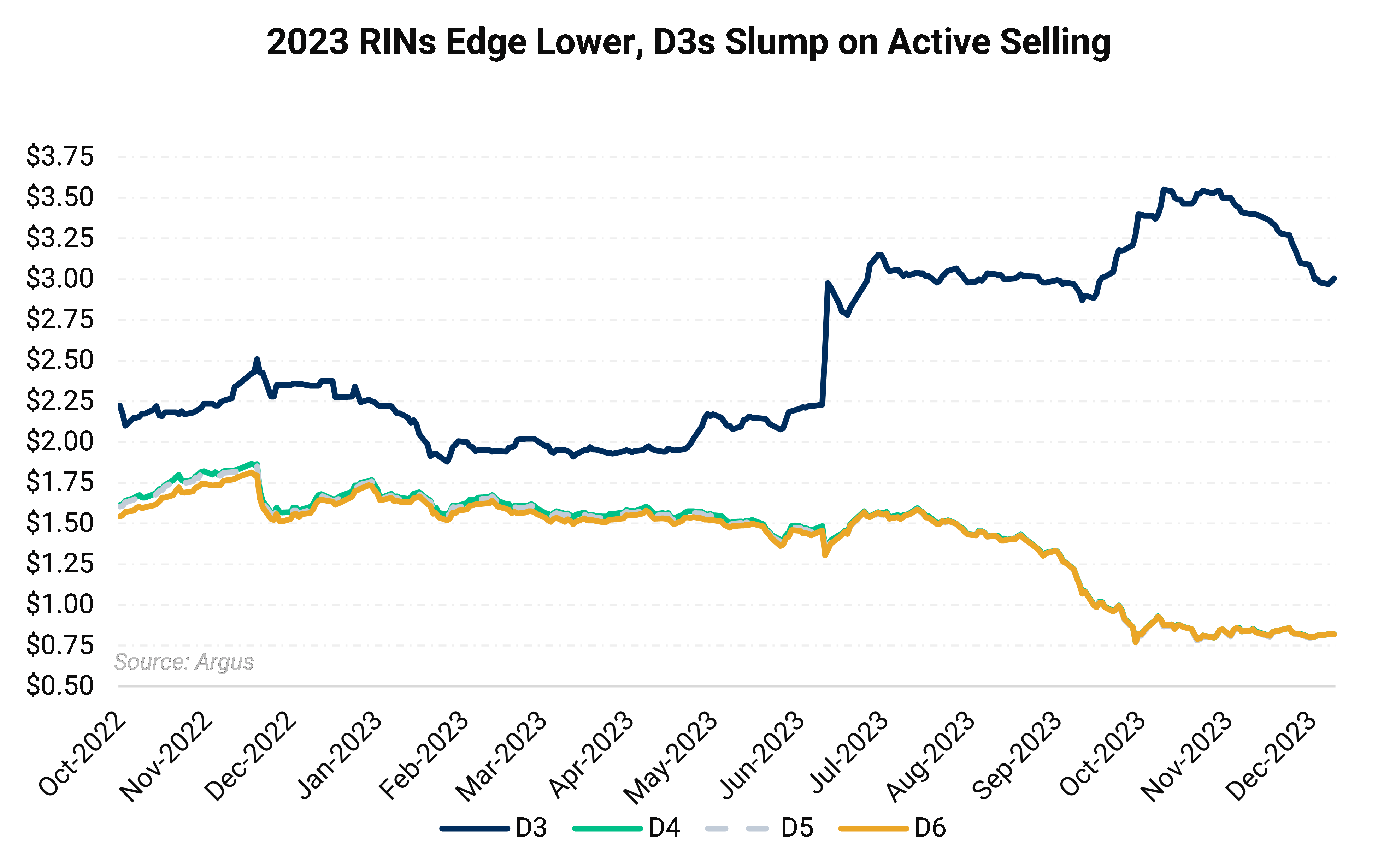

RIN prices posted modest losses as a recovery in the margin environment spurred selling. Renewable diesel margins proved volatile, bottoming out in early December, before recovering nearly 40% on average by the third week of the month. The RIN market rebounded off the lowest levels in over three years as diesel weakness spurred buying in the first half of November.

Diesel weakness saw the soybean oil-heating oil (BOHO) spread widen to $1.28/gallon on December 8, a level not seen since early October. The spread rapidly narrowed to $1.08/gallon as diesel prices rebounded over the second and third weeks of the month. A narrower BOHO spread implies stronger biodiesel margins, which is bearish the D4 RIN all else equal.

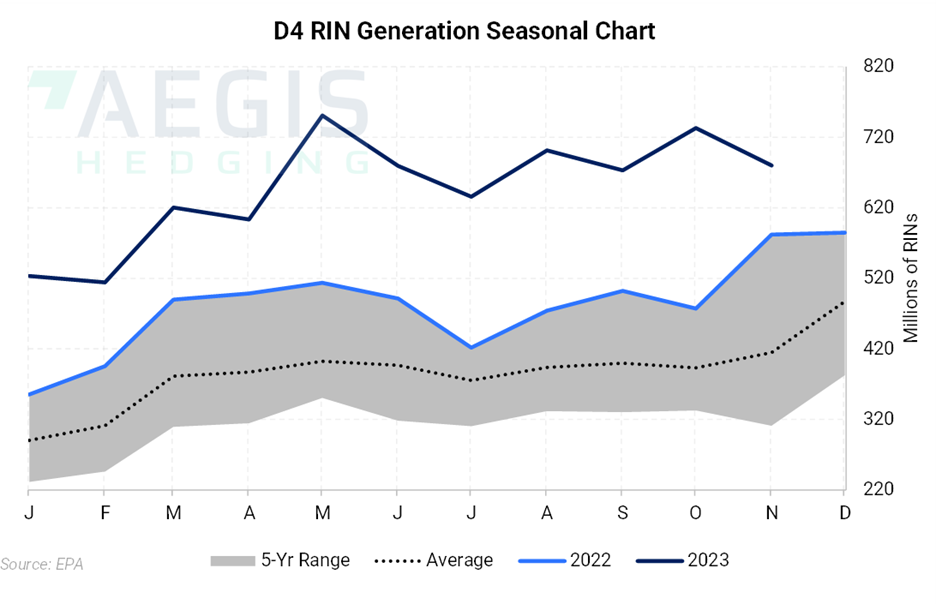

The December 21 release of November RIN generation showed 1.99 billion credits generated, down 11% from a record 2.1 billion credits generated in the month prior. Credit generation fell across all D categories except for D7, which posted credits for the first time in two months.

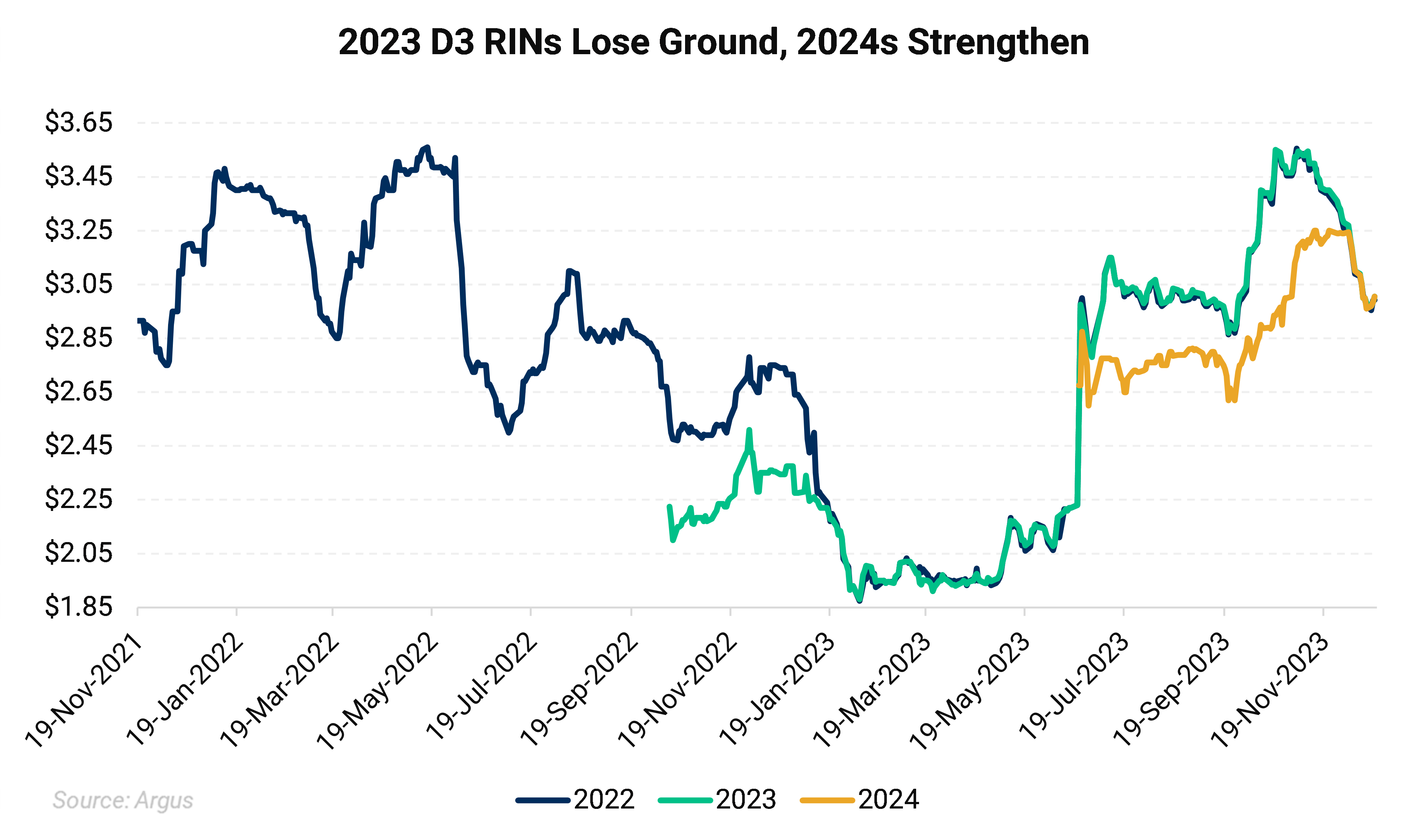

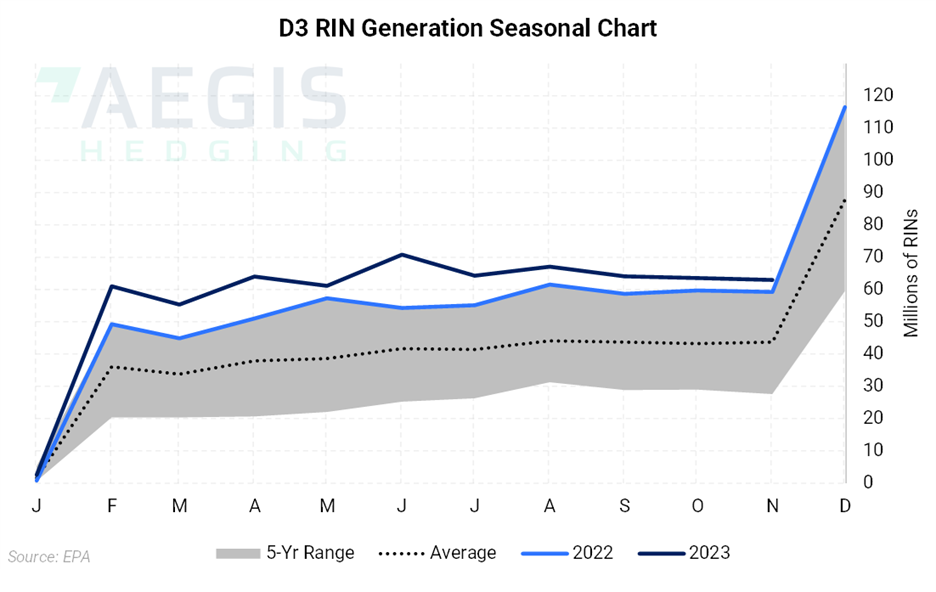

The D3 market continued a slump which started in early November as active selling pressured prices under the $3.00/RIN mark. The rout saw the 2023-2024 D3 spread compress to flat during the first three weeks of December.

Insufficient RIN generation and the lack of a Cellulosic Waiver Credit (CWC) had been supporting the 2023 market, yet the market began to price in the increased likelihood of deferred 2023 compliance. Total D3 RIN generation is running around 10% short of the cellulosic mandate.

- November total RIN generation came in at 1.99 billion credits, down 11% from the previous month when total RIN generation reached a record 2.1 billion credits.

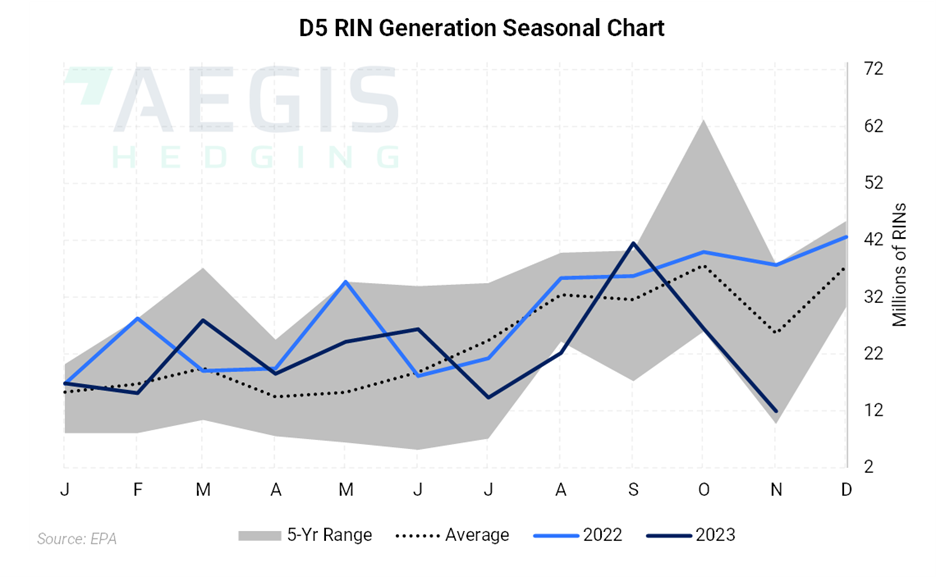

- D4 generation came in at 680 million credits, down 7% from the previous month’s level. Total D4 production reached 7.12 billion credits and is on pace to reach 7.76 billion credits by years’ end. Domestic renewable diesel production accounted for 49.5% of total D4 output, up from 47% the month prior. Foreign renewable diesel made up 11% of total D4 generation, steady from last month’s share. Domestic and imported biodiesel accounted for 39% of total D4 output, down from 41% the month prior, with no foreign biodiesel reported. No D4 credits for SAF were reported in November after accounting for less than one percentage point in October.

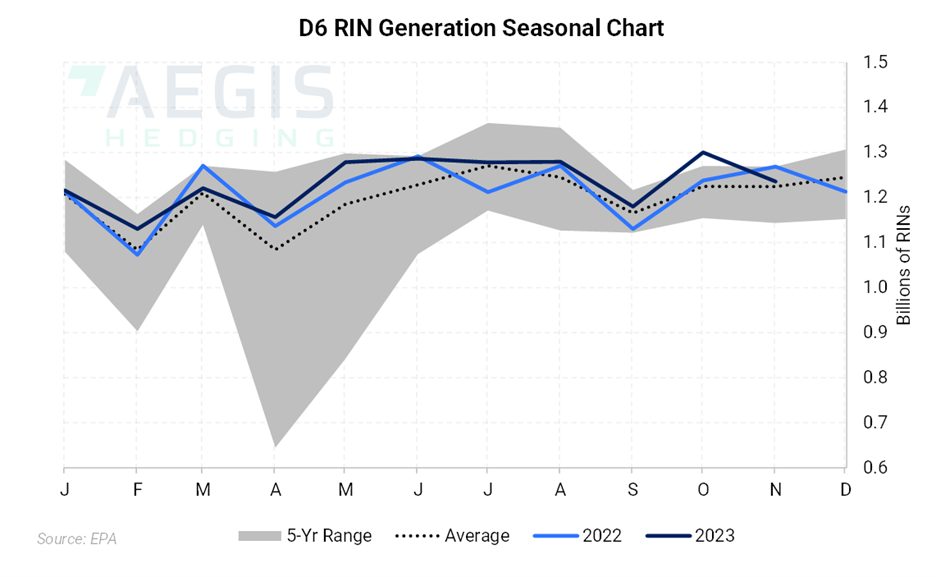

- D3 RIN generation fell less than one percent from the previous month. Total output to date is running just 15% over year-ago levels compared to a 25% growth rate used by the EPA to set the 2023 final mandate. Total D3 RIN generation is on pace to fall 10% short of the final mandate of 840 million RINs.

- November RIN generation data housed numerous revisions to 2021-2023 production levels for D6 credits upward revisions total 23,017,855 credits spanning from January 2021 to August 2023. The prior month’s generation data housed downward revisions totaling 16,514,951 credits across June and August 2023. D4 generation was revised 1,206,061 higher from April to October 2023. D5 generation was revised 5,086,213 higher for the month of October 2023, nearly offsetting the previous month’s downward revision of 5,686,621. D3 RIN generation saw an upward revision of 5,681,637 for the month of October, more than offsetting last month's downward revision of 4,975,315 credits.

- The EIA projected 2023 renewable diesel production of 174,000 Bbl/d in its December Short-Term Energy Outlook, a 1.8% increase from November. The forecast for 2024 production was cut by 0.8% to 236,000 Bbl/d. Demand for 2023 was forecast 1,000 Bbl/d higher at 195,000 Bbl/d, while the 2024 demand outlook was cut by 2,000 Bbl/d to 260,000 Bbl/d. The December STEO showed 2023 net renewable diesel imports unchanged at 23,000 Bbl/d for 2023 and 24,000 Bbl/d for 2023.

- EPA Fuel Program Center Director, Paul Machiele, said the oversupply of D4 credits is not currently a concern at the EPA as the agency’s primary driver in setting the 2023-2025 mandates was feedstock availability, according to Carbon Pulse. Machiele noted that the surge in imported feedstock was not taken into account when considering the final Set Rule, speaking at the OPIS RFS, RINs and Biofuels Forum in Chicago. Changes to exiting mandates are unlikely to be taken up during an election year. President of Advanced Biofuels Association, Michael McAdams, cited an unnamed source that the earliest the EPA would take action is 2026.

- EPA officials indicated that the next opportunity for addressing the adoption of the contentious eRIN pathway would be when the agency considers blending targets for 2026, according to EPA Fuel Programs Center director Paul Machiele when speaking at the Argus North American Biofuels, LCFS, & Carbon Markets Summit in mid-September.

Calendar:

- January 31, 2024: Three-year Registration Update

- March 31, 2024: EPA Expected Deadline for 2023 Compliance

- June 1, 2024: Attest Engagement Reporting Deadline for 2022

- March 31, 2025: EPA Expected Deadline for 2024 Compliance

Relevant News:

- The 5th US Circuit Court of Appeals ruled to block denials of SREs for six refineries. The SREs cover Calumet’s 57,000 Bbl/d Shreveport, Louisiana refinery, Placid Refining’s 75,000 Bbl/d Port Allen, Louisiana refinery, Ergon Refining’s 26,500 Bbl,d Vicksburg, Mississippi refinery, Ergon’s 23,000 Bbl,d West Virginia refinery, CVR’s 74,500 Bbl/d Wynnewood, Oklahoma refinery, and Allegiance Refining’s 21,000 Bbl/d San Antonio refinery. The court’s decision said the EPA’s blanket SRE rejection was “impermissibly retroactive; contrary to law; and counter to the record evidence.” The decision will add a bearish undertone to an already oversupplied marketplace, save for D3 credits.

- The US Treasury Department issued guidance on December 15, 2023, clarifying how SAF will be eligible for tax credits worth as much as $1.75/gallon under the Inflation Reduction Act. The SAF tax credit is only issued to fuels which reduce lifecycle GHG emissions 50% below petroleum-derived jet fuel. The Treasury Department plans to calculate emissions intensity using a modified version of the GREEET model planned for March 1, 2024. The adjusted GREET model could open the door for corn-based ethanol to contribute to SAF supply.

- On December 19, California’s Air Resources Board (CARB) released a preliminary LCFS proposal laying out amendments which nearly mirrored those in the Standardized Regulatory Impact Assessment released in September. CARB proposed a 30% reduction in carbon intensity by 2030, including a 5% step-down in 2025. This marks a 50% increase in carbon targets over the original 20% reduction target for 2030. Reductions increase to 90% by 2045 compared to a 2010 baseline. The proposal contained an automatic acceleration mechanism (AAM) which would advance stringency for a given year when unused credits more than triple average deficit generation by advancing the carbon reduction target by two years. Amendments included eliminating the exemption for intrastate jet fuel beginning in 2028 and new tracking requirements for crop-based and forestry-based feedstocks to their point of origin. The regulator proposed phasing out biogas used in transportation fuel by 2041 and by 2045 for biomethane used to produce renewable hydrogen. CARB expects to kick off the required 45-day public comment period in January, with a public hearing set for March 21, 2024.

- Recent fires at Marathon’s Martinez refinery triggered a federal investigation by the Chemical Safety and Hazard Investigation Board (CSB). Fires on November 11 and November 19 at a hydrodeoxygenation (HDO) unit led to spills of RD. Marathon aims to achieve 48,000 Bbl/d of production at its Martinez, California facility by year-end.

- Federal judges defended the EPA’s approach to setting the 2020-2022 blending mandates. US refiners have complained blend requirements were too high based on how the EPA adjusted blending targets to account for projected Small Refinery Exemptions (SREs). The EPA is also facing a separate lawsuit for its 2022 cellulosic biofuel requirement, with biofuel groups arguing that targets were set too low based on projections of actual production and not accounting for the availability of carryover credits for compliance. Refiners have also filed a series of lawsuits in the DC Circuit court challenging the EPA’s move to reject all outstanding SREs this year.

- HF Sinclair reported third quarter renewable diesel sales of 14,500 Bbl/d. The independent refiner is an obligated party in both Oregon and Washington state and operates RD facilities in Cheyenne, Wyoming, and Artesia, New Mexico.

- Calumet plans to add 3,000 Bbl/d of capacity to its 15,000 Bbl/d, Great Falls, Montana Renewables refinery by 2025. The Great Falls plant is currently undergoing repairs to a steam recovery system and moved forward a turnaround originally planned for 2024 to November. Calumet is mulling plans to ultimately maximize SAF production at the Great Falls facility.

- A California judge ruled that P66’s 67,000 Bbl/d RD Rodeo facility may not operate until permitting issues are resolved. The largest RD refinery conversion in the country is allowed to continue construction. The original permitting work for the plant took nearly a year to complete in May 2022. P66 aims to begin RD production at Rodeo by Q1 2024.

RIN markets posted modest losses over the course of December as the margin environment proved volatile. The mounting supply of D4 credits continued to hold spreads near flat.

Renewable diesel margins proved volatile, bottoming out in early December, before recovering nearly 40% on average by the third week of the month. The RIN market rebounded off the lowest levels in over three years as diesel weakness spurred buying in the first half of November.

Diesel weakness saw the soybean oil-heating oil (BOHO) spread widen to $1.28/gallon on December 8, a level not seen since early October. The spread rapidly narrowed to $1.08/gallon as diesel prices rebounded over the second and third weeks of the month. A narrower BOHO spread implies stronger biodiesel margins, which is bearish the D4 RIN all else equal.

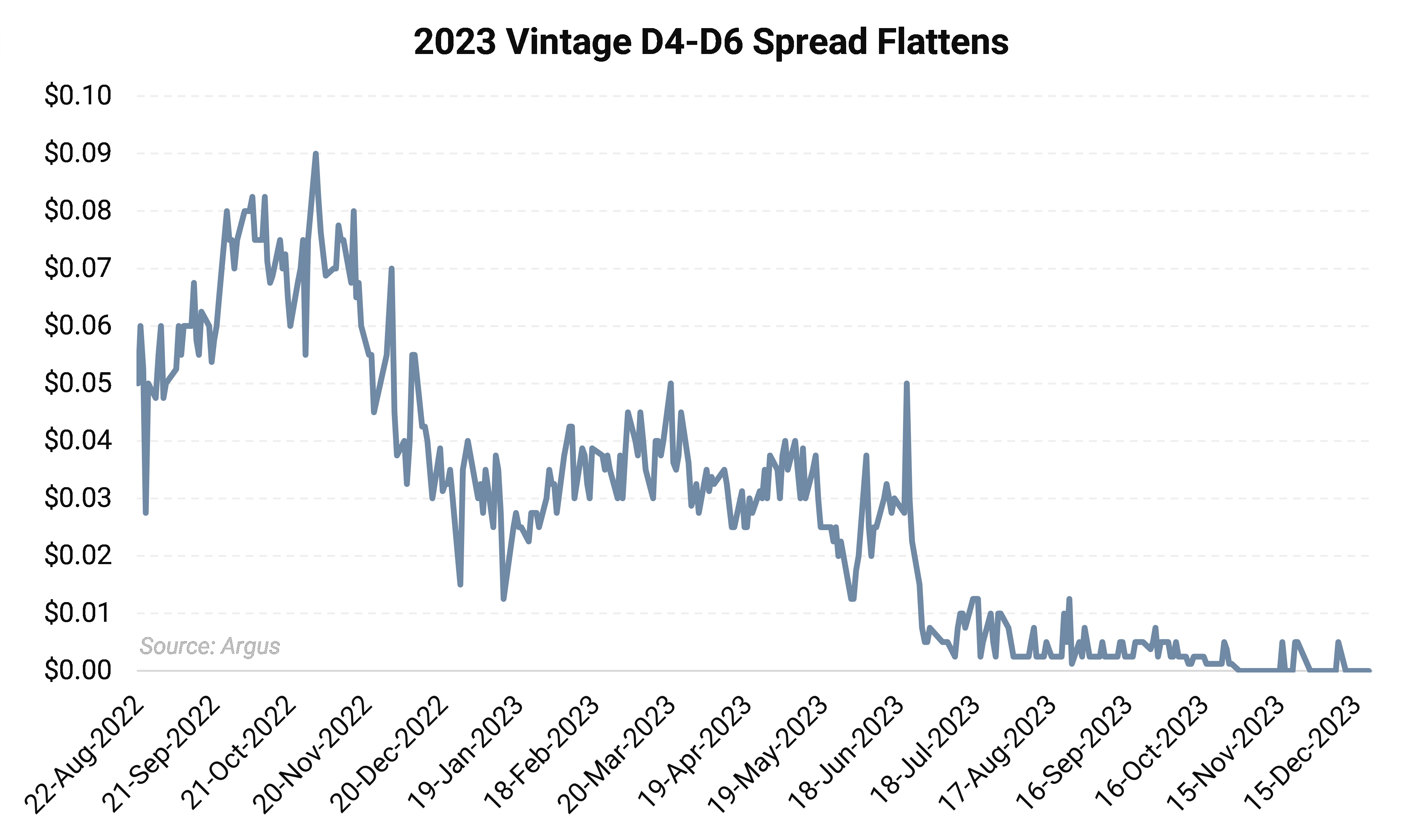

Current year vintage D4 RINs shed 2.8c, or 3.2% since the start of December. The D6 market posted identical losses over the same period with the D4/D6 spread holding at flat.

A narrower D4/D6 spread indicates tightness in D6 supply. In the absence of a sufficient supply of D6 credits, D4 and D5 credits from the advanced category can be used to satisfy compliance obligations.

We expect the 2023 D4/D6 spread to hold flat as the D4 RIN is the main vehicle of compliance for the total renewable fuel mandate.

D6 RIN generation is on pace to fall short of mandated volumes, though ample D4 RINs are available to cover the D6 compliance shortfall which will keep the D4/D6 spread near parity.

The 2023 D3 market continued a downturn that started in November as active selling throughout the holiday season saw 2023 vintage D3 RINs tumble 27.5c/RIN, or 8.4% since the start of December, recovering to just over $3.00/RIN by December 20.

The C23/C24 spread narrowed to flat after starting the month of November at 39.5c/RIN and reaching as high as 61.5c/RIN during October. This marks the narrowest spread since late June 2023 when the spread was inverted. The prospect of deferred 2023 compliance drove strength in 2024 D3 markets last month driving the inter-vintage spread to flat.

D3 RIN generation fell less than one percent from the previous month. Total output to date is running just 15% over year-ago levels compared to a 25% growth rate used by the EPA to set the 2023 final mandate. Total D3 RIN generation is on pace to fall 10% short of the final 840-million-gallon 2023 mandate. With no Cellulosic Waiver Credit in place and a record low RIN bank, we expect D3 RINs to remain at elevated levels barring an early implementation of eRINs and/or the issuance of a CWC under the EPA’s waiver authority.

The 2022 vintage D3 market shed 26.8c over the course of December, and the inter-vintage spread held fluctuated between flat and -1c/RIN.

The 2023 D4-D6 spread spent the entirety of the first three weeks of December at flat, stable from November. We expect the 2023 D4/D6 spread to hold flat as the D4 RIN is the main vehicle of compliance for the total renewable fuel mandate.

A wider D4-D6 spread implies a looser D6 supply as the D4 credit is the next vehicle of compliance in the absence of sufficient D6 RINs or the ability to use carryover credits. Conversely, a narrow D4-D6 spread implies a tight supply of D6 RINs. The theoretical cap on the spread is parity though D6s have traded at modest premiums to D4 credits in extreme circumstances.

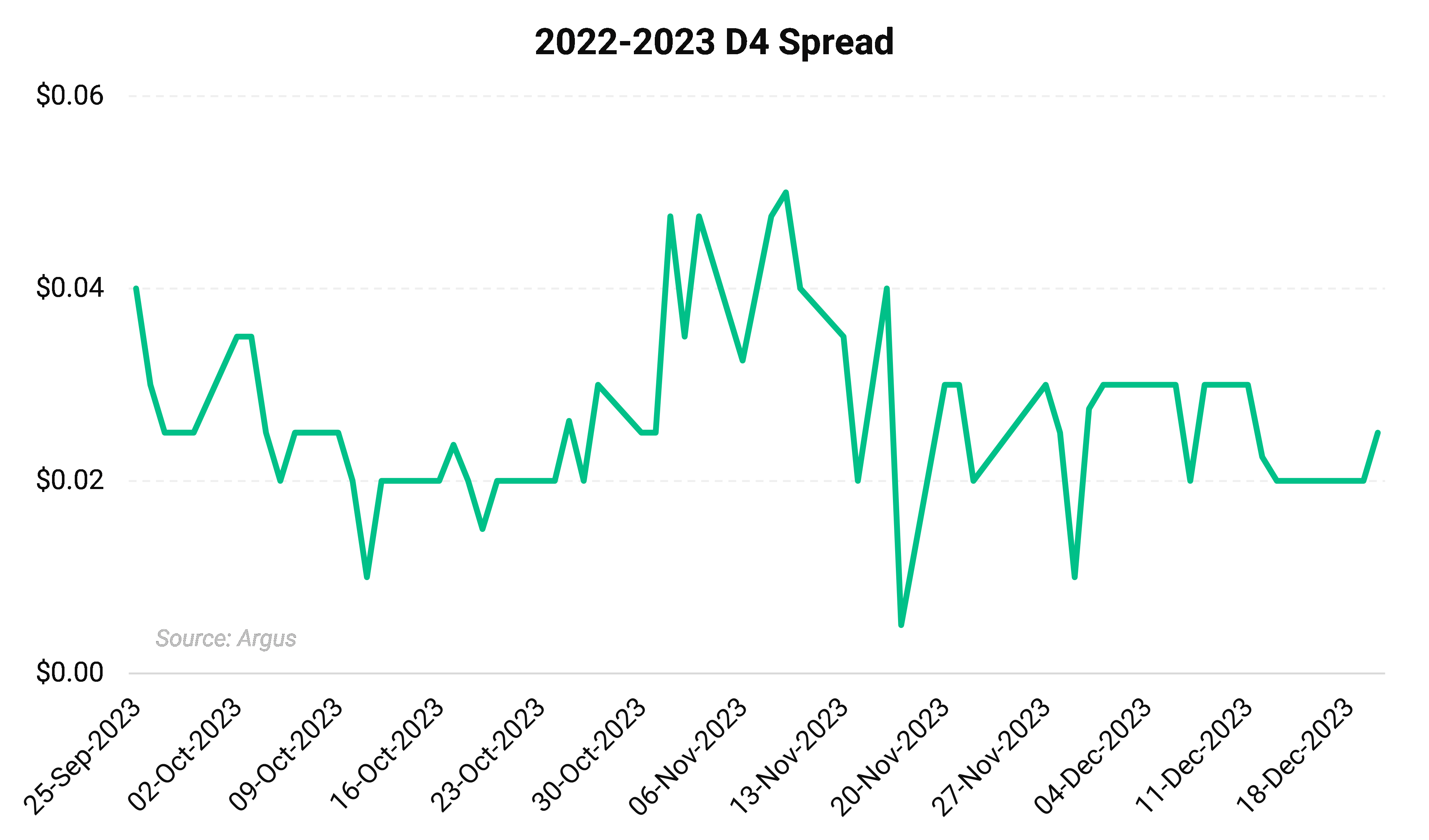

The inter-vintage D4 RIN spread narrowed down to the 2c mark following a more volatile November as the December 1 compliance deadline spurred activity. The spread started the month of December as wide as 3c before narrowing to 2c, averaging 2.5c for the first three weeks of the month.

AEGIS noted in earlier reports that volatility in diesel throughout the fourth quarter would drive credit markets as one of the main vehicles for buttressing renewable diesel margins. RIN generation should remain at elevated levels even if Q4 startups are delayed or run at reduced rates as long as feedstock pricing remains under pressure from imports. Poor margins have seen the closure of at least one small biodiesel plant.

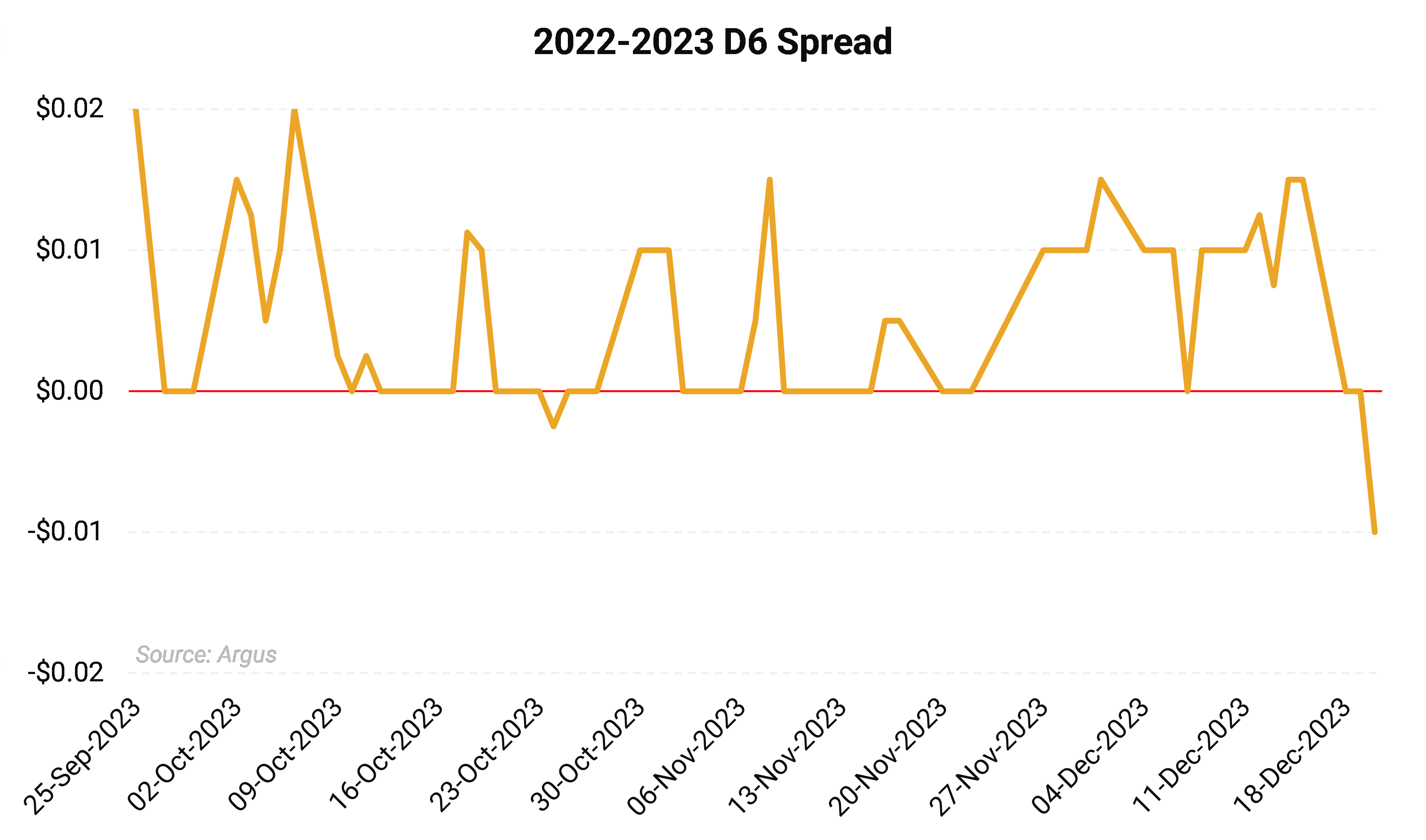

The 2022-2023 D6 spread fluctuated between flat and +1c before slipping to -1c on December 20. The inter-vintage D6 spread held at flat for the bulk of November.

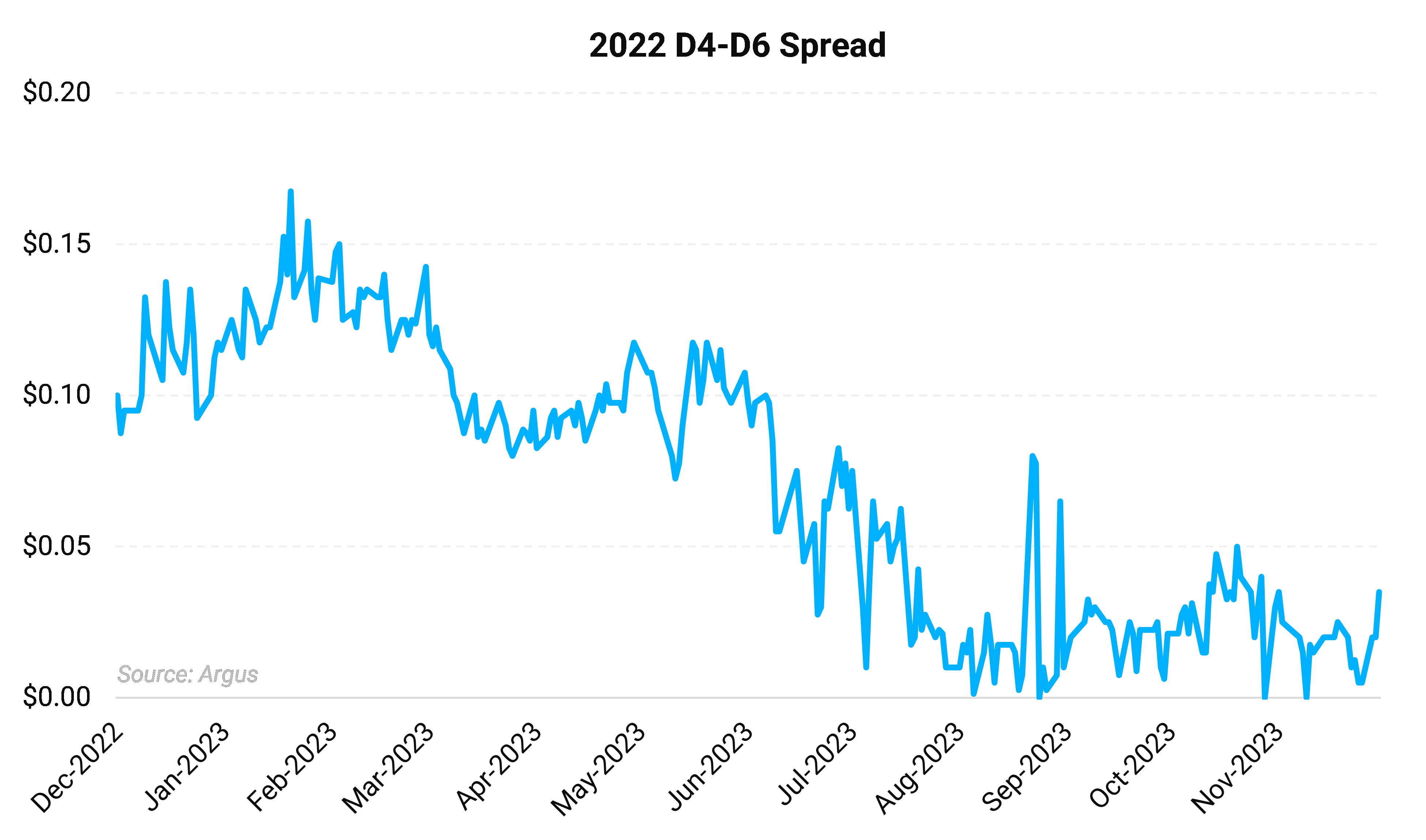

The 2022 D4-D6 spread narrowed on average to 1.8c during the first three weeks of December, down from November’s average of 2.9c. The spread averaged 2c in October, 2.4c in September, 4c/RIN in August, 5.5c/RIN in July, 9.6c/RIN during the month of June, and 9.8c/RIN during the month of May.

EPA RIN Generation Data as of Novembrer 17:

EPA Small Refinery Exemption (SRE) Data as of November 17:

Green indicates change

Some of the price and regulatory risk in the development of the renewable fuels markets is controllable through hedging or pre-selling. Other risks require constant monitoring of pending changes to regulations and programs. AEGIS can help with both.

Interested in receiving these updates directly to your inbox?