Latest Insight

Last Look: Oil snaps its two-week losing streak, finishing $1.63 higher this week

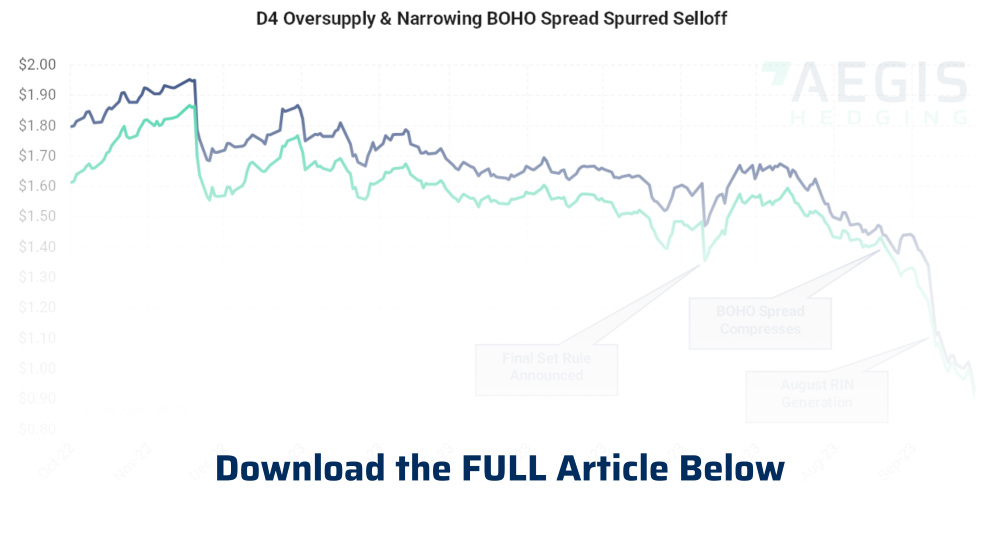

RIN markets gapped lower over the past three weeks as a mounting supply glut of biomass-based diesel credits saw prompt D4 prices fall to the lowest levels in over three years.

The release of August RIN generation data showed D4 output covered more than 98% of the total 2023 advanced biofuel mandate, spurring heavy selling. Diesel strength and weakness in soybean oil futures piled onto already bearish sentiment, stoking fears that RINs could plummet to tenths of cent.

D4 credits sold off more than 30c/RIN, or 28%, since the September 21 release of the August RIN generation data, reaching as low as 76c/RIN on October 10.

The following day, October 11, saw both D4 and D6 credits recover more than 9% with trades between 81.5c and 83c/RIN.

And so, the RIN rout took a breather as traders took a bit of diesel weakness as an opportunity to evaluate the landscape. What did they see?