Latest Insight

Last Look: Oil snaps its two-week losing streak, finishing $1.63 higher this week

To quickly access the page content, please click on the links below:

|

|

||

|

|

||

|

LCFS Spot Contract |

California LCFS |

Oregon LCFS |

|

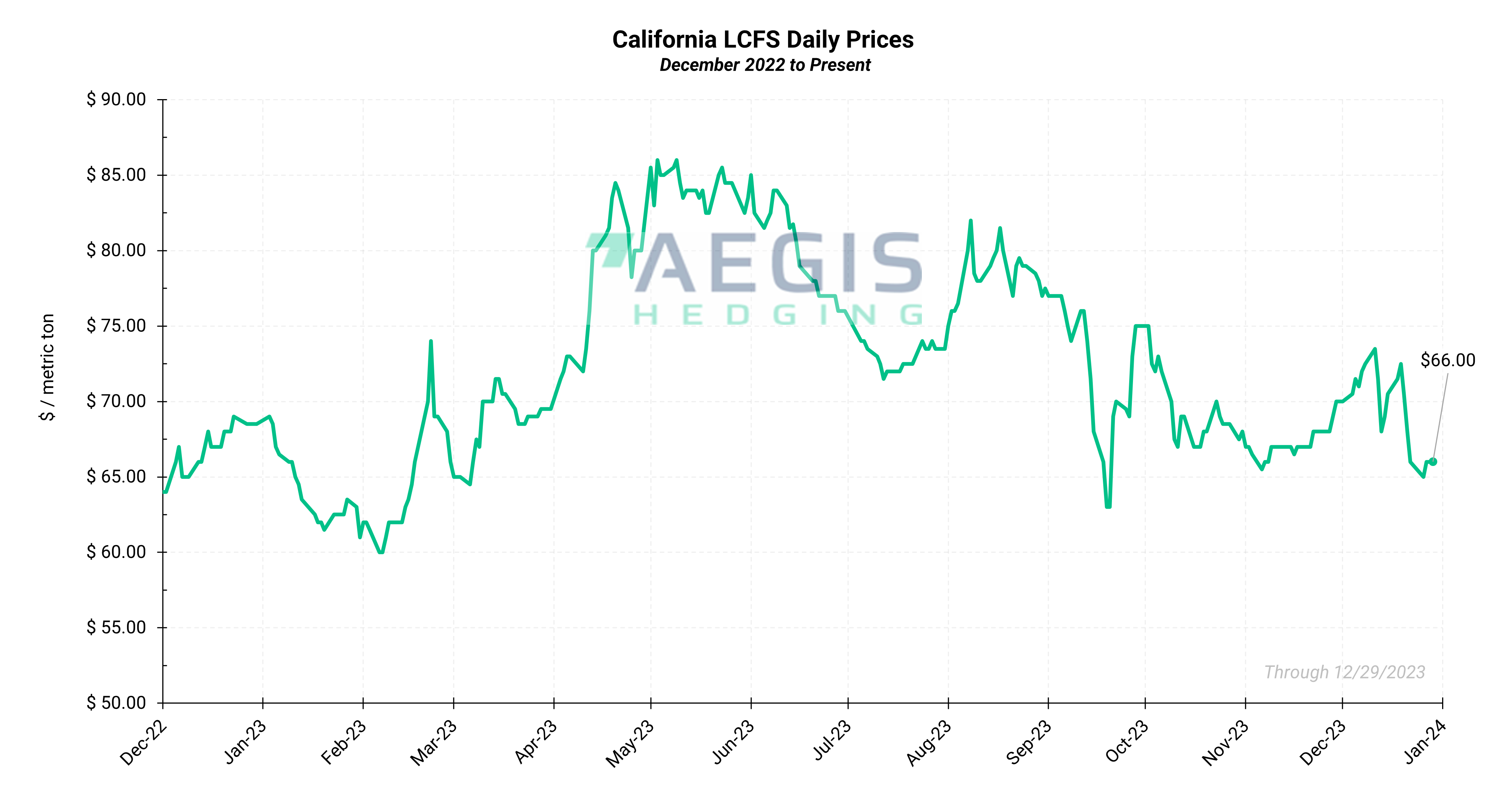

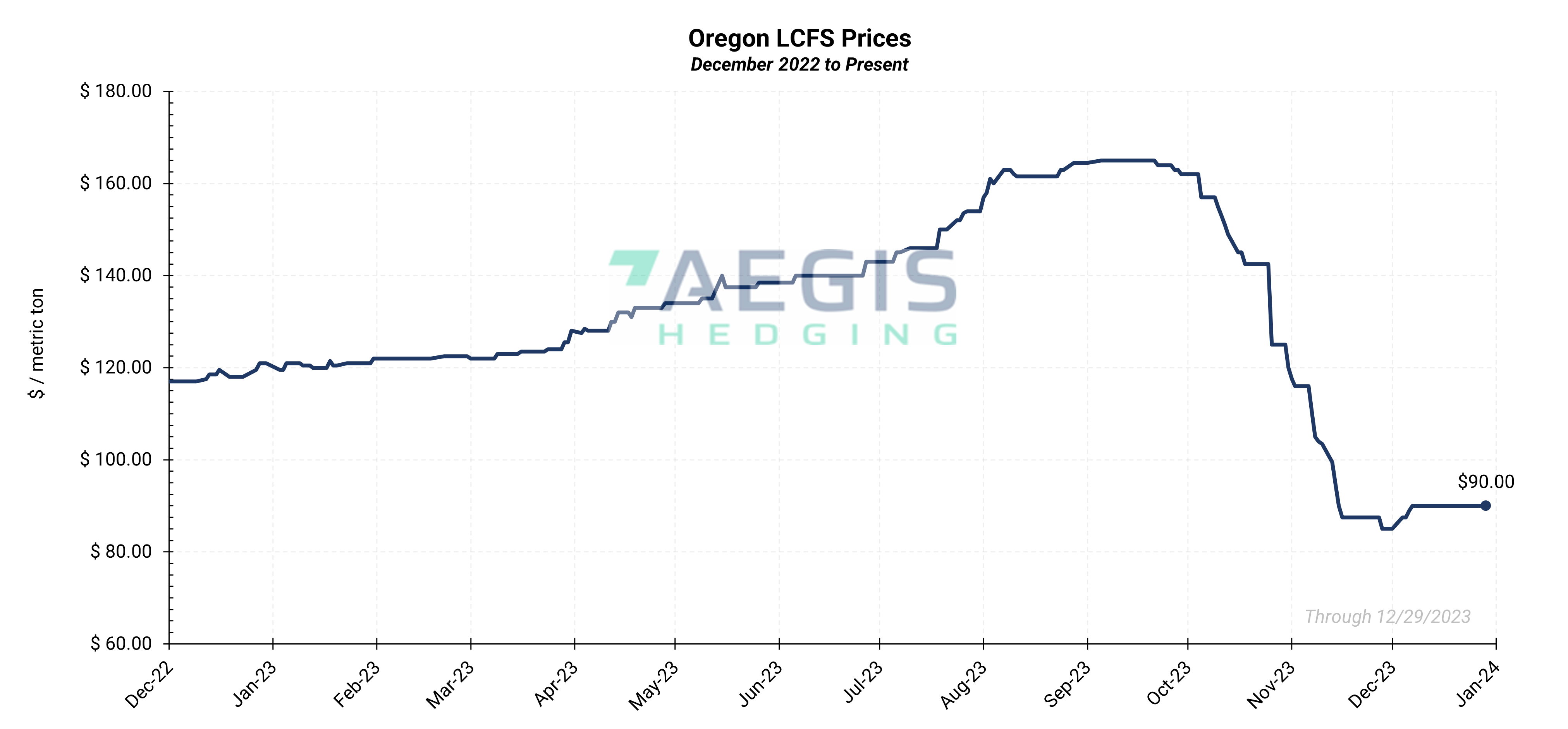

Price December 29th, 2023 |

$ 66.00 |

$ 90.00 |

|

Avg. Weekly Price December 26th - December 29th, 2023 |

$ 65.75 |

$ 90.00 |

|

Average Monthly Price December 2023 |

$ 69.58 |

$ 89.45 |

|

|

|

|

|

LCFS Futures Contract |

Pricing |

|

|

Dec. '24 |

$ 70.50 |

|

|

Dec. '25 |

$ 76.00 |

|

|

Dec. '26 |

$ 79.95 |

|

California Low Carbon Fuel Standard (LCFS) credit prices stabilized, halting two weeks of consecutive losses.

Prompt credits were stable at $66.00/t, levels not seen in a month and a half. The forward structure lack direction as well amid thinly participated holiday markets.

Contango heading into 2024 stood at flat, with a $1.00/t contango into Q2 2024 and Q3 2024.

On December 19, California’s Air Resources Board (CARB) released a preliminary LCFS proposal laying out amendments which nearly mirrored those in the Standardized Regulatory Impact Assessment released in September.

CARB proposed a 30% reduction in carbon intensity by 2030, including a 5% step-down in 2025. This marks a 50% increase in carbon targets over the original 20% reduction target for 2030.

Reductions increase to 90% by 2045 compared to a 2010 baseline.

The proposal contained an automatic acceleration mechanism (AAM) which would advance stringency for a given year when unused credits more than triple average deficit generation by advancing the carbon reduction target by two years.

Amendments included eliminating the exemption for intrastate jet fuel beginning in 2028 and new tracking requirements for crop-based and forestry-based feedstocks to their point of origin. CARB expects to kick off the required 45-day public comment period in January, with a public hearing set for March 21, 2024.

Prior to this proposal the prompt market had been in a choppy holding pattern since early May yet initiated a material downtrend starting in early June.

LCFS strength had been driven by trader buying and strength in futures markets as the credits become more attractive options ahead of CARB’s more stringent scoping plan.

Buying quickly turned to selling once the workshops concluded as traders became disillusioned with the timeline for the rulemaking.

|

||||

|

RIN Spot Contract |

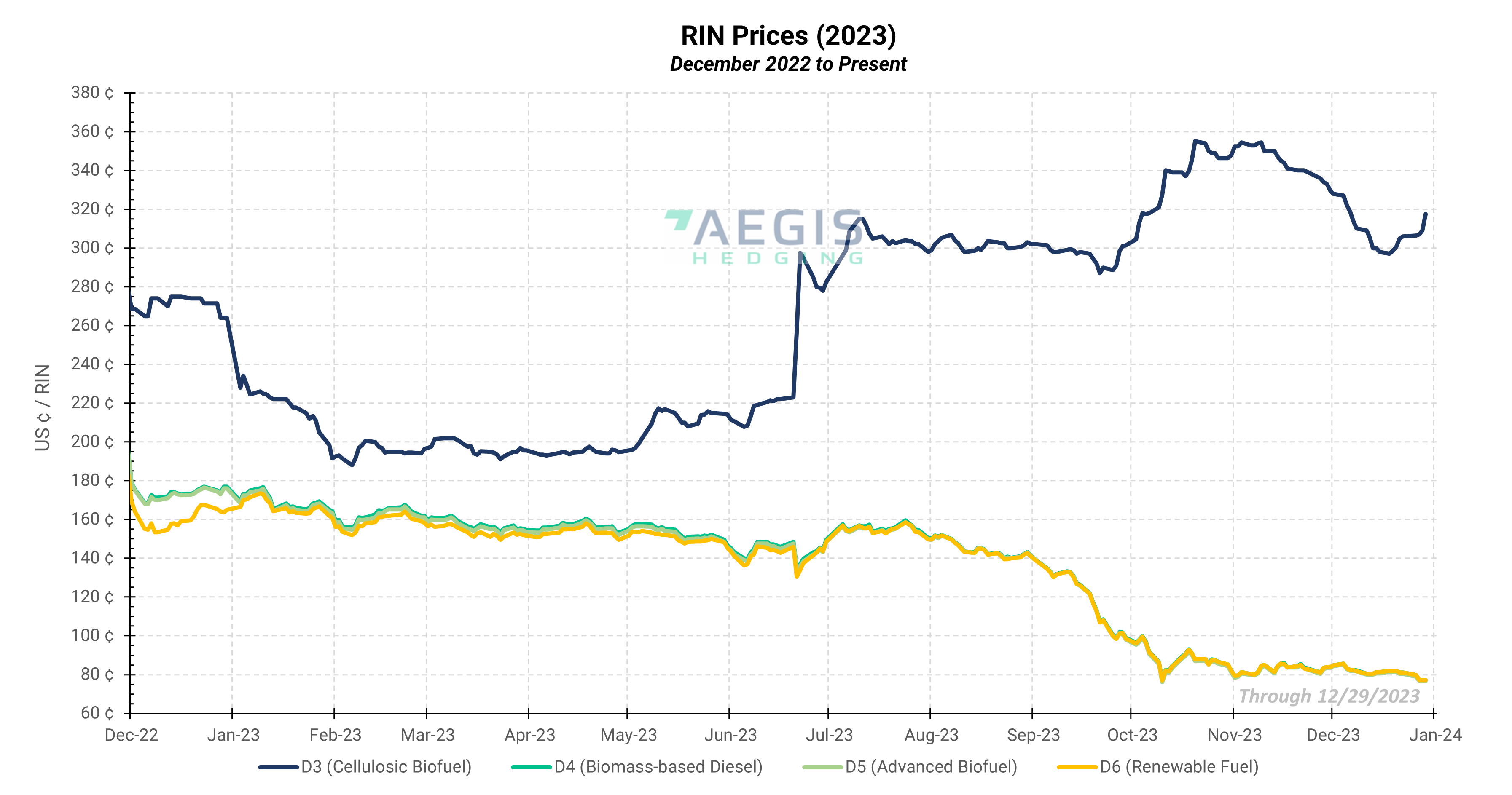

D3 |

D4 |

D5 |

D6 |

|

Price December 29th, 2023 |

$ 3.18 |

$ 0.77 | $ 0.77 | $ 0.77 |

|

Avg. Weekly Price December 26th - December 29th, 2023 |

$ 3.10 |

$ 0.78 | $ 0.77 | $ 0.78 |

|

Average Monthly Price December 2023 |

$ 3.09 |

$ 0.81 | $ 0.81 | $ 0.81 |

RINs came under pressure as the BOHO spread continued to average lower. The BOHO spread narrowed on average week-over-week, remaining near the lowest levels in a month and a half. The 2023 vintage market posted similar losses, with the inter-vintage spread inverting to -25pt.

The 5th US Circuit Court of Appeals ruled on November 22, 2023, to block denials of SREs for six refineries. The court’s decision said the EPA’s blanket SRE rejection was “impermissibly retroactive; contrary to law; and counter to the record evidence.” The decision will add a bearish undertone to an already oversupplied marketplace, save for D3 credits.

Fresh government data showed a mounting oversupply of D4 credits.

October total RIN generation came in at a record 2.1 billion credits, up 7.7% from the previous month when total RIN generation came in under 2.0 billion credits for the first time since April.

D4 generation came in at under 733 million credits, up 9% from the previous month’s levels and up 54% from year-ago levels. Total D4 production reached 7.72 billion credits, overshooting the entire 2023 advanced biofuel mandate by nearly 1.3 billion credits. Domestic renewable diesel production accounted for 47% of total D4 output, foreign renewable diesel made up 11%. Domestic and foreign biodiesel accounted for 41% of total D4 output, down from 44% the month prior. SAF accounted for less than one percentage point.

D3 RIN generation fell 10% from the previous month and is running just 13% over year-ago levels compared to a 25% growth rate used by the EPA to set the 2023 final mandate.

The EPA denied 26 small refinery exemptions covering the 2016-2018 and 2021-2023 compliance years on July 14. The move was consistent with the EPA’s blanket SRE denials under the Biden Administration. The two remaining SREs are for the 2018 compliance year.

SREs were carved out in the Renewable Fuel Standard (RFS) for refiners producing 75,000 b/d or less which could prove compliance with the RFS—i.e., purchasing RINs—resulted “undue economic hardship.”

The EPA retroactively overturned 69 Trump-Era SREs starting in April of last year by denying 31 SRE waivers for 2018 and then denying all SRE petitions for 2016 through 2020. Denying SREs is bullish for RINs markets as refiners must enter the marketplace to purchase RINs to cover compliance obligations which were originally waived.

Questions? Contact our team for more information: environmental@aegis-hedging.com