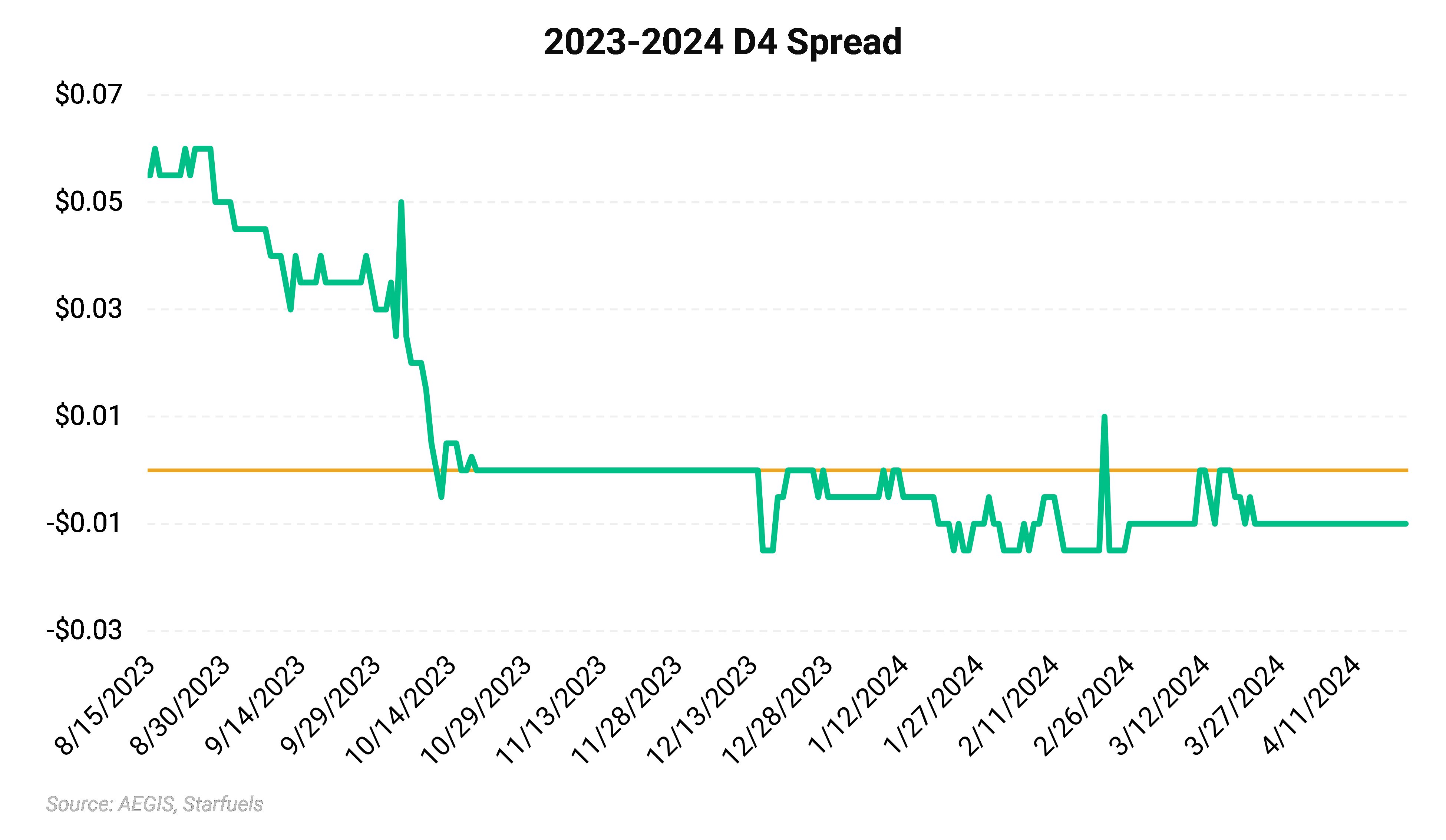

The 2023-2024 D4 RIN spread remained inverted as the deadline for 2023 compliance passed and trade for the prior year vintage credits slowed.

AEGIS noted in earlier reports that diesel would be the main driver of credit markets as RINs are the most responsive component of the credit stack for buttressing renewable diesel margins.

Heavy soybean oil losses have seen biodiesel margins recover off the lowest levels in nearly four months, with SBO renewable diesel margins rebounding off the lowest levels since June 203. Chevron REG recently announced the April 2024 closure of two of its biodiesel facilities citing poor market conditions.

We anticipate heavy production from both the RD and BD industry throughout 2024 despite worsening margins as producers strive to take advantage of the final year of the blenders tax credit (BTC). AEGIS has turned cautiously bullish on diesel as persistent tight supply conditions, geopolitical risk, and forward crude strength are facing historically low US demand, increased global refining capacity, and flagging global demand.

We expect RIN generation to remain at elevated levels as long as feedstock pricing remains under pressure from imports and diesel markets remain tight. First half 2024 startups are planned to run at half capacity and should start to pressure RIN markets more materially in the second half of the year.

Recent diesel weakness and an underperforming D4 market led producers to trim runs, conduct maintenance, and even saw the permanent closure of two biodiesel facilities. Renewable feedstock imports notably slowed during late February and early March yet resumed at normal levels in April.

On the renewable diesel side, the RIN spread to BOHO stood at +2.8c, up from +1.75c the month prior. The spread inverted during the third week of the month to as low as -4c/RIN as SRE concerns drove heavier selling. We have noted an increased correlation between renewable diesel-generated RINs and the BOHO spread since the start of March. Despite renewed declines in renewable diesel margins, SBO margins have returned from the brink of break-even levels as a robust Brazil harvest and increasing US stockpiles weighed heavily on SBO pricing.

Biodiesel economics showed signs of improvement as the spread between biodiesel-generated RINs and the BOHO narrowed to -7.25c on average from -15c the month prior. At these levels, returns for non-integrated producers rebounded to $0.37/gallon from $0.33/gallon the month prior, according to AEGIS estimates. Returns for integrated producers stood at $0.56/gallon during the first three weeks of April.

At current UCO pricing, D4 credits would have to tumble more than 30c/RIN to shut in UCO renewable diesel production.

Under prevailing conditions, we see D4 RINs as short-term underpriced relative to SRE concerns and medium term overpriced to reflect the margin environment and the return of producers from downtime. With renewed production we see room for losses of at least 7c/RIN. Resurgent diesel strength would carve out more room for losses.

The 2023-2024 D6 spread spent the bulk of the month wavering between -5pt and -10pt, widening from near parity seen the month prior as the passing of the 2023 compliance deadline saw diminished interest in prior year vintage credits.

EPA RIN Generation Data as of April 18:

EPA Small Refinery Exemption (SRE) Data as of April 18:

Green indicates change

Some of the price and regulatory risk in the development of the renewable fuels markets is controllable through hedging or pre-selling. Other risks require constant monitoring of pending changes to regulations and programs. AEGIS can help with both.

Interested in receiving these updates directly to your inbox?