Latest Insight

First Look: EQT's 1Q24 earnings highlight expanding data center demand and managing production

|

|

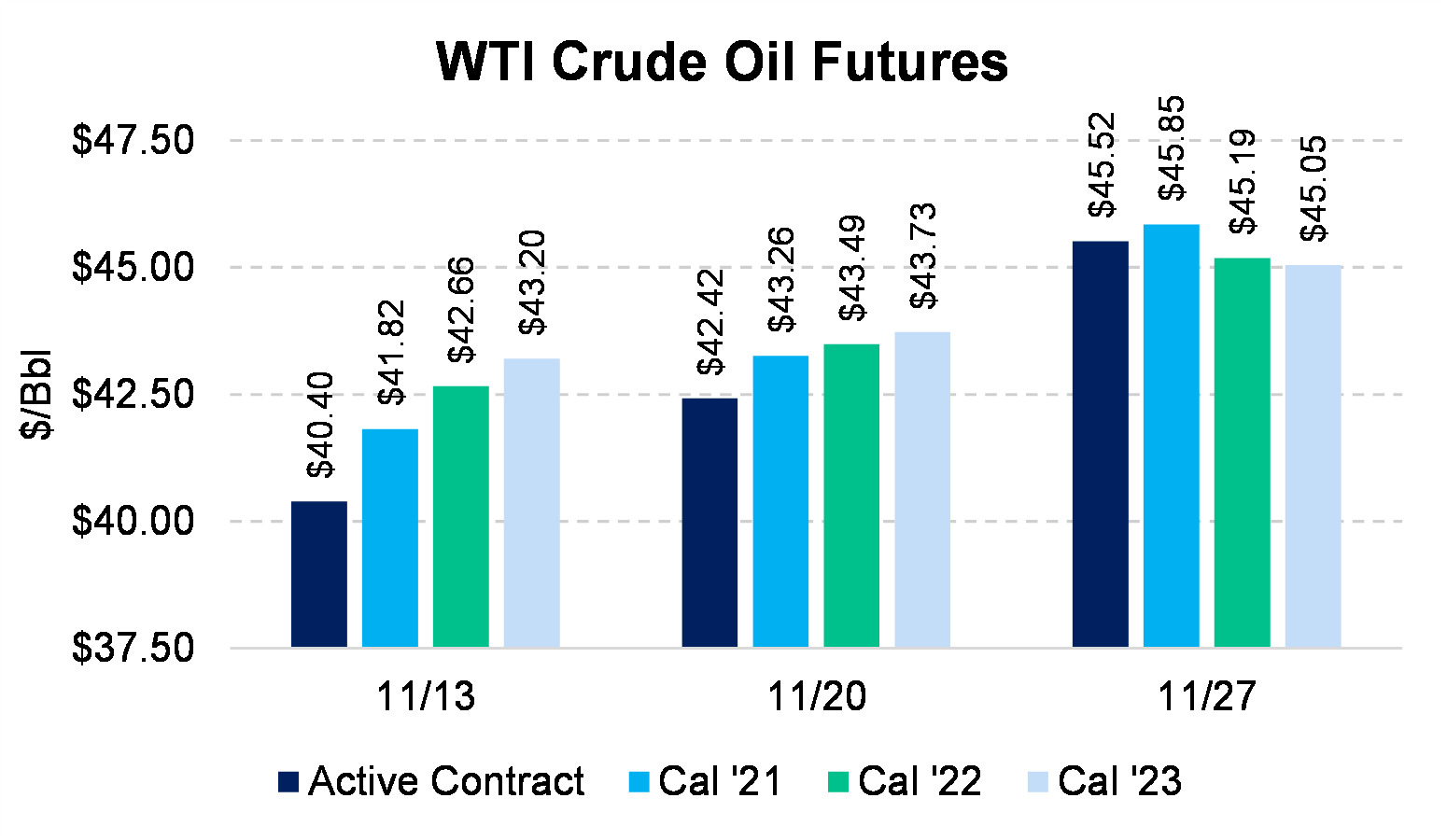

Bottom Line: WTI has been in a remarkably steady climb for all of November, with the January tenor now at $45.53. It is curious that the near-term strength has coincided with encouraging vaccine developments, but those vaccines would not have wide distribution until 2Q2021 per some government estimates. Yet, oil climbs, and we're concerned it is happening despite some headwinds.

A higher oil price is a psychological relief. Seeing bullish news can make us feel like better times are here. When prices move, the temptation is to wait and see how high it could go — try to hedge it at the top. However, we see this rally as an opportunity to sell at a higher price, rather than a signal that prices could go higher.

Prices do not have to agree with fundamentals. And, with the curve touching the mid-$40s, we see evidence in trading, in the news, and among our clients that D&C activity will increase. Therefore, $45 sounds like a fundamental ceiling. If price pierces through that ceiling, then it's possible more supply is encouraged to flow. Is such a supply-inducing price rally happening too soon?

We think it may be. In fact, we are emphasizing the use of swaps instead of option structures for tenors through mid-2021. Sell into this rally aggressively if you still need a foundation of hedges.

Also, if this rally is happening before demand has begun recovering (we're going back to the assumption that vaccines won't proliferate until mid-2021), then the early price recovery could also cause more supply growth in 2022 than anticipated. We previously documented that $50/Bbl WTI could generate an extra 1 MMBbl/d of U.S. production in one year. And $45 also has an effect, albeit smaller. Maybe that growth starts showing up in late 2021 now, rather than in 2022 as we originally thought. Could capital expenditures driving this growth already be deployed? An interesting twist in the shape of the forward curve could be signaling widespread hedging by producers. Our own trade volume has been high in November, so our representative AEGIS sample of U.S. oil producers would corroborate this. Check out the evidence (and a killer animated chart on curve evolution) in our article here.

What could you do with an existing hedge portfolio now that prices are a little higher? One thing to consider when prices are moving higher could be converting any three-way collars. Why? The three-ways are hedges designed to give protection, but also to keep exposure to upside. When the market rallies, you can mentally consider the three-way collar to have done its job. Contact the AEGIS trading desk if converting those old three-ways into swaps or vanilla collars could make sense.

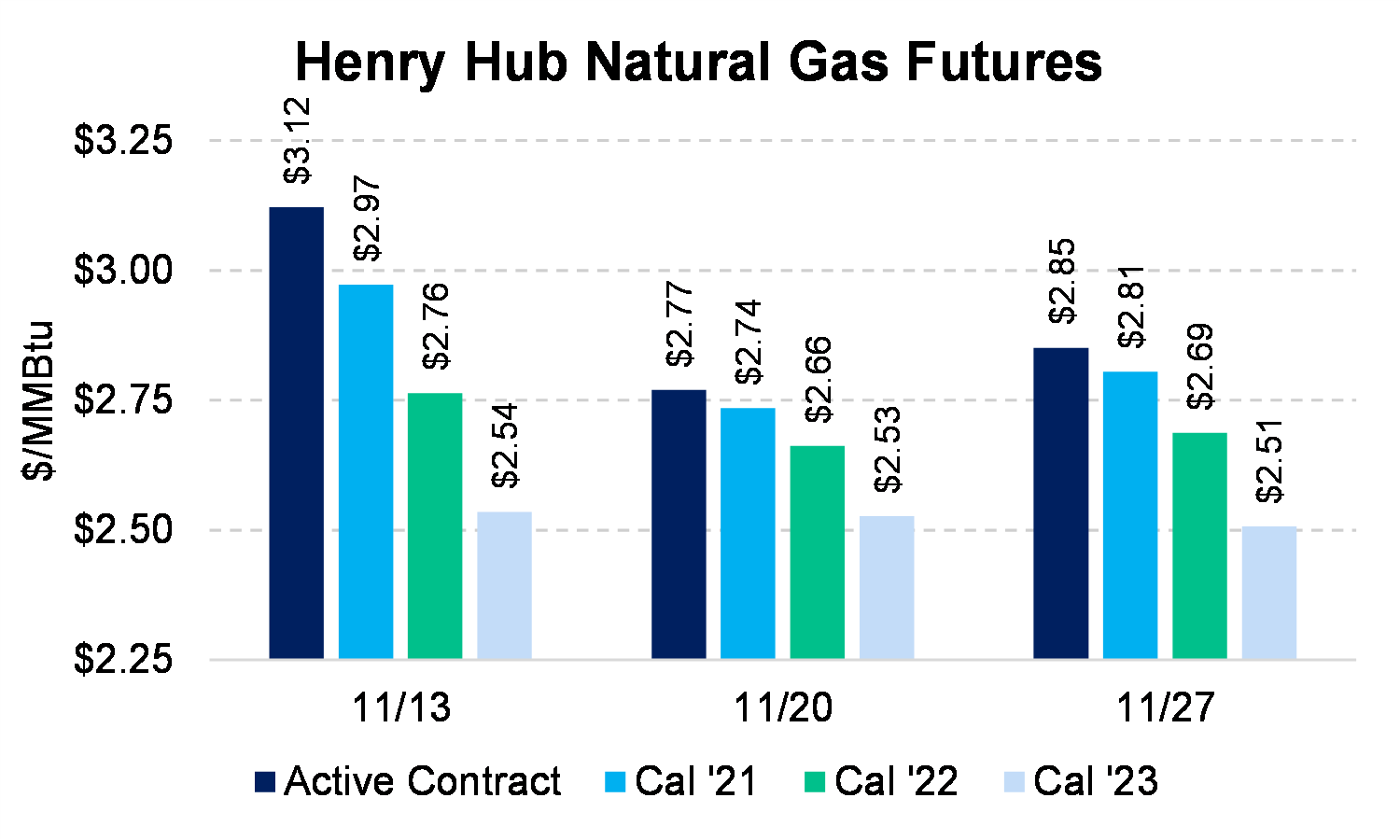

Bottom Line: Natural gas was having a good week until Friday. The January contract had bottomed out around $2.72, then flirted with $3, settling at $2.96 ahead of the Thanksgiving holiday. However, the threat of mild weather in the East and less cold air potential in Canada sent prices back down to $2.84 to close on Friday.

Don't forget some other non-weather factors that have held back gas prices. And, definitely don't forget why gas has perhaps 18 months of undersupply ahead of it. There is evidence of more gas supply both now and during 2021. Daily readings show Appalachia production has been rising during November. That is a near-term supply increase. But with oil prices rising, we are hearing of more producers in oil plays (think Permian basin) consider adding rigs or completing more wells. The timing is such that more gas could arrive in mid- to late-2021.

Therefore, watch out for continued oil development. It is a major factor to watch for next winter's gas market, and into 2022. With that in mind, consider some costless collars to hedge in Winter '21-'22. The levels are still high enough to establish a high floor. For example, intraday Friday (Nov 27), when the Winter '21-'22 swap was $2.97 on the AEGIS bid side, a costless collar could be constructed at a $2.75 floor, with a generous $3.35 cap. If you need to act, we like that costless collar's construction for most clients.

We recommend collars instead of swaps because our models still show a tightening supply-demand balance in late winter and 2021. Once weather cooperates, we would expect prices to improve quickly.