Latest Insight

Last Look: Oil snaps its two-week losing streak, finishing $1.63 higher this week

To quickly access the page content, please click on the links below:

|

|

||

|

|

||

|

LCFS Spot Contract |

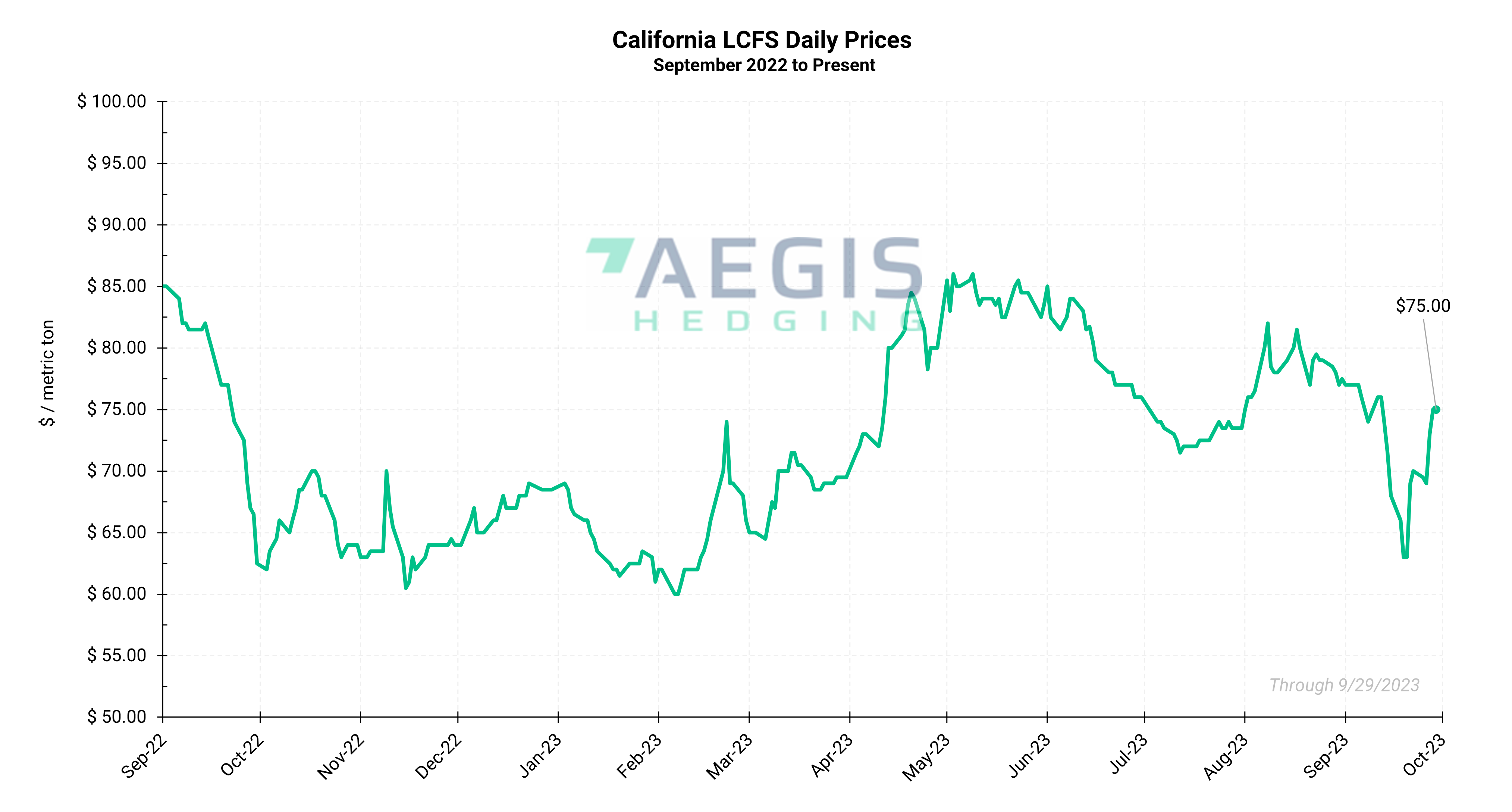

California LCFS |

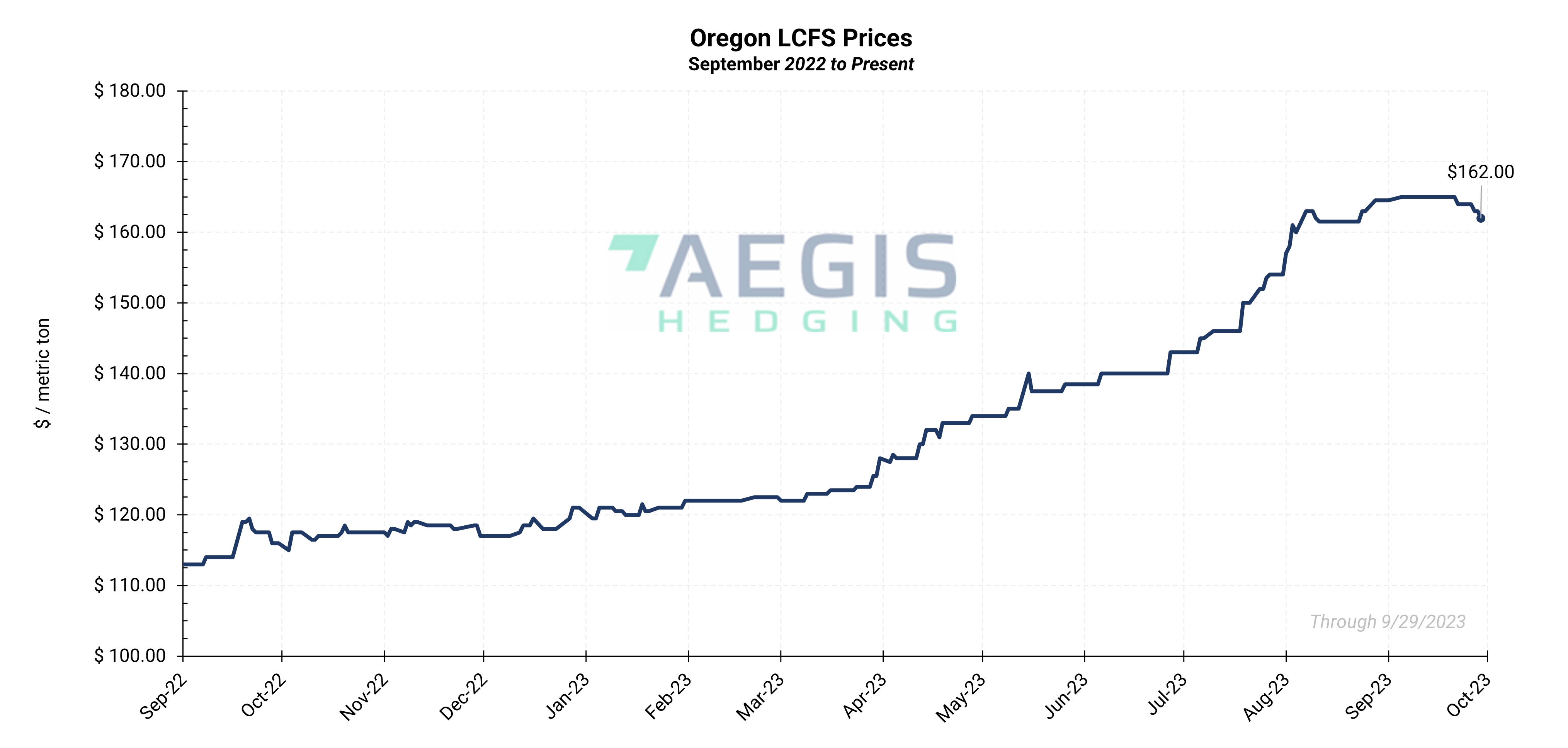

Oregon LCFS |

|

Price September 29th, 2023 |

$ 75.00 |

$ 162.00 |

|

Avg. Weekly Price September 25th - September 29th, 2023 |

$ 72.30 |

$ 163.20 |

|

Average Monthly Price September 2023 |

$ 71.85 |

$ 164.48 |

|

|

|

|

|

LCFS Futures Contract |

Pricing |

|

|

Dec. '23 |

$ 77.25 |

|

|

Dec. '24 |

$ 81.25 |

|

|

Dec. '25 |

$ 88.95 |

|

The California Low Carbon Fuel Standard (LCFS) market recovered as a public, non-voting board meeting spurred buying. Materials provided showed CARB is considering a 30% reduction scenario with a 5% step down in 2025. A 25% reduction scenario with limitations to biodiesel use was considered but found to not displace enough fossil fuel. A 35% reduction scenario was also considered but found to be too costly.

Prompt credits rebounded $6.1/t, or 9.2%, to average $72.30/t. The market closed out the week at $75.00/t, up from last week’s low of $63.00/t; the lowest level since February 2023.

The forward structure maintained a $1/credit contango heading into 2024.

The prompt market had been in a choppy holding pattern since early May yet initiated a material downtrend starting in early June. LCFS strength has been driven by trader buying and strength in futures markets as the credits become more attractive options ahead of CARB’s more stringent scoping plan.

CARB released a proposal ahead of its rulemaking which adopted a 30% carbon intensity reduction by 2030, curbed biogas contributions, and included an auto-acceleration mechanism. Traders now await the late-September board meeting for the next cues and the release of the final proposal for the state’s scoping plan.

During the August 16 workshop, California’s Air Resources Board (CARB) provided updated guidance on the timeline for its rulemaking process to usher in more stringent carbon intensity targets. The regulator aims to release a proposal after a late-September board meeting during which a non-voting LCFS item will be outlined. The proposal will face a 45-day public comment period allowing the item to be voted on at a board meeting in early 2024.

The new targets could come into effect by mid-to-late 2024, or CARB could wait till January 1, 2025. CARB clarified that it would not retroactively apply the ruling to any part of the 2024 compliance year.

The August 16 public workshop covered extensive modeling updates to its California Transportation Supply Model (CATS). The updated scenarios included material upward revisions in electrification of HDVs and MDVs, added in total out-of-state biomethane supply and built in a credit bank drawdown pathway. CARB did not factor alcohol-to-jet into the model as sufficient data was not available.

Stakeholders raised concerns that the electricity CI used in the model was too high and took issue with using total out-of-state biomethane (RNG) in the model, while not adjusting for out of state competition and restrictions.

|

||||

|

RIN Spot Contract |

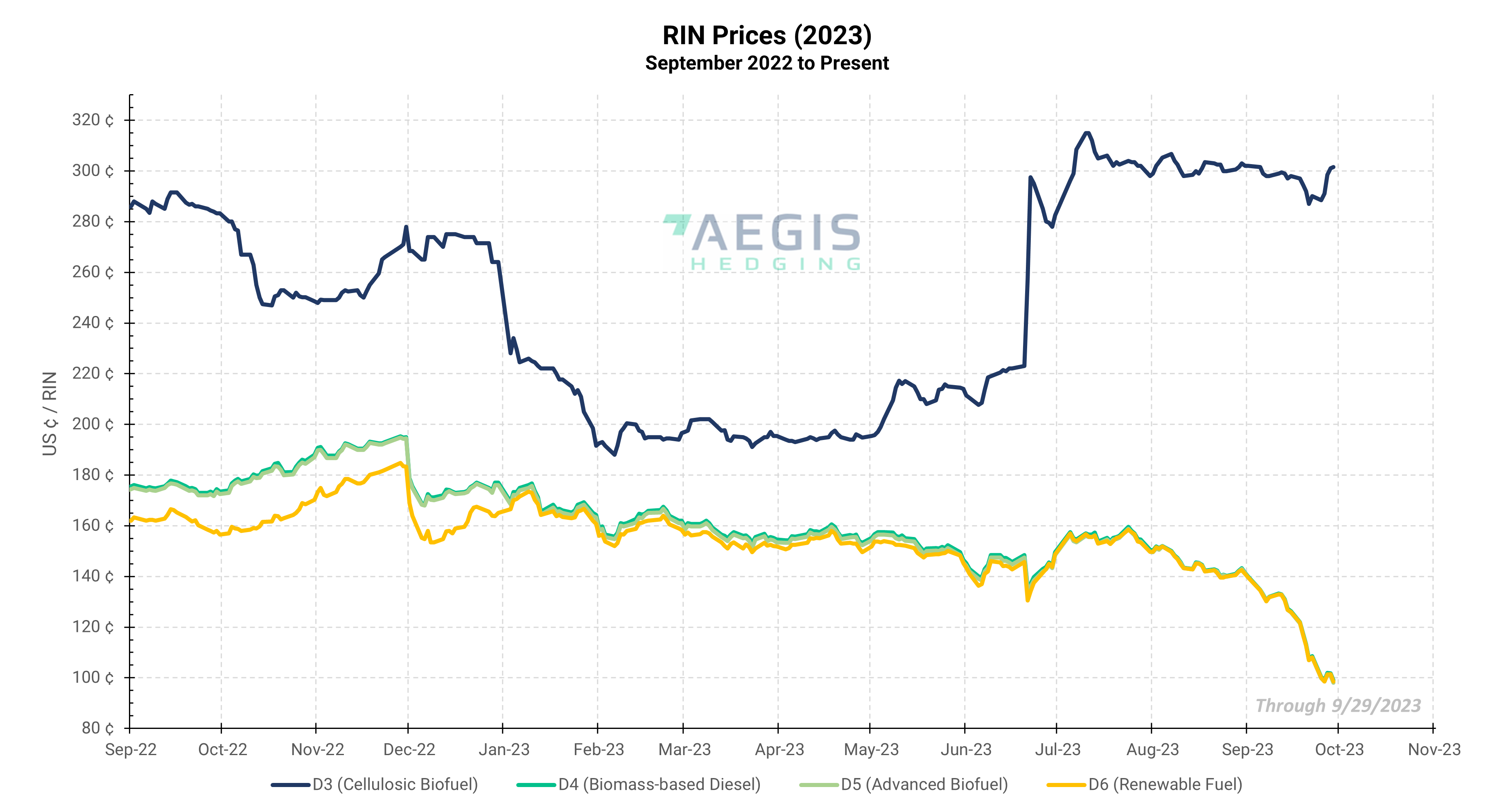

D3 |

D4 |

D5 |

D6 |

|

Price September 29th, 2023 |

$ 3.02 |

$ 0.99 | $ 0.98 | $ 0.99 |

|

Avg. Weekly Price September 25th - September 29th, 2023 |

$ 2.96 |

$ 1.00 | $ 1.00 | $ 1.00 |

|

Average Monthly Price September 2023 |

$ 2.97 |

$ 1.02 | $ 1.19 | $ 1.19 |

Current year vintage D4 RINs tumbled $0.13/RIN, or 11.7%, to average $1.004/RIN. The market reached as low as $0.99, marking the lowest level since December 2020. The B22/B23 spread narrowed to 2.5c as B22 losses outpaced B23s despite an approaching December compliance deadline.

August total RIN generation came in at 2.04 billion credits, up 2.4% on the previous month and nearly 11% over year-ago levels.

D4 generation came in at over 701 million credits, up 13% from the previous month’s levels and 46% from year-ago levels. Total D4 production reached 5.03 billion credits, less than 2% short of satisfying the entire 2023 advanced biofuel mandate.

Domestic and foreign renewable diesel production accounted for 57% of total D4 output, domestic and foreign biodiesel made up 42%, while SAF accounted for less than one percentage point.

The EPA denied 26 small refinery exemptions covering the 2016-2018 and 2021-2023 compliance years on July 14. The move was consistent with the EPA’s blanket SRE denials under the Biden Administration. The two remaining SREs are for the 2018 compliance year.

We have been advising since last year that the Biden Administration was unlikely to approve any SREs.

SREs were carved out in the Renewable Fuel Standard (RFS) for refiners producing 75,000 b/d or less which could prove compliance with the RFS—i.e., purchasing RINs—resulted “undue economic hardship.”

The EPA retroactively overturned 69 Trump-Era SREs starting in April of last year by denying 31 SRE waivers for 2018 and then denying all SRE petitions for 2016 through 2020. Denying SREs is bullish for RINs markets as refiners must enter the marketplace to purchase RINs to cover compliance obligations which were originally waived.

Questions? Contact our team for more information: environmental@aegis-hedging.com